What is Global Confectionery and Candy Processing Equipment Market?

The Global Confectionery and Candy Processing Equipment Market encompasses a wide array of machinery and tools specifically designed for the production and processing of sweets, chocolates, and candies. This market caters to the needs of various businesses involved in confectionery manufacturing, offering solutions to streamline operations, enhance efficiency, and improve product quality. The equipment available in this market is crucial for several stages of confectionery production, including cooking, mixing, shaping, and packaging. As the demand for confectionery products continues to rise globally, driven by changing consumer preferences and the introduction of innovative flavors and healthier options, the market for confectionery and candy processing equipment is experiencing significant growth. Manufacturers in this sector are constantly innovating and upgrading their machinery to accommodate the evolving requirements of confectionery producers, ensuring that they can meet the growing market demands efficiently. With a focus on automation, sustainability, and flexibility, the Global Confectionery and Candy Processing Equipment Market is poised for continued expansion, offering advanced solutions to confectionery manufacturers worldwide.

Coating and Enrobing Equipment, Tempering Equipment, Forming and Depositing Equipment, Extrusion Equipment, Others in the Global Confectionery and Candy Processing Equipment Market:

In the realm of the Global Confectionery and Candy Processing Equipment Market, various types of equipment play pivotal roles in the production of sweets and chocolates. Coating and Enrobing Equipment is essential for adding a finishing touch to confections, covering them in chocolate or other coatings to enhance flavor and appearance. Tempering Equipment is crucial for chocolate processing, ensuring that chocolate has the perfect texture and snap by carefully controlling temperature. Forming and Depositing Equipment allows for the precise shaping and placement of candy and chocolate into molds, enabling the production of a wide variety of shapes and sizes. Extrusion Equipment is used to create complex shapes and textures in confectionery products, such as licorice or gummy candies, by forcing the mixture through a die. Other types of equipment, including mixers, blenders, and packaging machinery, are also integral to the confectionery production process, each serving specific functions that contribute to the efficiency and quality of the final product. The diversity of equipment available in the market reflects the complexity and variety of confectionery products, catering to the needs of manufacturers to produce innovative and high-quality candies and chocolates that appeal to consumers worldwide.

Food Factory, Restaurant, Others in the Global Confectionery and Candy Processing Equipment Market:

The Global Confectionery and Candy Processing Equipment Market finds its applications in various settings, notably in food factories, restaurants, and other establishments. In food factories, this equipment is indispensable for mass-producing candies and confections, enabling manufacturers to meet the high demand for these products efficiently. The machinery's advanced technology ensures consistent quality and safety of the food items, which is paramount in large-scale production. Restaurants also benefit from smaller-scale confectionery and candy processing equipment, allowing chefs to craft unique desserts and sweets that enhance the dining experience. This equipment enables restaurants to offer freshly made, high-quality confections that can set them apart from competitors. Other areas where this equipment is used include small bakeries, boutique confectionery shops, and even in educational settings where culinary arts are taught. These diverse applications underscore the versatility and importance of confectionery and candy processing equipment in not only supporting the commercial production of sweets but also in enriching the culinary landscape by enabling the creation of innovative and delightful treats.

Global Confectionery and Candy Processing Equipment Market Outlook:

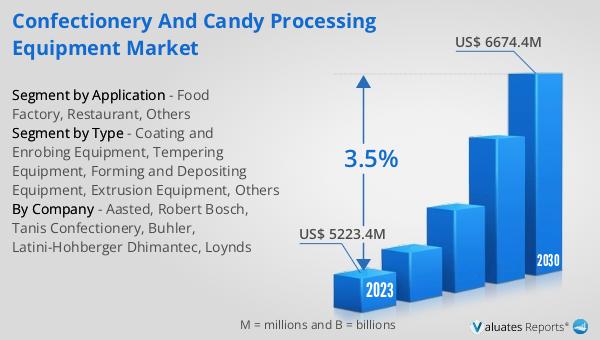

The market outlook for the Global Confectionery and Candy Processing Equipment Market reveals a promising trajectory. As of 2023, the market's valuation stood at approximately $5223.4 million. Looking ahead, projections indicate a growth trend, with expectations to reach around $6674.4 million by the year 2030. This anticipated growth, marked by a compound annual growth rate (CAGR) of 3.5% during the forecast period from 2024 to 2030, underscores the dynamic nature of the confectionery and candy processing equipment sector. Such growth can be attributed to various factors, including technological advancements in equipment, rising global demand for confectionery products, and the industry's adaptation to changing consumer preferences towards more innovative and healthier snack options. This outlook reflects the sector's potential for expansion and the increasing importance of efficient, high-quality processing equipment in meeting the evolving needs of the confectionery industry.

| Report Metric | Details |

| Report Name | Confectionery and Candy Processing Equipment Market |

| Accounted market size in 2023 | US$ 5223.4 million |

| Forecasted market size in 2030 | US$ 6674.4 million |

| CAGR | 3.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Aasted, Robert Bosch, Tanis Confectionery, Buhler, Latini-Hohberger Dhimantec, Loynds |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |