What is Global Baby Video Monitors Market?

The global Baby Video Monitors market is a rapidly growing sector that caters to the needs of modern parents who seek to ensure the safety and well-being of their infants. These devices allow parents to monitor their babies remotely, providing peace of mind and convenience. Baby video monitors come equipped with cameras and audio systems that transmit real-time video and sound to a receiver, which can be a dedicated monitor or a smartphone app. The market is driven by technological advancements, increasing awareness about child safety, and the rising number of working parents. The demand for baby video monitors is also fueled by the growing trend of nuclear families and the need for constant monitoring of infants. The market is segmented based on product type, connectivity, distribution channel, and region. Key players in the market are continuously innovating to offer advanced features such as high-definition video, night vision, temperature monitoring, and two-way communication. The global Baby Video Monitors market is expected to witness significant growth in the coming years, driven by the increasing adoption of smart home technologies and the rising disposable income of consumers.

Wired, Wireless in the Global Baby Video Monitors Market:

In the global Baby Video Monitors market, products are primarily categorized based on their connectivity options: wired and wireless. Wired baby video monitors are traditional devices that require a physical connection between the camera and the monitor. These monitors are known for their reliability and consistent performance, as they are not susceptible to interference from other wireless devices. However, the need for physical cables can limit their placement and flexibility. On the other hand, wireless baby video monitors have gained immense popularity due to their convenience and ease of installation. These monitors use Wi-Fi or other wireless technologies to transmit video and audio signals from the camera to the monitor or a smartphone app. Wireless monitors offer greater flexibility in terms of placement and mobility, allowing parents to monitor their babies from anywhere within the range of the wireless network. They also come with advanced features such as remote access, cloud storage, and integration with other smart home devices. Despite their advantages, wireless monitors can be prone to interference from other wireless devices and may require a stable internet connection for optimal performance. Both wired and wireless baby video monitors have their own set of advantages and disadvantages, and the choice between the two depends on the specific needs and preferences of the parents.

Online Sales, Offline Sales in the Global Baby Video Monitors Market:

The usage of baby video monitors in the global market can be broadly categorized into online sales and offline sales. Online sales have seen a significant surge in recent years, driven by the increasing penetration of the internet and the growing popularity of e-commerce platforms. Parents prefer online shopping for baby video monitors due to the convenience of browsing through a wide range of products, reading customer reviews, and comparing prices from the comfort of their homes. E-commerce platforms also offer attractive discounts, fast delivery options, and easy return policies, making them a preferred choice for many consumers. Additionally, the availability of detailed product descriptions, specifications, and demonstration videos helps parents make informed purchasing decisions. On the other hand, offline sales continue to hold a significant share of the market, especially in regions where internet penetration is low, or consumers prefer to physically inspect the product before making a purchase. Brick-and-mortar stores, including specialty baby stores, electronics retailers, and department stores, offer a hands-on shopping experience, allowing parents to see and test the baby video monitors in person. Sales representatives in these stores can provide personalized recommendations and assistance, helping parents choose the right product based on their specific needs. Moreover, offline sales channels often host promotional events, product demonstrations, and exclusive in-store discounts, attracting a significant number of customers. Both online and offline sales channels play a crucial role in the distribution of baby video monitors, catering to the diverse preferences and shopping behaviors of consumers.

Global Baby Video Monitors Market Outlook:

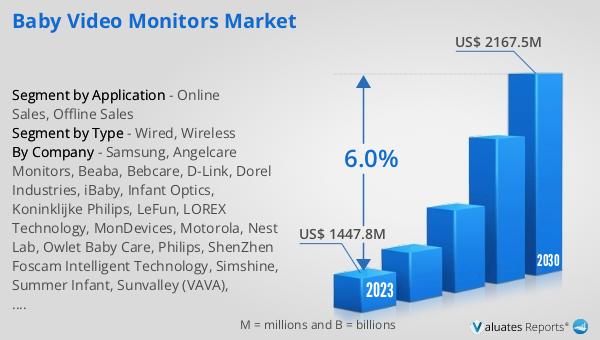

The global Baby Video Monitors market was valued at approximately US$ 1447.8 million in 2023 and is projected to reach around US$ 2167.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.0% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for baby video monitors as parents seek advanced solutions for monitoring their infants. According to the National Bureau of Statistics, China's birth rate in 2022 was 6.77%, with a birth population of 9.56 million. This demographic data underscores the potential market for baby video monitors in regions with high birth rates. The rising number of births, coupled with the growing awareness about child safety and the adoption of smart home technologies, is expected to drive the demand for baby video monitors globally. The market outlook suggests a positive trend, with continuous innovations and advancements in technology further enhancing the features and functionalities of baby video monitors, making them an essential tool for modern parenting.

| Report Metric | Details |

| Report Name | Baby Video Monitors Market |

| Accounted market size in 2023 | US$ 1447.8 million |

| Forecasted market size in 2030 | US$ 2167.5 million |

| CAGR | 6.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Samsung, Angelcare Monitors, Beaba, Bebcare, D-Link, Dorel Industries, iBaby, Infant Optics, Koninklijke Philips, LeFun, LOREX Technology, MonDevices, Motorola, Nest Lab, Owlet Baby Care, Philips, ShenZhen Foscam Intelligent Technology, Simshine, Summer Infant, Sunvalley (VAVA), Tommee Tippee, VTech Holdings, Withings |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |