What is Global Underfills for Semiconductor Market?

The Global Underfills for Semiconductor Market is a crucial segment within the electronics industry, focusing on materials used to enhance the reliability and performance of semiconductor devices. Underfills are specialized materials applied to fill the gaps between a semiconductor chip and its substrate, providing mechanical support and protection against environmental factors. These materials are essential in preventing mechanical stress and thermal expansion, which can lead to device failure. The market for underfills is driven by the increasing demand for miniaturized electronic devices, which require more robust and reliable packaging solutions. As technology advances, the need for efficient heat dissipation and mechanical stability in semiconductor devices becomes more critical, further propelling the demand for underfills. The market encompasses various types of underfills, including capillary underfills, no-flow underfills, and molded underfills, each catering to specific applications and requirements. With the continuous evolution of semiconductor technology, the Global Underfills for Semiconductor Market is poised for significant growth, driven by innovations in material science and the increasing complexity of electronic devices. This market plays a vital role in ensuring the longevity and performance of semiconductors, which are integral to modern electronic systems.

Chip-on-film Underfills, Flip Chip Underfills, CSP/BGA Board Level Underfills in the Global Underfills for Semiconductor Market:

Chip-on-film underfills, flip chip underfills, and CSP/BGA board level underfills are integral components of the Global Underfills for Semiconductor Market, each serving distinct roles in enhancing the performance and reliability of semiconductor devices. Chip-on-film underfills are used primarily in applications where flexibility and lightweight characteristics are essential, such as in display technologies and flexible electronics. These underfills provide the necessary mechanical support and thermal management to ensure the durability of the chip-on-film assemblies, which are often subjected to bending and flexing during use. Flip chip underfills, on the other hand, are crucial in high-performance computing and communication devices. They are applied to fill the gaps between the flip chip and the substrate, providing a robust mechanical bond and enhancing thermal conductivity. This is particularly important in applications where high power and heat dissipation are critical, such as in processors and graphic chips. CSP/BGA board level underfills are used in chip-scale packages and ball grid arrays, which are common in consumer electronics and automotive applications. These underfills help in distributing mechanical stress evenly across the board, preventing solder joint failures and enhancing the overall reliability of the device. The choice of underfill material and application method is critical, as it directly impacts the performance and longevity of the semiconductor device. Each type of underfill has its unique properties and advantages, making them suitable for specific applications and environments. The development of advanced underfill materials with improved thermal and mechanical properties is a key focus area in the industry, driven by the need for more reliable and efficient semiconductor packaging solutions. As the demand for smaller, faster, and more efficient electronic devices continues to grow, the role of underfills in ensuring the performance and reliability of semiconductor devices becomes increasingly important. The Global Underfills for Semiconductor Market is characterized by continuous innovation and development, with manufacturers focusing on creating materials that meet the evolving needs of the electronics industry. This includes the development of underfills with enhanced thermal conductivity, lower viscosity, and improved adhesion properties, which are essential for the next generation of semiconductor devices. The market is also influenced by the increasing adoption of advanced packaging technologies, such as 3D packaging and system-in-package, which require more sophisticated underfill solutions. As a result, the Global Underfills for Semiconductor Market is expected to witness significant growth, driven by the increasing complexity and performance requirements of modern electronic devices.

Industrial Electronics, Defense & Aerospace Electronics, Consumer Electronics, Automotive Electronics, Medical Electronics, Others in the Global Underfills for Semiconductor Market:

The usage of Global Underfills for Semiconductor Market spans across various sectors, including industrial electronics, defense and aerospace electronics, consumer electronics, automotive electronics, medical electronics, and others. In industrial electronics, underfills are used to enhance the reliability and performance of devices that operate in harsh environments, such as factory automation systems and power electronics. These applications require robust underfill materials that can withstand high temperatures and mechanical stress, ensuring the longevity and efficiency of the devices. In defense and aerospace electronics, underfills play a critical role in ensuring the reliability and performance of mission-critical systems. These applications demand high-performance underfill materials that can withstand extreme temperatures, vibrations, and mechanical stress, ensuring the reliability and performance of the devices in challenging environments. In consumer electronics, underfills are used to enhance the performance and reliability of devices such as smartphones, tablets, and wearable devices. These applications require underfill materials that provide excellent thermal management and mechanical support, ensuring the longevity and performance of the devices. In automotive electronics, underfills are used to enhance the reliability and performance of electronic systems in vehicles, such as engine control units, infotainment systems, and advanced driver-assistance systems. These applications require underfill materials that can withstand high temperatures and mechanical stress, ensuring the reliability and performance of the devices in challenging environments. In medical electronics, underfills are used to enhance the reliability and performance of devices such as diagnostic equipment, monitoring systems, and implantable devices. These applications require underfill materials that provide excellent thermal management and mechanical support, ensuring the longevity and performance of the devices. The Global Underfills for Semiconductor Market is characterized by continuous innovation and development, with manufacturers focusing on creating materials that meet the evolving needs of the electronics industry. This includes the development of underfills with enhanced thermal conductivity, lower viscosity, and improved adhesion properties, which are essential for the next generation of semiconductor devices. As the demand for smaller, faster, and more efficient electronic devices continues to grow, the role of underfills in ensuring the performance and reliability of semiconductor devices becomes increasingly important. The market is also influenced by the increasing adoption of advanced packaging technologies, such as 3D packaging and system-in-package, which require more sophisticated underfill solutions. As a result, the Global Underfills for Semiconductor Market is expected to witness significant growth, driven by the increasing complexity and performance requirements of modern electronic devices.

Global Underfills for Semiconductor Market Outlook:

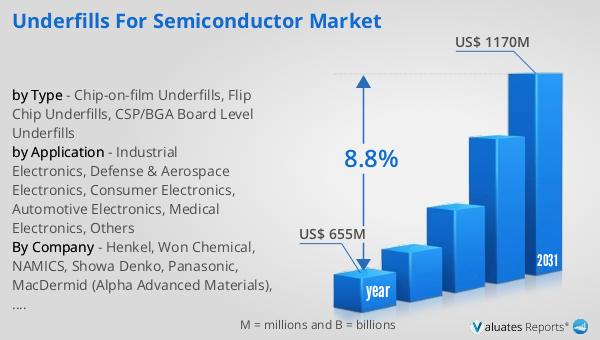

In 2024, the global market for underfills used in semiconductors was valued at approximately $655 million. By 2031, this market is anticipated to expand to a revised size of around $1,170 million, reflecting a compound annual growth rate (CAGR) of 8.8% over the forecast period. This growth trajectory underscores the increasing demand for underfills, driven by advancements in semiconductor technology and the rising need for reliable and efficient electronic devices. The market is characterized by a high level of concentration, with the top three manufacturers collectively holding a market share exceeding 50%. This concentration indicates a competitive landscape where leading companies are leveraging their technological expertise and innovation capabilities to maintain their market positions. The growth of the Global Underfills for Semiconductor Market is fueled by the continuous evolution of electronic devices, which require more sophisticated packaging solutions to enhance performance and reliability. As the demand for miniaturized and high-performance electronic devices continues to rise, the role of underfills in ensuring the longevity and efficiency of semiconductor devices becomes increasingly critical. The market is also influenced by the increasing adoption of advanced packaging technologies, such as 3D packaging and system-in-package, which require more sophisticated underfill solutions. As a result, the Global Underfills for Semiconductor Market is expected to witness significant growth, driven by the increasing complexity and performance requirements of modern electronic devices.

| Report Metric | Details |

| Report Name | Underfills for Semiconductor Market |

| Accounted market size in year | US$ 655 million |

| Forecasted market size in 2031 | US$ 1170 million |

| CAGR | 8.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Henkel, Won Chemical, NAMICS, Showa Denko, Panasonic, MacDermid (Alpha Advanced Materials), Shin-Etsu, Sunstar, Fuji Chemical, Zymet, Shenzhen Dover, Threebond, AIM Solder, Darbond, Master Bond, Hanstars, Nagase ChemteX, LORD Corporation, Asec Co., Ltd., Everwide Chemical, Bondline, Panacol-Elosol, United Adhesives, U-Bond, Shenzhen Cooteck Electronic Material Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |