What is PCB Board - Global Market?

Printed Circuit Boards (PCBs) are the backbone of modern electronic devices, serving as the foundation upon which electronic components are mounted and interconnected. The global market for PCB boards is a vast and dynamic sector, driven by the ever-increasing demand for electronic devices across various industries. PCBs are essential in the manufacturing of a wide range of products, from simple consumer electronics to complex industrial machinery. The market encompasses various types of PCBs, including single-sided, double-sided, and multilayer boards, each catering to different technological needs and applications. The growth of the PCB market is fueled by advancements in technology, such as the miniaturization of electronic components and the increasing complexity of electronic circuits. Additionally, the rise of emerging technologies like the Internet of Things (IoT), 5G, and artificial intelligence has further propelled the demand for sophisticated PCBs. As industries continue to innovate and integrate more electronics into their products, the PCB market is expected to expand, offering numerous opportunities for manufacturers and suppliers worldwide. The global PCB market is not only a reflection of technological progress but also a critical component in the supply chain of the electronics industry, underscoring its significance in the modern world.

Multilayer PCB, Single and double panels, HDI board, Others in the PCB Board - Global Market:

Multilayer PCBs, single and double panels, HDI boards, and other types of PCBs each play a unique role in the global market, catering to diverse technological requirements. Multilayer PCBs consist of multiple layers of electronic components and conductive pathways, stacked and interconnected to form a compact and efficient circuit. These boards are essential in applications where space is limited, and high performance is required, such as in smartphones, laptops, and advanced medical devices. The complexity of multilayer PCBs allows for greater functionality and reliability, making them a popular choice in high-tech industries. Single and double panels, on the other hand, are simpler in design and are typically used in less complex electronic devices. Single-sided PCBs have components on one side and are used in basic applications like calculators and remote controls. Double-sided PCBs have components on both sides, offering more flexibility and are used in slightly more complex devices like LED lighting systems and automotive dashboards. HDI (High-Density Interconnect) boards represent a more advanced type of PCB, characterized by their high wiring density per unit area. These boards are used in applications that require high-speed signal transmission and miniaturization, such as in aerospace and defense systems, as well as in cutting-edge consumer electronics. Other types of PCBs include flexible PCBs, which can be bent and shaped to fit into unconventional spaces, and rigid-flex PCBs, which combine the benefits of both rigid and flexible boards. These specialized PCBs are used in applications where durability and adaptability are crucial, such as in wearable technology and military equipment. The diversity of PCB types in the global market reflects the wide range of applications and industries that rely on these essential components, highlighting the importance of innovation and customization in meeting the evolving demands of the electronics industry.

Vehicle electronics, Consumer Electronics, Computer, Industrial control, Others in the PCB Board - Global Market:

The usage of PCB boards in various sectors such as vehicle electronics, consumer electronics, computers, industrial control, and others underscores their versatility and indispensability in modern technology. In vehicle electronics, PCBs are crucial for the functioning of various systems, including engine management, navigation, and infotainment systems. As vehicles become more technologically advanced, with features like autonomous driving and electric propulsion, the demand for sophisticated PCBs in the automotive industry continues to grow. In consumer electronics, PCBs are the foundation of devices like smartphones, tablets, and home appliances, enabling the integration of complex circuits in compact designs. The miniaturization of electronic components and the increasing functionality of consumer devices drive the need for advanced PCBs that can support high-speed data processing and connectivity. In the computer industry, PCBs are essential for the operation of motherboards, graphics cards, and other critical components, facilitating the seamless performance of personal computers, servers, and data centers. The rapid advancement of computing technology, including the rise of cloud computing and artificial intelligence, necessitates the development of PCBs that can handle increased processing power and data transfer rates. In industrial control systems, PCBs are used in machinery and equipment to ensure precise control and automation of processes. These boards must be robust and reliable to withstand harsh industrial environments and maintain consistent performance. Other sectors, such as telecommunications, healthcare, and aerospace, also rely heavily on PCBs for the development of cutting-edge technologies and systems. The versatility of PCBs allows them to be customized for specific applications, making them a critical component in the innovation and advancement of various industries. As technology continues to evolve, the role of PCBs in enabling new functionalities and improving the efficiency of electronic devices remains paramount, driving the growth and diversification of the global PCB market.

PCB Board - Global Market Outlook:

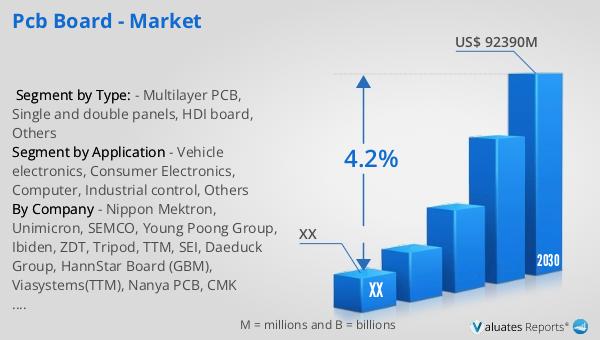

The global market for PCB boards was valued at approximately $71.57 billion in 2023, reflecting its significant role in the electronics industry. This market is projected to grow to an estimated $92.39 billion by 2030, with a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for electronic devices and the continuous advancements in technology that require sophisticated PCBs. The expansion of the PCB market is driven by several factors, including the proliferation of consumer electronics, the rise of smart technologies, and the integration of electronics in various sectors such as automotive, healthcare, and industrial automation. As industries continue to innovate and incorporate more electronic components into their products, the need for reliable and efficient PCBs becomes more critical. The projected growth of the PCB market also highlights the importance of research and development in creating new and improved PCB designs that can meet the evolving demands of the electronics industry. Manufacturers and suppliers in the PCB market are poised to benefit from this growth, as they continue to develop innovative solutions that cater to the diverse needs of their customers. The global PCB market is not only a reflection of technological progress but also a testament to the critical role that PCBs play in the advancement of modern technology.

| Report Metric | Details |

| Report Name | PCB Board - Market |

| Forecasted market size in 2030 | US$ 92390 million |

| CAGR | 4.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Nippon Mektron, Unimicron, SEMCO, Young Poong Group, Ibiden, ZDT, Tripod, TTM, SEI, Daeduck Group, HannStar Board (GBM), Viasystems(TTM), Nanya PCB, CMK Corporation, Shinko Electric Ind, Compeq, AT&S, Kingboard, Ellington, Junda Electronic, CCTC, Redboard, Wuzhu Group, Kinwong, Aoshikang, Shennan Circuits |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |