What is Global Hermetic Connectors for Semiconductor Equipment Market?

The global hermetic connectors for semiconductor equipment market is a specialized segment within the broader electronics and semiconductor industry. Hermetic connectors are designed to provide airtight seals, ensuring that no gases or liquids can penetrate the connection points. This is crucial in semiconductor manufacturing, where even the smallest contamination can lead to significant defects in the final product. These connectors are used in various semiconductor equipment to maintain the integrity of the manufacturing environment. The market for these connectors is driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, and industrial sectors. As technology advances, the need for more reliable and efficient semiconductor manufacturing processes grows, further boosting the demand for hermetic connectors. The market is characterized by a high level of innovation, with manufacturers continuously developing new products to meet the evolving needs of the semiconductor industry.

Sensor & Signal Connectors, Power Connectors, Motor Connectors, Ethernet Connectors, RF Connectors, Others in the Global Hermetic Connectors for Semiconductor Equipment Market:

Sensor and signal connectors, power connectors, motor connectors, Ethernet connectors, RF connectors, and other types of connectors play a vital role in the global hermetic connectors for semiconductor equipment market. Sensor and signal connectors are essential for transmitting data and signals within semiconductor equipment. They ensure that the equipment operates accurately and efficiently by providing reliable connections for various sensors and signal pathways. Power connectors, on the other hand, are responsible for delivering electrical power to different components of the semiconductor equipment. These connectors must be highly reliable and capable of handling high power loads to ensure the smooth operation of the equipment. Motor connectors are used to connect motors within the semiconductor equipment, enabling precise control of various mechanical movements. Ethernet connectors are crucial for networking and communication within the semiconductor manufacturing environment. They provide high-speed data transfer capabilities, ensuring that different parts of the equipment can communicate effectively. RF connectors are used for high-frequency signal transmission, which is essential in many semiconductor manufacturing processes. These connectors must provide excellent signal integrity and minimal loss to ensure accurate and reliable performance. Other types of connectors, such as those used for specific applications or custom requirements, also play a significant role in the market. Each type of connector has its unique features and specifications, tailored to meet the specific needs of semiconductor equipment. The demand for these connectors is driven by the increasing complexity and sophistication of semiconductor manufacturing processes. As the industry continues to evolve, the need for more advanced and reliable connectors will continue to grow, driving innovation and development in the market.

Etching, Sputtering, Vacuum deposition, CVD, PVD, Ion Implantation Systems, Others in the Global Hermetic Connectors for Semiconductor Equipment Market:

The usage of global hermetic connectors for semiconductor equipment is critical in various processes such as etching, sputtering, vacuum deposition, chemical vapor deposition (CVD), physical vapor deposition (PVD), ion implantation systems, and others. In etching, hermetic connectors ensure that the equipment operates in a controlled environment, preventing contamination and ensuring precise etching of semiconductor materials. Sputtering, a process used to deposit thin films on substrates, also relies on hermetic connectors to maintain the integrity of the vacuum environment. This ensures that the sputtering process is consistent and produces high-quality films. Vacuum deposition, which includes both CVD and PVD, requires hermetic connectors to maintain the vacuum conditions necessary for the deposition process. In CVD, hermetic connectors help in delivering precursor gases to the reaction chamber while preventing any leaks that could compromise the process. Similarly, in PVD, these connectors ensure that the vacuum environment is maintained, allowing for the accurate deposition of materials onto the substrate. Ion implantation systems, which are used to introduce dopants into semiconductor materials, also rely on hermetic connectors to maintain the vacuum and prevent contamination. These connectors ensure that the ion implantation process is precise and produces the desired doping levels. Other processes in semiconductor manufacturing, such as lithography and wafer bonding, also benefit from the use of hermetic connectors. These connectors help maintain the controlled environments necessary for these processes, ensuring high-quality and reliable semiconductor products. The use of hermetic connectors in these various processes highlights their importance in maintaining the integrity and reliability of semiconductor manufacturing equipment. As the demand for more advanced and reliable semiconductor devices continues to grow, the need for high-quality hermetic connectors will also increase, driving further innovation and development in the market.

Global Hermetic Connectors for Semiconductor Equipment Market Outlook:

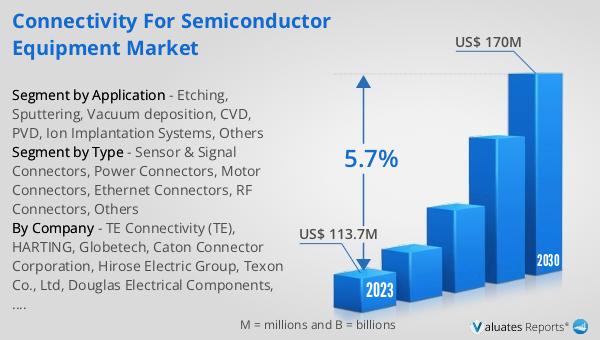

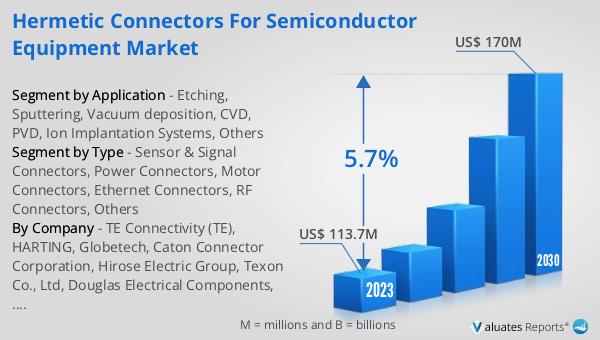

The global hermetic connectors for semiconductor equipment market was valued at US$ 113.7 million in 2023 and is expected to reach US$ 170 million by 2030, with a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2024 to 2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased by 5% from $102.6 billion in 2021 to a record $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022, despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings. This growth in the semiconductor equipment market is indicative of the increasing demand for advanced semiconductor devices and the need for reliable and efficient manufacturing processes. The market for hermetic connectors is expected to benefit from this trend, as these connectors are essential for maintaining the integrity and reliability of semiconductor manufacturing equipment. The continuous advancements in semiconductor technology and the increasing complexity of manufacturing processes are likely to drive further demand for high-quality hermetic connectors in the coming years.

| Report Metric | Details |

| Report Name | Hermetic Connectors for Semiconductor Equipment Market |

| Accounted market size in 2023 | US$ 113.7 million |

| Forecasted market size in 2030 | US$ 170 million |

| CAGR | 5.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TE Connectivity (TE), HARTING, Globetech, Caton Connector Corporation, Hirose Electric Group, Texon Co., Ltd, Douglas Electrical Components, GigaLane, JAE Electronics, Inc., CeramTec, OMRON SWITCH & DEVICES Corporation, Rosenberger Group, Winchester Interconnect, LEONI, Telit |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |