What is Global Bio-based Super Absorbent Polymer Market?

The Global Bio-based Super Absorbent Polymer Market refers to the industry focused on the production and distribution of super absorbent polymers (SAPs) derived from renewable biological sources. These polymers are designed to absorb and retain large amounts of liquid relative to their own mass. Unlike traditional SAPs, which are typically made from petroleum-based materials, bio-based SAPs are produced from renewable resources such as agricultural products and other bio-based feedstocks. This shift towards bio-based materials is driven by increasing environmental concerns, regulatory pressures, and the growing demand for sustainable and eco-friendly products. The market encompasses various applications, including personal hygiene products like diapers and feminine hygiene products, agricultural products, and other industrial uses. The adoption of bio-based SAPs is expected to grow as industries and consumers alike seek more sustainable alternatives to traditional materials.

Bio-based Propylene, Starch, Others in the Global Bio-based Super Absorbent Polymer Market:

Bio-based super absorbent polymers (SAPs) are derived from renewable resources and can be categorized into several types, including bio-based propylene, starch, and other bio-based materials. Bio-based propylene is a type of SAP that is produced from renewable sources such as corn, sugarcane, or other biomass. This type of SAP offers similar performance characteristics to traditional petroleum-based SAPs but with a reduced environmental footprint. The production process involves converting the biomass into propylene, which is then polymerized to create the super absorbent material. Starch-based SAPs, on the other hand, are derived from natural starches found in crops like corn, potatoes, and wheat. These SAPs are biodegradable and offer a sustainable alternative to synthetic polymers. The starch is chemically modified to enhance its absorbent properties, making it suitable for various applications. Other bio-based SAPs can be derived from a variety of renewable sources, including cellulose, chitosan, and other biopolymers. These materials are often chosen for their specific properties, such as biodegradability, biocompatibility, and environmental sustainability. The use of bio-based SAPs is gaining traction across different industries due to their eco-friendly nature and the growing emphasis on sustainability. As the demand for sustainable products continues to rise, the development and adoption of bio-based SAPs are expected to increase, offering a viable alternative to traditional petroleum-based polymers.

Disposable Diapers, Adult Incontinence, Feminine Hygiene, Agriculture Products, Others in the Global Bio-based Super Absorbent Polymer Market:

The Global Bio-based Super Absorbent Polymer Market finds extensive usage in various applications, including disposable diapers, adult incontinence products, feminine hygiene products, agricultural products, and other industrial uses. In the realm of disposable diapers, bio-based SAPs are used to enhance the absorbency and comfort of the diapers. These polymers can absorb and retain large amounts of liquid, keeping the baby's skin dry and reducing the risk of diaper rash. The use of bio-based SAPs in diapers also aligns with the growing demand for eco-friendly and sustainable baby products. In adult incontinence products, bio-based SAPs play a crucial role in providing superior absorbency and comfort for individuals with incontinence issues. These products are designed to absorb and lock away moisture, preventing leaks and maintaining skin health. The use of bio-based materials in these products also addresses the environmental concerns associated with traditional incontinence products. Feminine hygiene products, such as sanitary pads and tampons, also benefit from the use of bio-based SAPs. These polymers enhance the absorbency and comfort of the products, providing reliable protection during menstruation. The use of bio-based materials in feminine hygiene products is particularly important as it reduces the environmental impact of disposable products. In the agricultural sector, bio-based SAPs are used to improve soil moisture retention and enhance crop yield. These polymers can absorb and retain water, releasing it slowly to the plants as needed. This helps in reducing water usage and improving the efficiency of irrigation systems. Other industrial uses of bio-based SAPs include applications in medical products, packaging, and construction materials. The versatility and eco-friendly nature of bio-based SAPs make them suitable for a wide range of applications, driving their adoption across different industries.

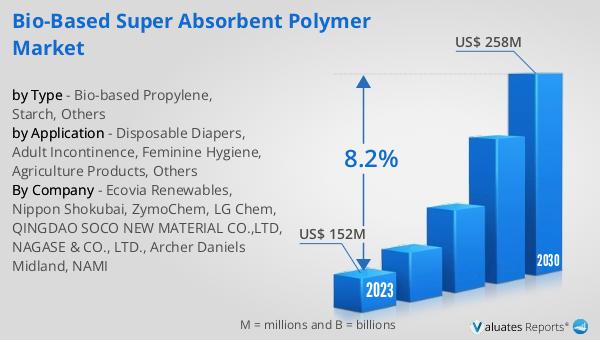

Global Bio-based Super Absorbent Polymer Market Outlook:

The global market for bio-based super absorbent polymers was valued at $152 million in 2023 and is projected to grow to $258 million by 2030, reflecting a compound annual growth rate (CAGR) of 8.2% during the forecast period from 2024 to 2030. This growth is driven by increasing environmental concerns, regulatory pressures, and the rising demand for sustainable and eco-friendly products. The shift towards bio-based materials is gaining momentum as industries and consumers alike seek alternatives to traditional petroleum-based products. The adoption of bio-based SAPs is expected to increase across various applications, including personal hygiene products, agricultural products, and other industrial uses. The market outlook indicates a positive trend towards the development and adoption of bio-based SAPs, offering a viable and sustainable alternative to traditional materials.

| Report Metric | Details |

| Report Name | Bio-based Super Absorbent Polymer Market |

| Accounted market size in 2023 | US$ 152 million |

| Forecasted market size in 2030 | US$ 258 million |

| CAGR | 8.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Ecovia Renewables, Nippon Shokubai, ZymoChem, LG Chem, QINGDAO SOCO NEW MATERIAL CO.,LTD, NAGASE & CO., LTD., Archer Daniels Midland, NAMI |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |