What is Global Solar EVA Sheets Market?

The Global Solar EVA Sheets Market refers to the market for Ethylene Vinyl Acetate (EVA) sheets used in solar panels. EVA sheets are crucial components in photovoltaic (PV) modules, serving as encapsulants that protect solar cells from environmental damage and mechanical stress. These sheets are sandwiched between the solar cells and the top and bottom layers of the module, providing durability and enhancing the efficiency of solar panels. The market for these sheets is expanding due to the increasing adoption of solar energy worldwide, driven by the need for sustainable and renewable energy sources. The demand for solar EVA sheets is also influenced by technological advancements in solar panel manufacturing and the growing emphasis on reducing carbon footprints. As countries and companies invest more in solar energy projects, the market for EVA sheets is expected to grow, offering opportunities for manufacturers and suppliers in the industry.

Fast-curing, Conventional, Others in the Global Solar EVA Sheets Market:

In the Global Solar EVA Sheets Market, there are different types of EVA sheets, including fast-curing, conventional, and others. Fast-curing EVA sheets are designed to speed up the manufacturing process of solar panels. These sheets have a shorter curing time, which means they can be processed more quickly during the lamination stage of solar panel production. This efficiency can lead to cost savings and increased production rates for manufacturers. Fast-curing EVA sheets are particularly beneficial in large-scale solar panel manufacturing facilities where time and efficiency are critical. Conventional EVA sheets, on the other hand, have a standard curing time and are widely used in the industry. They offer a balance between performance and cost, making them a popular choice for many solar panel manufacturers. Conventional EVA sheets provide reliable protection for solar cells and are known for their durability and long-term performance. Other types of EVA sheets may include specialized formulations designed for specific applications or environmental conditions. For example, some EVA sheets may be formulated to withstand higher temperatures or offer enhanced UV resistance. These specialized sheets can be used in solar panels deployed in extreme environments or regions with high solar radiation. The choice between fast-curing, conventional, and other types of EVA sheets depends on various factors, including the specific requirements of the solar panel manufacturer, the intended application of the solar panels, and cost considerations. Each type of EVA sheet has its own advantages and can be selected based on the desired balance between performance, cost, and manufacturing efficiency.

Residential, Commercial, Others in the Global Solar EVA Sheets Market:

The usage of Global Solar EVA Sheets Market spans across various sectors, including residential, commercial, and others. In the residential sector, EVA sheets are used in solar panels installed on rooftops of homes. These panels help homeowners generate their own electricity, reducing reliance on the grid and lowering energy bills. The use of EVA sheets in residential solar panels ensures that the solar cells are protected from environmental factors such as moisture, dust, and mechanical stress, thereby enhancing the longevity and efficiency of the panels. In the commercial sector, EVA sheets are used in larger solar installations on commercial buildings, factories, and other industrial facilities. These installations often require high-performance solar panels that can withstand harsh environmental conditions and provide reliable energy output. EVA sheets play a crucial role in ensuring the durability and performance of these panels, making them suitable for large-scale energy generation. Additionally, EVA sheets are used in solar farms and utility-scale solar projects, where thousands of solar panels are deployed to generate electricity for the grid. These large-scale projects require EVA sheets that offer excellent encapsulation properties to protect the solar cells and ensure long-term performance. Other applications of EVA sheets include their use in portable solar devices, solar-powered streetlights, and off-grid solar systems. In these applications, the protective and encapsulating properties of EVA sheets are essential to ensure the reliability and efficiency of the solar panels. Overall, the usage of EVA sheets in various sectors highlights their importance in the solar energy industry and their contribution to the growth of renewable energy solutions.

Global Solar EVA Sheets Market Outlook:

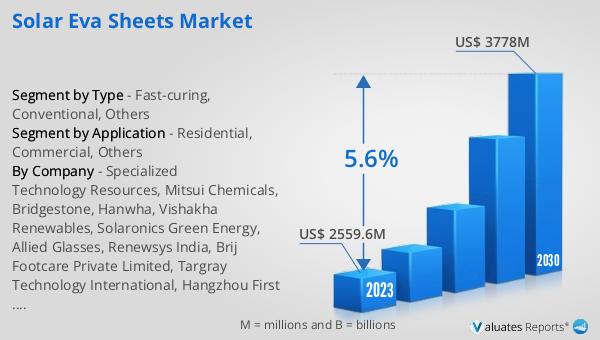

The global Solar EVA Sheets market was valued at US$ 2559.6 million in 2023 and is anticipated to reach US$ 3778 million by 2030, witnessing a CAGR of 5.6% during the forecast period 2024-2030. According to the International Energy Agency, China's market share in all key products of the supply chain has exceeded 80%. This significant market growth can be attributed to the increasing adoption of solar energy worldwide, driven by the need for sustainable and renewable energy sources. The demand for solar EVA sheets is also influenced by technological advancements in solar panel manufacturing and the growing emphasis on reducing carbon footprints. As countries and companies invest more in solar energy projects, the market for EVA sheets is expected to grow, offering opportunities for manufacturers and suppliers in the industry. The dominance of China in the supply chain highlights the strategic importance of the country in the global solar energy market. With its extensive manufacturing capabilities and technological advancements, China plays a crucial role in meeting the growing demand for solar EVA sheets and other key components of solar panels. This market outlook underscores the potential for continued growth and innovation in the solar energy sector, driven by the increasing adoption of renewable energy solutions and the need for sustainable energy sources.

| Report Metric | Details |

| Report Name | Solar EVA Sheets Market |

| Accounted market size in 2023 | US$ 2559.6 million |

| Forecasted market size in 2030 | US$ 3778 million |

| CAGR | 5.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Specialized Technology Resources, Mitsui Chemicals, Bridgestone, Hanwha, Vishakha Renewables, Solaronics Green Energy, Allied Glasses, Renewsys India, Brij Footcare Private Limited, Targray Technology International, Hangzhou First Applied Material, AKCOME, Changzhou Sveck Photovoltaic New Materials, Guangzhou Lushan New Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |