What is EV IGBT - Global Market?

The Electric Vehicle Insulated Gate Bipolar Transistor (EV IGBT) market is a crucial component of the electric vehicle industry, serving as a key element in the power electronics that drive electric motors. IGBTs are semiconductor devices that combine the advantages of both MOSFETs and bipolar transistors, offering high efficiency and fast switching capabilities. These characteristics make them ideal for managing the high power levels required in electric vehicles. The global market for EV IGBTs is experiencing significant growth due to the increasing adoption of electric vehicles worldwide. As more countries implement stringent emission regulations and promote sustainable transportation, the demand for efficient power management solutions like IGBTs is rising. This growth is further fueled by advancements in IGBT technology, which enhance the performance and reliability of electric vehicles. The market is characterized by intense competition among key players who are investing in research and development to innovate and improve their product offerings. As the electric vehicle market continues to expand, the role of IGBTs in ensuring efficient energy conversion and management becomes increasingly vital, positioning the EV IGBT market as a pivotal segment in the broader automotive industry landscape.

DC motor IGBT, AC motor IGBT, Others in the EV IGBT - Global Market:

In the realm of electric vehicles, Insulated Gate Bipolar Transistors (IGBTs) play a pivotal role in managing the power flow to both DC and AC motors, which are integral to the vehicle's propulsion system. DC motor IGBTs are specifically designed to handle the direct current that powers certain types of electric motors. These IGBTs are crucial for applications where precise control over motor speed and torque is required, such as in electric vehicles that utilize DC motors for propulsion. The ability of DC motor IGBTs to efficiently switch and manage high power levels makes them indispensable in ensuring optimal performance and energy efficiency in electric vehicles. On the other hand, AC motor IGBTs are tailored for alternating current applications, which are more common in modern electric vehicles. These IGBTs facilitate the conversion of DC power from the battery into AC power, which is then used to drive the vehicle's AC motors. The efficiency and reliability of AC motor IGBTs are critical in maximizing the range and performance of electric vehicles, as they directly impact the vehicle's energy consumption and overall driving experience. Beyond DC and AC motor applications, IGBTs are also utilized in various other components of electric vehicles, such as inverters and converters, which are essential for managing the flow of electricity between the battery and the motor. These applications highlight the versatility and importance of IGBTs in the electric vehicle ecosystem, as they enable efficient power management and contribute to the overall sustainability of electric transportation. As the global market for electric vehicles continues to grow, the demand for advanced IGBT solutions is expected to rise, driving further innovation and development in this critical area of power electronics.

Passenger Cars, Commerical Vechicle in the EV IGBT - Global Market:

The usage of EV IGBTs in passenger cars and commercial vehicles is a testament to their versatility and efficiency in managing power within electric vehicles. In passenger cars, IGBTs are primarily used in the powertrain to control the electric motor, which is responsible for propelling the vehicle. The efficiency of IGBTs in converting and managing electrical energy directly impacts the vehicle's range and performance, making them a crucial component in the design and operation of electric passenger cars. As consumers increasingly prioritize sustainability and energy efficiency, the role of IGBTs in enhancing the performance of electric passenger cars becomes even more significant. In commercial vehicles, the application of IGBTs is equally important, albeit with different priorities. Commercial vehicles, such as buses and trucks, require robust and reliable power management solutions to handle the higher power demands associated with transporting heavier loads over longer distances. IGBTs in commercial vehicles are used to manage the power flow to the electric motor, ensuring that the vehicle can operate efficiently and reliably under varying load conditions. The ability of IGBTs to handle high power levels and provide precise control over motor operation is essential in optimizing the performance and efficiency of electric commercial vehicles. Additionally, the use of IGBTs in commercial vehicles contributes to reducing emissions and operating costs, aligning with the broader industry trend towards sustainable and cost-effective transportation solutions. As the adoption of electric vehicles continues to rise across both passenger and commercial segments, the demand for advanced IGBT solutions is expected to grow, driving further innovation and development in this critical area of power electronics.

EV IGBT - Global Market Outlook:

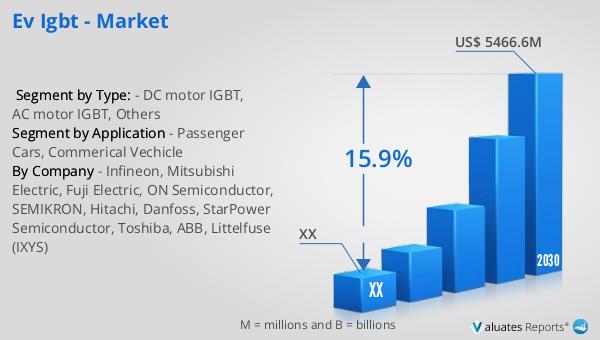

The global market for EV IGBTs was valued at approximately $2,003.6 million in 2023, and it is projected to grow significantly, reaching an estimated size of $5,466.6 million by 2030. This growth trajectory reflects a compound annual growth rate (CAGR) of 15.9% during the forecast period from 2024 to 2030. The robust expansion of the EV IGBT market is closely linked to the continued strength of global electric vehicle sales. For instance, in 2022, the sales of pure electric vehicles in Europe saw a remarkable increase of 29% year-on-year, totaling 1.58 million units. This surge in electric vehicle sales underscores the growing consumer demand for sustainable and energy-efficient transportation solutions, which in turn drives the demand for advanced power management technologies like IGBTs. As more countries implement policies to promote electric vehicle adoption and reduce carbon emissions, the market for EV IGBTs is poised for continued growth. The increasing focus on enhancing the performance and efficiency of electric vehicles further fuels the demand for innovative IGBT solutions, positioning the EV IGBT market as a key enabler of the global transition towards sustainable transportation.

| Report Metric | Details |

| Report Name | EV IGBT - Market |

| Forecasted market size in 2030 | US$ 5466.6 million |

| CAGR | 15.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Infineon, Mitsubishi Electric, Fuji Electric, ON Semiconductor, SEMIKRON, Hitachi, Danfoss, StarPower Semiconductor, Toshiba, ABB, Littelfuse (IXYS) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |