What is Global Marine Seismic Equipment Market?

The Global Marine Seismic Equipment Market refers to the industry that provides specialized tools and technologies used to explore and map the underwater geological structures of the Earth's crust. This market is essential for various applications, including oil and gas exploration, subsea infrastructure development, and scientific research. Marine seismic equipment helps in acquiring detailed images of sub-surface formations, which are crucial for identifying potential hydrocarbon reserves and understanding geological features. The equipment used in this market includes sub-bottom profilers, ocean bottom seismometers, geophones and hydrophones, air and water guns, among others. These tools work together to generate and capture seismic waves, which are then analyzed to create detailed maps of the underwater environment. The market is driven by the increasing demand for energy resources, advancements in technology, and the need for more accurate and efficient exploration methods. As the world continues to seek new energy sources and better understand the ocean's geology, the Global Marine Seismic Equipment Market is expected to grow and evolve, providing critical support to various industries and scientific endeavors.

Sub-Bottom Profilers, Ocean Bottom Seismometers, Geophones and Hydrophone, Air and Water Guns, Other in the Global Marine Seismic Equipment Market:

Sub-Bottom Profilers, Ocean Bottom Seismometers, Geophones and Hydrophones, Air and Water Guns, and other equipment play a vital role in the Global Marine Seismic Equipment Market. Sub-Bottom Profilers are used to penetrate the seabed and provide detailed images of the sub-surface layers. They emit sound waves that travel through the water and seabed, reflecting back to the surface to create a profile of the sub-surface structure. This information is crucial for understanding sediment layers, identifying potential drilling sites, and conducting environmental assessments. Ocean Bottom Seismometers (OBS) are deployed on the seafloor to record seismic waves generated by natural or artificial sources. They are essential for monitoring seismic activity, studying tectonic movements, and exploring underwater geological formations. OBS can operate in deep and shallow waters, providing valuable data for both scientific research and commercial exploration. Geophones and Hydrophones are sensors used to detect and measure seismic waves in the water and seabed. Geophones are typically used on land, while hydrophones are designed for underwater use. These sensors convert seismic energy into electrical signals, which are then analyzed to create detailed images of the sub-surface structures. They are crucial for identifying potential hydrocarbon reserves and understanding geological features. Air and Water Guns are used to generate seismic waves by releasing compressed air or water into the ocean. These waves travel through the water and seabed, reflecting back to the surface to be captured by sensors. Air and water guns are commonly used in seismic surveys for oil and gas exploration, providing high-resolution images of the sub-surface formations. Other equipment in the Global Marine Seismic Equipment Market includes various tools and technologies that support seismic surveys and data acquisition. These may include navigation systems, data processing software, and specialized vessels designed for seismic operations. Together, these tools and technologies enable accurate and efficient exploration of underwater geological structures, supporting various industries and scientific research. The integration of advanced technologies and continuous innovation in the field of marine seismic equipment ensures that the market remains dynamic and capable of meeting the evolving needs of its users. As the demand for energy resources and the need for detailed geological information continue to grow, the importance of these tools and technologies in the Global Marine Seismic Equipment Market cannot be overstated.

Oil and Gas, Subsea Infrastructure, Other in the Global Marine Seismic Equipment Market:

The Global Marine Seismic Equipment Market finds extensive usage in various areas, including Oil and Gas, Subsea Infrastructure, and other applications. In the Oil and Gas industry, marine seismic equipment is crucial for exploring and identifying potential hydrocarbon reserves. Seismic surveys provide detailed images of the sub-surface formations, helping geologists and engineers determine the best drilling locations and assess the potential yield of oil and gas fields. This information is vital for making informed decisions about exploration and production activities, reducing risks, and optimizing resource extraction. The use of advanced seismic equipment ensures that exploration activities are conducted efficiently and accurately, minimizing environmental impact and maximizing the chances of successful discoveries. In the Subsea Infrastructure sector, marine seismic equipment is used to map the seabed and sub-surface structures, providing essential data for the design and construction of underwater installations. This includes pipelines, cables, and other infrastructure required for the transportation of oil, gas, and other resources. Detailed seismic surveys help engineers understand the geological conditions of the seabed, identify potential hazards, and plan the safest and most efficient routes for subsea installations. This information is crucial for ensuring the stability and integrity of subsea infrastructure, reducing the risk of damage and costly repairs. Other applications of marine seismic equipment include scientific research, environmental monitoring, and disaster preparedness. Researchers use seismic surveys to study underwater geological formations, tectonic movements, and seismic activity, contributing to our understanding of the Earth's processes and natural hazards. Environmental monitoring involves assessing the impact of human activities on marine ecosystems, identifying sensitive areas, and developing strategies for conservation and sustainable use of ocean resources. In disaster preparedness, seismic equipment helps monitor and predict seismic events, such as earthquakes and tsunamis, providing early warning systems and supporting emergency response efforts. The versatility and advanced capabilities of marine seismic equipment make it an indispensable tool for various industries and applications. As technology continues to advance, the accuracy, efficiency, and range of applications for marine seismic equipment are expected to expand, further enhancing its value and importance in the Global Marine Seismic Equipment Market.

Global Marine Seismic Equipment Market Outlook:

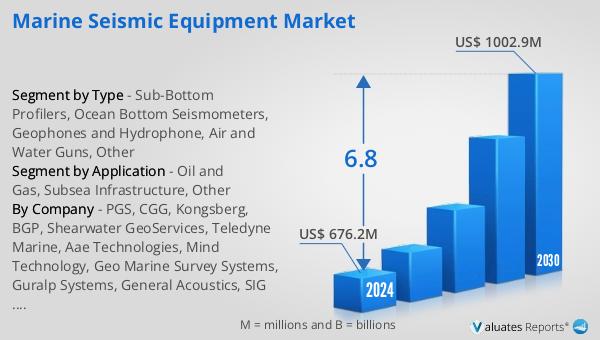

The global Marine Seismic Equipment market is anticipated to expand from US$ 676.2 million in 2024 to US$ 1002.9 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period. The market is characterized by a high level of competition, with the top four players holding approximately 40% of the market share. North America stands out as the largest market, accounting for about 34% of the global share. When it comes to product types, Ocean Bottom Seismometers represent the largest segment, making up around 20% of the market. In terms of application, the Oil and Gas sector dominates, with a substantial share of about 68%. This growth trajectory underscores the increasing demand for advanced seismic equipment to support various industries, particularly in regions with significant exploration and production activities. The market's expansion is driven by technological advancements, the need for more accurate and efficient exploration methods, and the continuous search for new energy sources. As the industry evolves, the Global Marine Seismic Equipment Market is poised to play a critical role in supporting the exploration and understanding of underwater geological structures, benefiting a wide range of applications and industries.

| Report Metric | Details |

| Report Name | Marine Seismic Equipment Market |

| Accounted market size in 2024 | US$ 676.2 million |

| Forecasted market size in 2030 | US$ 1002.9 million |

| CAGR | 6.8 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | PGS, CGG, Kongsberg, BGP, Shearwater GeoServices, Teledyne Marine, Aae Technologies, Mind Technology, Geo Marine Survey Systems, Guralp Systems, General Acoustics, SIG France |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |