What is Global Self-Sovereign Identity (SIS) System Market?

The Global Self-Sovereign Identity (SIS) System Market is a rapidly evolving sector that focuses on providing individuals with control over their digital identities. Unlike traditional identity systems where a central authority manages and verifies identities, SIS allows individuals to own, manage, and share their identity information securely and privately. This system leverages blockchain technology to ensure that identity data is tamper-proof and verifiable without the need for intermediaries. The SIS market is gaining traction due to increasing concerns over data privacy, security breaches, and the inefficiencies of centralized identity systems. By enabling users to have full control over their personal data, SIS systems aim to enhance trust and transparency in digital interactions. This market is expected to see significant growth as more industries and governments recognize the benefits of decentralized identity management.

Biometric, Non-biometric in the Global Self-Sovereign Identity (SIS) System Market:

Biometric and non-biometric methods are two primary approaches within the Global Self-Sovereign Identity (SIS) System Market. Biometric systems use unique physical characteristics such as fingerprints, facial recognition, iris scans, and voice recognition to verify an individual's identity. These methods are highly secure because they rely on attributes that are difficult to replicate or forge. For instance, fingerprint recognition is widely used in smartphones and security systems due to its accuracy and ease of use. Facial recognition technology is also gaining popularity in various sectors, including airports and financial institutions, for seamless and secure identity verification. Iris scans and voice recognition are other biometric methods that offer high levels of security and convenience. On the other hand, non-biometric methods involve the use of digital credentials, passwords, PINs, and cryptographic keys to authenticate users. These methods are often easier to implement and can be used in conjunction with biometric systems for multi-factor authentication, enhancing overall security. Digital credentials, for example, can be stored on a blockchain, ensuring that they are immutable and easily verifiable. Passwords and PINs, while traditional, are still widely used but are increasingly being supplemented with more secure methods due to their vulnerability to hacking and phishing attacks. Cryptographic keys, which are used in public-key infrastructure (PKI) systems, provide a robust method for securing digital identities by enabling encrypted communication and data exchange. Both biometric and non-biometric methods have their advantages and limitations, and the choice between them often depends on the specific requirements of the application and the level of security needed. In the SIS market, a combination of both methods is often employed to provide a balanced approach to identity verification, ensuring both security and user convenience. As technology continues to advance, we can expect to see further innovations in both biometric and non-biometric identity verification methods, driving the growth and adoption of SIS systems across various sectors.

BFSI, Government, Healthcare and Life Sciences, Telecom and IT, Retail and E-Commerce, Transport and Logistics, Media & Entertainment, Other in the Global Self-Sovereign Identity (SIS) System Market:

The Global Self-Sovereign Identity (SIS) System Market finds extensive usage across various sectors, including BFSI (Banking, Financial Services, and Insurance), Government, Healthcare and Life Sciences, Telecom and IT, Retail and E-Commerce, Transport and Logistics, Media & Entertainment, and others. In the BFSI sector, SIS systems are used to enhance the security of financial transactions, reduce fraud, and streamline customer onboarding processes. By providing a secure and verifiable way to manage digital identities, SIS systems help financial institutions comply with regulatory requirements and improve customer trust. In the government sector, SIS systems are used for secure and efficient identity management in various applications, including voting, social services, and border control. These systems help governments reduce identity fraud, improve service delivery, and enhance citizen trust. In the Healthcare and Life Sciences sector, SIS systems are used to secure patient data, streamline medical records management, and ensure compliance with data privacy regulations. By providing patients with control over their health data, SIS systems enhance patient trust and improve the efficiency of healthcare services. In the Telecom and IT sector, SIS systems are used to secure digital identities, prevent fraud, and enhance customer experience. These systems help telecom companies manage customer identities more efficiently and securely, reducing the risk of identity theft and fraud. In the Retail and E-Commerce sector, SIS systems are used to enhance customer trust, streamline authentication processes, and reduce fraud. By providing a secure and verifiable way to manage digital identities, SIS systems help retailers improve customer experience and increase sales. In the Transport and Logistics sector, SIS systems are used to secure supply chain operations, enhance tracking and tracing of goods, and improve efficiency. These systems help logistics companies reduce fraud, improve transparency, and enhance customer trust. In the Media & Entertainment sector, SIS systems are used to secure digital content, prevent piracy, and enhance user experience. By providing a secure and verifiable way to manage digital identities, SIS systems help media companies protect their content and improve customer trust. Other sectors where SIS systems are used include education, where they are used to secure student records and enhance the efficiency of administrative processes, and energy, where they are used to secure smart grid operations and enhance the efficiency of energy management. Overall, the usage of SIS systems across various sectors highlights their importance in enhancing security, improving efficiency, and building trust in digital interactions.

Global Self-Sovereign Identity (SIS) System Market Outlook:

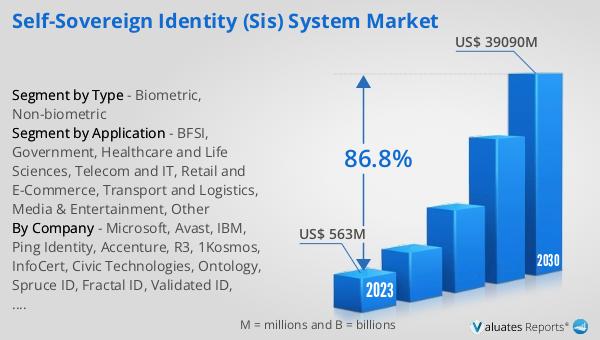

The global Self-Sovereign Identity (SIS) System market was valued at US$ 563 million in 2023 and is anticipated to reach US$ 39,090 million by 2030, witnessing a CAGR of 86.8% during the forecast period 2024-2030. This remarkable growth rate underscores the increasing recognition of the benefits of decentralized identity management systems. As concerns over data privacy and security continue to rise, more industries and governments are turning to SIS systems to provide individuals with control over their digital identities. The projected growth in the market reflects the widespread adoption of SIS systems across various sectors, including BFSI, government, healthcare, telecom, retail, transport, media, and more. The significant increase in market value from 2023 to 2030 highlights the potential of SIS systems to revolutionize identity management by enhancing security, improving efficiency, and building trust in digital interactions. As technology continues to advance and more organizations recognize the importance of secure and verifiable digital identities, the SIS market is poised for substantial growth in the coming years.

| Report Metric | Details |

| Report Name | Self-Sovereign Identity (SIS) System Market |

| Accounted market size in 2023 | US$ 563 million |

| Forecasted market size in 2030 | US$ 39090 million |

| CAGR | 86.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Microsoft, Avast, IBM, Ping Identity, Accenture, R3, 1Kosmos, InfoCert, Civic Technologies, Ontology, Spruce ID, Fractal ID, Validated ID, TrueVett (VeriME), Finema, Dock Labs, Nuggets, Affinidi, Metadium, Infopulse, Dragonchain, Serto, Datarella, Blockster Labs |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |