What is Global Nuclear Industry Grade Boron Isotopes Market?

The Global Nuclear Industry Grade Boron Isotopes Market is a specialized segment within the broader chemical and nuclear industries, focusing on the production and application of boron isotopes, particularly boron-10. Boron isotopes are critical due to their unique nuclear properties, which make them indispensable in various high-tech and industrial applications. The market is driven by the demand for nuclear-grade boron isotopes, which are essential for controlling nuclear reactions in power plants and other nuclear facilities. These isotopes are also used in radiation shielding and neutron capture therapy, a form of cancer treatment. The market's growth is influenced by the increasing need for clean energy solutions, advancements in nuclear technology, and the expanding applications of boron isotopes in fields such as semiconductors and medical research. As industries continue to innovate and seek more efficient and sustainable solutions, the demand for high-purity boron isotopes is expected to rise, making this market a crucial component of the global industrial landscape. The market's complexity is further compounded by the technical challenges associated with isotope separation and the stringent regulatory requirements governing their use.

Liquid, Solid, Gaseous in the Global Nuclear Industry Grade Boron Isotopes Market:

In the Global Nuclear Industry Grade Boron Isotopes Market, boron isotopes are available in various forms, including liquid, solid, and gaseous states, each serving distinct purposes and applications. Liquid boron isotopes are often used in chemical processes where precise control over concentration and reactivity is required. These isotopes can be dissolved in solvents to create solutions that are easily integrated into various industrial processes. The liquid form is particularly advantageous in applications where uniform distribution and rapid reaction rates are necessary, such as in certain types of chemical synthesis and nuclear reactor cooling systems. Solid boron isotopes, on the other hand, are typically used in applications requiring stable, long-term performance. These include neutron shielding materials, where boron is incorporated into solid matrices to absorb neutrons and protect sensitive equipment and personnel from radiation. Solid forms are also used in the manufacturing of semiconductors, where boron is implanted into silicon wafers to modify their electrical properties. The solid state offers durability and ease of handling, making it suitable for applications where physical stability is paramount. Gaseous boron isotopes are less common but are used in specialized applications where high diffusion rates and low densities are required. These include certain types of nuclear reactors and advanced research facilities where boron gas can be used to study nuclear reactions and material interactions at the atomic level. The gaseous form allows for rapid mixing and interaction with other gases, providing unique opportunities for experimentation and innovation. Each form of boron isotope presents its own set of challenges and advantages, influencing their selection based on the specific requirements of the application. The choice between liquid, solid, and gaseous forms depends on factors such as the desired reactivity, stability, and ease of integration into existing systems. As the demand for boron isotopes continues to grow, advancements in production and processing technologies are expected to enhance the availability and versatility of these materials, further expanding their applications across various industries.

Nuclear Power, Semiconductors, Others in the Global Nuclear Industry Grade Boron Isotopes Market:

The usage of Global Nuclear Industry Grade Boron Isotopes Market spans several critical areas, including nuclear power, semiconductors, and other specialized fields. In the nuclear power sector, boron isotopes, particularly boron-10, play a vital role in controlling nuclear reactions. They are used as neutron absorbers in nuclear reactors, helping to regulate the fission process and maintain safe operating conditions. This application is crucial for the efficient and safe generation of nuclear energy, as boron isotopes help prevent the reactor from reaching criticality and ensure a stable energy output. In the semiconductor industry, boron isotopes are used in the doping process, where they are introduced into silicon wafers to alter their electrical properties. This process is essential for the production of various electronic components, including transistors and integrated circuits, which form the backbone of modern electronic devices. The precise control over the electrical characteristics of semiconductors enabled by boron isotopes is critical for the development of faster, more efficient, and more reliable electronic products. Beyond nuclear power and semiconductors, boron isotopes find applications in other areas such as medical research and treatment. In neutron capture therapy, a form of cancer treatment, boron-10 is used to target and destroy cancer cells with minimal damage to surrounding healthy tissue. This innovative approach leverages the unique nuclear properties of boron isotopes to provide a targeted and effective treatment option for certain types of cancer. Additionally, boron isotopes are used in the production of advanced materials and coatings, where their unique properties can enhance the performance and durability of the final product. The versatility and effectiveness of boron isotopes in these diverse applications underscore their importance in modern industry and research. As technology continues to advance, the demand for high-purity boron isotopes is expected to grow, driving further innovation and development in this dynamic market.

Global Nuclear Industry Grade Boron Isotopes Market Outlook:

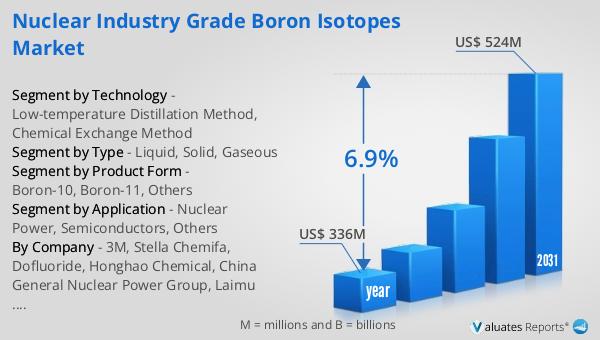

The global market for Nuclear Industry Grade Boron Isotopes was valued at $336 million in 2024 and is anticipated to expand to a revised size of $524 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.9% over the forecast period. This growth trajectory underscores the increasing importance and demand for boron isotopes, particularly boron-10, which is central to this market. Boron-10 has a natural abundance of just 19.78%, making its extraction and refinement a complex and specialized process. The rising demand is driven by its critical applications in nuclear power generation, where it serves as a neutron absorber, and in the semiconductor industry, where it is used in doping processes to enhance the performance of electronic components. Additionally, boron isotopes are gaining traction in medical applications, such as neutron capture therapy for cancer treatment, further contributing to market growth. The market's expansion is also supported by advancements in production technologies and the increasing emphasis on clean energy solutions, which are driving the adoption of nuclear power as a sustainable energy source. As industries continue to innovate and seek more efficient and sustainable solutions, the demand for high-purity boron isotopes is expected to rise, making this market a crucial component of the global industrial landscape. The market's complexity is further compounded by the technical challenges associated with isotope separation and the stringent regulatory requirements governing their use.

| Report Metric | Details |

| Report Name | Nuclear Industry Grade Boron Isotopes Market |

| Accounted market size in year | US$ 336 million |

| Forecasted market size in 2031 | US$ 524 million |

| CAGR | 6.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Product Form |

|

| Segment by Technology |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | 3M, Stella Chemifa, Dofluoride, Honghao Chemical, China General Nuclear Power Group, Laimu Technology, Rosatom, Westinghouse |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |