What is Steel Sandwich Sheet - Global Market?

Steel sandwich sheets are a crucial component in the construction industry, known for their unique structure and versatile applications. These sheets consist of two outer layers of steel with an insulating core sandwiched between them. This design not only provides structural strength but also offers excellent thermal insulation, making them ideal for various building applications. The global market for steel sandwich sheets is driven by the increasing demand for energy-efficient building materials. As construction standards evolve to prioritize sustainability and energy conservation, these sheets have gained popularity due to their ability to reduce energy consumption by minimizing heat transfer. Additionally, their lightweight nature and ease of installation make them a preferred choice for both residential and commercial projects. The market is also influenced by advancements in manufacturing technologies, which have improved the quality and performance of these sheets. With growing urbanization and industrialization, particularly in emerging economies, the demand for steel sandwich sheets is expected to continue rising, making them a vital component in modern construction practices.

PUR/PIR Panels, EPS Panels, Mineral Wool Panels, Others in the Steel Sandwich Sheet - Global Market:

PUR (Polyurethane) and PIR (Polyisocyanurate) panels are among the most popular types of steel sandwich sheets in the global market. These panels are renowned for their superior thermal insulation properties, which make them ideal for applications where temperature control is crucial. PUR panels are made by injecting a polyurethane foam between two steel sheets, creating a rigid and durable structure. PIR panels, on the other hand, are similar but offer enhanced fire resistance due to their chemical composition. Both types of panels are widely used in the construction of cold storage facilities, warehouses, and industrial buildings where maintaining a consistent internal temperature is essential. EPS (Expanded Polystyrene) panels are another type of steel sandwich sheet that is gaining traction in the market. These panels are lightweight and cost-effective, making them a popular choice for budget-conscious projects. EPS panels provide good thermal insulation and are often used in residential buildings, schools, and commercial structures. However, they are less fire-resistant compared to PUR and PIR panels, which can be a consideration in certain applications. Mineral wool panels are known for their excellent fire resistance and sound insulation properties. These panels are made by sandwiching a layer of mineral wool between two steel sheets, providing a robust and fire-safe solution for construction projects. They are commonly used in buildings where fire safety is a top priority, such as hospitals, schools, and high-rise buildings. The global market for steel sandwich sheets also includes other types of panels, such as those made with phenolic foam or other insulating materials. These panels offer unique benefits and are chosen based on specific project requirements. Overall, the diversity of steel sandwich sheet types allows for a wide range of applications, catering to different needs in the construction industry. As technology advances and new materials are developed, the market for these panels is expected to expand further, offering even more options for builders and architects.

Building Wall, Building Roof, Cold Storage, Others in the Steel Sandwich Sheet - Global Market:

Steel sandwich sheets are widely used in various construction applications due to their versatility and performance. In building walls, these sheets provide excellent thermal insulation, helping to maintain a comfortable indoor environment while reducing energy costs. The insulating core of the sandwich sheet minimizes heat transfer, keeping the interior warm in winter and cool in summer. This makes them an ideal choice for both residential and commercial buildings, where energy efficiency is a priority. Additionally, the steel outer layers offer durability and protection against weather elements, ensuring the longevity of the structure. For building roofs, steel sandwich sheets offer similar benefits. They provide a lightweight yet strong roofing solution that can withstand harsh weather conditions. The thermal insulation properties of these sheets help to regulate the temperature inside the building, reducing the need for excessive heating or cooling. This not only contributes to energy savings but also enhances the overall comfort of the occupants. In cold storage facilities, steel sandwich sheets are indispensable due to their superior insulation capabilities. These sheets help maintain the required low temperatures inside the storage units, ensuring the preservation of perishable goods. The use of steel sandwich sheets in cold storage construction also helps in reducing energy consumption, making them a cost-effective solution for businesses. Beyond these applications, steel sandwich sheets are used in various other areas, such as industrial buildings, warehouses, and even in the construction of temporary structures. Their ease of installation and adaptability to different designs make them a versatile choice for a wide range of projects. As the demand for energy-efficient and sustainable building materials continues to grow, the use of steel sandwich sheets is expected to increase, further solidifying their position in the global market.

Steel Sandwich Sheet - Global Market Outlook:

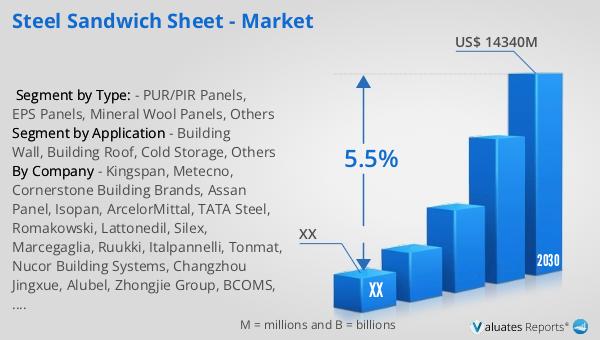

The global market for steel sandwich sheets was valued at approximately $9.8 billion in 2023, and it is projected to grow to a revised size of $14.34 billion by 2030, reflecting a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2024 to 2030. This growth is largely attributed to the increasing demand for effective insulation solutions in the construction industry. Steel sandwich sheets are highly valued for their ability to provide excellent thermal insulation, which is crucial in minimizing heat transfer between the interior and exterior of buildings. This insulation capability not only enhances energy efficiency but also contributes to the overall comfort of building occupants by maintaining a stable indoor climate. As energy costs continue to rise and environmental concerns become more pressing, the demand for energy-efficient building materials like steel sandwich sheets is expected to grow. The market's expansion is also supported by advancements in manufacturing technologies, which have improved the quality and performance of these sheets. As a result, steel sandwich sheets are becoming an increasingly popular choice for builders and architects seeking sustainable and cost-effective construction solutions.

| Report Metric | Details |

| Report Name | Steel Sandwich Sheet - Market |

| Forecasted market size in 2030 | US$ 14340 million |

| CAGR | 5.5% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kingspan, Metecno, Cornerstone Building Brands, Assan Panel, Isopan, ArcelorMittal, TATA Steel, Romakowski, Lattonedil, Silex, Marcegaglia, Ruukki, Italpannelli, Tonmat, Nucor Building Systems, Changzhou Jingxue, Alubel, Zhongjie Group, BCOMS, Isomec, Panelco, AlShahin, Dana Group, Multicolor, Pioneer India |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |