What is Thermotropic Liquid Crystalline Polymer - Global Market?

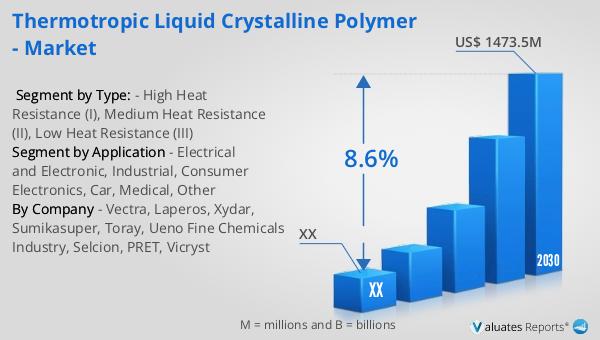

Thermotropic Liquid Crystalline Polymers (TLCPs) are a fascinating class of high-performance polymers that exhibit unique properties due to their liquid crystalline nature. These polymers are characterized by their ability to form ordered structures in the melt phase, which imparts them with exceptional mechanical and thermal properties. TLCPs are known for their high strength, stiffness, and resistance to heat and chemicals, making them ideal for demanding applications. They have a low density, which contributes to their excellent specific properties, meaning they offer high performance without adding significant weight. This makes them particularly valuable in industries where weight reduction is crucial, such as aerospace and automotive. The global market for TLCPs is growing as industries increasingly seek materials that can withstand harsh environments while maintaining structural integrity. In 2023, the market was valued at approximately US$ 836 million, and it is projected to reach around US$ 1473.5 million by 2030, growing at a compound annual growth rate (CAGR) of 8.6% from 2024 to 2030. This growth is driven by the rising demand for lightweight, durable materials in various sectors, including electronics, automotive, and industrial applications.

High Heat Resistance (I), Medium Heat Resistance (II), Low Heat Resistance (III) in the Thermotropic Liquid Crystalline Polymer - Global Market:

Thermotropic Liquid Crystalline Polymers (TLCPs) are categorized based on their heat resistance, which is a critical factor in determining their suitability for various applications. High Heat Resistance (I) TLCPs are designed to withstand extreme temperatures without losing their structural integrity. These polymers are used in applications where materials are exposed to high thermal stress, such as in automotive engine components, aerospace parts, and industrial machinery. Their ability to maintain performance at elevated temperatures makes them indispensable in these sectors. Medium Heat Resistance (II) TLCPs offer a balance between performance and cost. They are suitable for applications where moderate heat resistance is required, such as in consumer electronics and electrical components. These polymers provide sufficient thermal stability for devices that generate heat during operation, ensuring reliability and longevity. Low Heat Resistance (III) TLCPs are used in applications where heat exposure is minimal. These polymers are often chosen for their cost-effectiveness and are used in products that do not require high thermal stability, such as certain consumer goods and packaging materials. Despite their lower heat resistance, they still offer the benefits of TLCPs, such as strength and chemical resistance. The global market for TLCPs is expanding as industries recognize the advantages of these materials in enhancing product performance and durability. The demand for high heat resistance TLCPs is particularly strong in sectors where safety and reliability are paramount, such as automotive and aerospace. Medium heat resistance TLCPs are gaining traction in the electronics industry, where they are used in components that need to dissipate heat efficiently. Low heat resistance TLCPs are finding applications in cost-sensitive markets where performance requirements are less stringent. As industries continue to innovate and develop new technologies, the demand for TLCPs with varying heat resistance levels is expected to grow, driving further advancements in polymer science and engineering.

Electrical and Electronic, Industrial, Consumer Electronics, Car, Medical, Other in the Thermotropic Liquid Crystalline Polymer - Global Market:

Thermotropic Liquid Crystalline Polymers (TLCPs) are versatile materials used across various industries due to their unique properties. In the electrical and electronic sector, TLCPs are valued for their excellent dielectric properties, high thermal stability, and resistance to chemicals. They are used in connectors, switches, and other components that require reliable performance in high-temperature environments. The industrial sector benefits from TLCPs' strength and durability, making them suitable for applications such as gears, bearings, and seals. These polymers can withstand harsh conditions, reducing maintenance costs and improving equipment longevity. In consumer electronics, TLCPs are used in devices that require lightweight, durable materials, such as smartphones, tablets, and laptops. Their ability to maintain performance under thermal stress makes them ideal for components like housings and connectors. The automotive industry utilizes TLCPs in various applications, including under-the-hood components, interior parts, and electrical systems. Their high strength-to-weight ratio contributes to vehicle weight reduction, improving fuel efficiency and reducing emissions. In the medical field, TLCPs are used in devices that require biocompatibility and sterilization resistance, such as surgical instruments and diagnostic equipment. Their chemical resistance and mechanical properties ensure reliability and safety in medical applications. Other industries, such as packaging and textiles, also benefit from TLCPs' unique properties, using them to create lightweight, durable products. As the demand for high-performance materials continues to grow, TLCPs are expected to play an increasingly important role in various sectors, driving innovation and improving product performance.

Thermotropic Liquid Crystalline Polymer - Global Market Outlook:

Thermotropic Liquid Crystalline Polymers (TLCPs) are a remarkable class of high-performance polymers that combine excellent thermomechanical properties with low density, resulting in outstanding specific properties. These polymers are gaining significant attention in the global market due to their ability to deliver high performance without adding substantial weight, making them ideal for a wide range of applications. In 2023, the global market for TLCPs was valued at approximately US$ 836 million. This market is projected to grow to a readjusted size of US$ 1473.5 million by 2030, with a compound annual growth rate (CAGR) of 8.6% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for lightweight, durable materials in various industries, including electronics, automotive, and industrial applications. TLCPs are particularly valued for their high strength, stiffness, and resistance to heat and chemicals, making them suitable for demanding environments. As industries continue to seek materials that can withstand harsh conditions while maintaining structural integrity, the demand for TLCPs is expected to rise. This trend is further supported by advancements in polymer science and engineering, which are expanding the potential applications of TLCPs and driving innovation in the field.

| Report Metric | Details |

| Report Name | Thermotropic Liquid Crystalline Polymer - Market |

| Forecasted market size in 2030 | US$ 1473.5 million |

| CAGR | 8.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Vectra, Laperos, Xydar, Sumikasuper, Toray, Ueno Fine Chemicals Industry, Selcion, PRET, Vicryst |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |