What is Global Residential Storage Inverter Market?

The Global Residential Storage Inverter Market refers to the industry focused on the production and distribution of inverters designed for residential energy storage systems. These inverters play a crucial role in converting the direct current (DC) generated by solar panels or stored in batteries into alternating current (AC) that can be used by household appliances. The market has seen significant growth due to the increasing adoption of renewable energy sources, particularly solar power, and the rising need for energy independence and efficiency in homes. Residential storage inverters are essential for optimizing energy usage, reducing electricity bills, and providing backup power during outages. They are available in various capacities and configurations to suit different household needs, from small apartments to large homes. The market is driven by technological advancements, government incentives for renewable energy adoption, and the growing awareness of environmental sustainability. As more homeowners seek to reduce their carbon footprint and gain control over their energy consumption, the demand for residential storage inverters is expected to continue rising.

Single-phase, Three-phase in the Global Residential Storage Inverter Market:

Single-phase and three-phase inverters are two primary types of inverters used in the Global Residential Storage Inverter Market, each serving different needs based on the household's energy requirements and the electrical infrastructure. Single-phase inverters are typically used in smaller residential settings where the energy demand is relatively low. These inverters are designed to handle a single alternating current (AC) waveform, making them suitable for homes with standard electrical setups. They are easier to install, more cost-effective, and ideal for small to medium-sized homes with basic energy needs. Single-phase inverters are often used in conjunction with smaller solar panel systems and battery storage units, providing sufficient power for daily household activities and ensuring energy efficiency. On the other hand, three-phase inverters are used in larger residential settings where the energy demand is higher. These inverters can handle three AC waveforms simultaneously, making them suitable for homes with more complex electrical setups and higher power consumption. Three-phase inverters are more efficient in distributing power across multiple circuits, reducing the risk of overloads and ensuring a stable energy supply. They are often used in larger homes with extensive electrical systems, multiple appliances, and higher energy needs. Three-phase inverters are also preferred in residential settings where the electrical infrastructure supports three-phase power, providing a more balanced and efficient energy distribution. Both single-phase and three-phase inverters play a crucial role in the Global Residential Storage Inverter Market, catering to different household needs and ensuring optimal energy usage. The choice between single-phase and three-phase inverters depends on various factors, including the size of the home, the complexity of the electrical system, and the overall energy requirements. As the demand for residential energy storage solutions continues to grow, both types of inverters are expected to see increased adoption, driven by the need for energy efficiency, cost savings, and environmental sustainability.

Small House Use, Large House Use in the Global Residential Storage Inverter Market:

The usage of Global Residential Storage Inverter Market in small house use and large house use varies significantly based on the energy requirements and the size of the household. In small house use, residential storage inverters are primarily used to optimize energy consumption and reduce electricity bills. Small houses typically have lower energy demands, making single-phase inverters an ideal choice. These inverters are easy to install, cost-effective, and provide sufficient power for daily household activities. They work in conjunction with smaller solar panel systems and battery storage units, allowing homeowners to harness solar energy, store excess power, and use it during peak hours or power outages. This not only reduces reliance on the grid but also ensures a steady supply of clean energy, contributing to environmental sustainability. In small houses, residential storage inverters help in managing energy consumption efficiently, providing backup power during outages, and reducing overall electricity costs. On the other hand, in large house use, residential storage inverters are used to meet higher energy demands and manage more complex electrical systems. Large houses often have multiple appliances, extensive electrical setups, and higher power consumption, making three-phase inverters a more suitable choice. These inverters can handle higher loads and distribute power more efficiently across multiple circuits, ensuring a stable and balanced energy supply. In large houses, residential storage inverters work with larger solar panel systems and battery storage units, providing ample power for all household needs. They help in optimizing energy usage, reducing electricity bills, and providing backup power during outages. Additionally, three-phase inverters in large houses can support advanced energy management systems, allowing homeowners to monitor and control their energy consumption more effectively. This not only enhances energy efficiency but also contributes to significant cost savings and environmental benefits. Overall, the usage of residential storage inverters in both small and large houses plays a crucial role in optimizing energy consumption, reducing electricity costs, and promoting environmental sustainability. The choice of inverter type depends on the size of the house, the complexity of the electrical system, and the overall energy requirements. As the demand for residential energy storage solutions continues to grow, the adoption of both single-phase and three-phase inverters is expected to increase, driven by the need for energy efficiency, cost savings, and environmental sustainability.

Global Residential Storage Inverter Market Outlook:

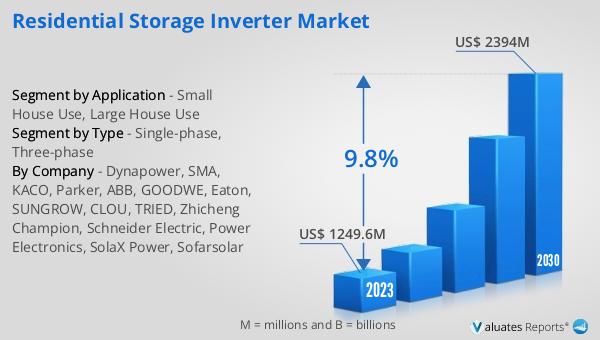

The global Residential Storage Inverter market was valued at US$ 1249.6 million in 2023 and is anticipated to reach US$ 2394 million by 2030, witnessing a CAGR of 9.8% during the forecast period 2024-2030. This significant growth reflects the increasing demand for energy-efficient solutions in residential settings. As more homeowners seek to reduce their reliance on traditional energy sources and embrace renewable energy, the market for residential storage inverters is expected to expand. These inverters play a crucial role in converting and managing the energy generated by solar panels and stored in batteries, ensuring a steady and reliable power supply for households. The rising awareness of environmental sustainability, coupled with government incentives and technological advancements, is driving the adoption of residential storage inverters. Homeowners are increasingly recognizing the benefits of these inverters in optimizing energy usage, reducing electricity bills, and providing backup power during outages. As a result, the market is poised for substantial growth in the coming years, with a projected CAGR of 9.8% from 2024 to 2030.

| Report Metric | Details |

| Report Name | Residential Storage Inverter Market |

| Accounted market size in 2023 | US$ 1249.6 million |

| Forecasted market size in 2030 | US$ 2394 million |

| CAGR | 9.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dynapower, SMA, KACO, Parker, ABB, GOODWE, Eaton, SUNGROW, CLOU, TRIED, Zhicheng Champion, Schneider Electric, Power Electronics, SolaX Power, Sofarsolar |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |