What is Global STATCOM Systems Market?

The Global STATCOM Systems Market refers to the worldwide industry focused on the development, production, and deployment of Static Synchronous Compensators (STATCOMs). These systems are crucial in modern electrical grids as they help maintain voltage stability and improve power quality. STATCOMs are advanced power electronic devices that provide fast and efficient reactive power compensation, which is essential for stabilizing voltage levels in power systems. They are particularly valuable in scenarios where power demand fluctuates rapidly, such as in renewable energy integration and industrial applications. The market for STATCOM systems is expanding due to the increasing demand for reliable and efficient power supply solutions, driven by the growing adoption of renewable energy sources and the need for modernizing aging power infrastructure. As countries worldwide invest in upgrading their electrical grids to accommodate new energy sources and improve overall efficiency, the demand for STATCOM systems is expected to rise, making it a significant area of focus for companies involved in power electronics and grid management.

High Voltage STATCOM, Low Voltage STATCOM in the Global STATCOM Systems Market:

High Voltage STATCOM and Low Voltage STATCOM are two primary categories within the Global STATCOM Systems Market, each serving distinct roles based on their voltage handling capabilities. High Voltage STATCOMs are designed for large-scale power systems, typically used in transmission networks where they help stabilize voltage levels over long distances. These systems are crucial in managing the reactive power flow in high voltage transmission lines, ensuring that the power supply remains stable and efficient. They are often deployed in areas with significant renewable energy generation, such as wind farms and solar power plants, where they help mitigate the variability in power output. High Voltage STATCOMs are also essential in interconnecting different power grids, allowing for the seamless transfer of electricity across regions and countries. On the other hand, Low Voltage STATCOMs are used in distribution networks and industrial applications where the voltage levels are lower. These systems are vital in maintaining power quality in local grids, particularly in urban areas with dense populations and high electricity demand. Low Voltage STATCOMs help reduce voltage fluctuations and improve the overall reliability of the power supply, making them indispensable in industries that require a stable power source for their operations. They are also used in commercial buildings and data centers, where maintaining a consistent power supply is critical to prevent disruptions. Both High Voltage and Low Voltage STATCOMs play a crucial role in enhancing the efficiency and reliability of power systems, making them integral components of modern electrical grids. As the demand for electricity continues to grow and the integration of renewable energy sources becomes more prevalent, the need for advanced STATCOM systems is expected to increase, driving innovation and development in this field.

Electric Utilities, Renewable Energy, Industrial & Manufacturing, Others in the Global STATCOM Systems Market:

The Global STATCOM Systems Market finds its applications across various sectors, including Electric Utilities, Renewable Energy, Industrial & Manufacturing, and others. In the Electric Utilities sector, STATCOM systems are used to enhance the stability and reliability of power transmission and distribution networks. They help manage reactive power flow, reduce transmission losses, and improve voltage stability, which is crucial for maintaining a consistent power supply to consumers. In the Renewable Energy sector, STATCOM systems play a vital role in integrating renewable energy sources into the grid. They help manage the variability in power output from sources like wind and solar, ensuring that the electricity generated is efficiently transmitted and distributed. This is particularly important as the share of renewable energy in the global energy mix continues to grow. In the Industrial & Manufacturing sector, STATCOM systems are used to maintain power quality and ensure the smooth operation of machinery and equipment. They help reduce voltage fluctuations and improve the overall efficiency of industrial processes, which is essential for minimizing downtime and maximizing productivity. Other sectors that benefit from STATCOM systems include transportation, where they are used in electrified railways to maintain voltage stability, and data centers, where they ensure a reliable power supply to critical infrastructure. Overall, the Global STATCOM Systems Market is driven by the need for efficient and reliable power solutions across various industries, making it a key area of focus for companies involved in power electronics and grid management.

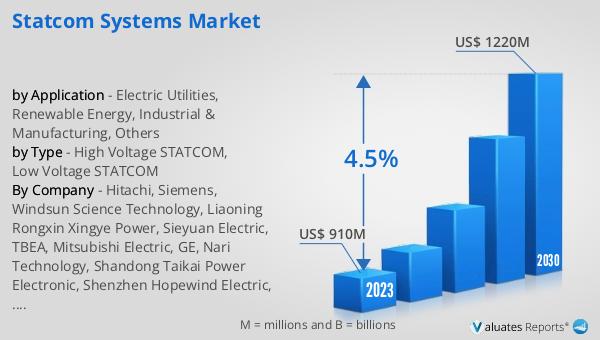

Global STATCOM Systems Market Outlook:

The outlook for the Global STATCOM Systems Market indicates a promising growth trajectory, with the market expected to expand from US$ 936 million in 2024 to US$ 1270 million by 2031. This growth, at a compound annual growth rate (CAGR) of 4.5% from 2025 to 2031, is fueled by the increasing demand for STATCOM systems across various critical product segments and diverse end-use applications. As the world continues to transition towards renewable energy sources and modernize its power infrastructure, the need for advanced power management solutions like STATCOM systems is becoming more pronounced. These systems are essential for maintaining voltage stability and improving power quality in electrical grids, making them indispensable in sectors such as electric utilities, renewable energy, and industrial manufacturing. However, the market also faces challenges, particularly with evolving U.S. tariff policies that introduce trade-cost volatility and supply-chain uncertainty. These factors could impact the cost and availability of STATCOM systems, influencing market dynamics and competitive strategies. Despite these challenges, the overall outlook for the Global STATCOM Systems Market remains positive, driven by the ongoing demand for efficient and reliable power solutions in an increasingly electrified world.

| Report Metric | Details |

| Report Name | STATCOM Systems Market |

| Accounted market size in 2024 | US$ 936 million |

| Forecasted market size in 2031 | US$ 1270 million |

| CAGR | 4.5% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Hitachi, Siemens, Windsun Science Technology, Liaoning Rongxin Xingye Power, Sieyuan Electric, TBEA, Mitsubishi Electric, GE, Nari Technology, Shandong Taikai Power Electronic, Shenzhen Hopewind Electric, American Superconductor, Ingeteam, Beijing In-power Electric |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |