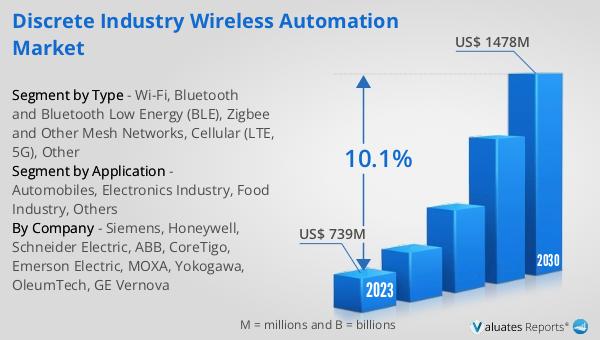

What is Global Process Industry Wireless Automation Market?

The Global Process Industry Wireless Automation Market refers to the integration of wireless technologies in various industrial processes to enhance efficiency, safety, and productivity. This market encompasses a wide range of wireless communication technologies that are used to automate and streamline operations in industries such as oil and gas, petrochemicals, energy, and more. Wireless automation allows for real-time data collection and monitoring, enabling industries to make informed decisions quickly. It reduces the need for extensive wiring, which can be costly and time-consuming to install and maintain. By leveraging wireless technologies, industries can achieve greater flexibility and scalability in their operations. This market is driven by the increasing demand for efficient and cost-effective solutions to manage complex industrial processes. As industries continue to evolve and embrace digital transformation, the adoption of wireless automation technologies is expected to grow, offering numerous benefits such as improved operational efficiency, reduced downtime, and enhanced safety. The Global Process Industry Wireless Automation Market is a critical component of the broader industrial automation landscape, playing a vital role in the modernization of industrial processes worldwide.

Wi-Fi, Bluetooth and Bluetooth Low Energy (BLE), Zigbee and Other Mesh Networks, Cellular (LTE, 5G), Other in the Global Process Industry Wireless Automation Market:

In the Global Process Industry Wireless Automation Market, several wireless communication technologies play a pivotal role in enhancing industrial operations. Wi-Fi is one of the most widely used technologies, offering high-speed internet connectivity and data transfer capabilities. It is particularly useful in environments where a stable and fast connection is required for real-time monitoring and control. Wi-Fi networks can support a large number of devices, making them ideal for complex industrial setups. Bluetooth and Bluetooth Low Energy (BLE) are also significant players in this market. Bluetooth is known for its short-range communication capabilities, making it suitable for connecting devices within a limited area. BLE, on the other hand, is designed for low power consumption, making it ideal for battery-operated devices that require long-term connectivity without frequent recharging. Zigbee and other mesh networks are crucial for creating robust and reliable communication networks in industrial settings. These technologies enable devices to communicate with each other in a mesh topology, ensuring that data can be transmitted even if some nodes in the network fail. This makes them highly reliable for critical industrial applications where uninterrupted communication is essential. Cellular technologies, including LTE and 5G, are increasingly being adopted in the Global Process Industry Wireless Automation Market. LTE provides high-speed data transfer and wide coverage, making it suitable for remote monitoring and control of industrial processes. 5G, with its ultra-low latency and high bandwidth, is set to revolutionize industrial automation by enabling real-time data processing and advanced applications such as augmented reality and remote robotics. Other wireless technologies, such as LoRaWAN and Sigfox, are also gaining traction in this market. These technologies are designed for long-range communication with low power consumption, making them ideal for applications that require wide-area coverage and minimal energy usage. In summary, the Global Process Industry Wireless Automation Market is characterized by a diverse range of wireless communication technologies, each offering unique advantages for industrial applications. These technologies enable industries to achieve greater efficiency, flexibility, and reliability in their operations, driving the adoption of wireless automation solutions across various sectors.

Oil and Gas Industry, Petrochemical Industry, Energy Industry, Other in the Global Process Industry Wireless Automation Market:

The Global Process Industry Wireless Automation Market finds extensive usage across various industries, including oil and gas, petrochemicals, energy, and others. In the oil and gas industry, wireless automation technologies are used to monitor and control drilling operations, pipeline management, and refinery processes. These technologies enable real-time data collection and analysis, allowing operators to make informed decisions quickly and efficiently. Wireless sensors and communication networks help in monitoring equipment health, detecting leaks, and ensuring safety compliance, thereby reducing the risk of accidents and downtime. In the petrochemical industry, wireless automation plays a crucial role in optimizing production processes and ensuring product quality. Wireless technologies enable seamless communication between different stages of production, allowing for precise control and monitoring of chemical reactions and processes. This results in improved efficiency, reduced waste, and enhanced safety. Wireless automation also facilitates predictive maintenance, helping to identify potential equipment failures before they occur and minimizing unplanned downtime. The energy industry also benefits significantly from wireless automation technologies. In power generation and distribution, wireless communication networks enable real-time monitoring and control of equipment, ensuring efficient operation and reducing energy losses. Wireless sensors are used to monitor environmental conditions, equipment performance, and energy consumption, providing valuable insights for optimizing energy usage and reducing costs. Additionally, wireless automation supports the integration of renewable energy sources into the grid, enabling more flexible and sustainable energy management. Other industries, such as manufacturing, pharmaceuticals, and food and beverage, also leverage wireless automation technologies to enhance their operations. In manufacturing, wireless communication networks enable seamless integration of production lines, improving efficiency and reducing downtime. In the pharmaceutical industry, wireless sensors and monitoring systems ensure compliance with regulatory standards and maintain product quality. In the food and beverage industry, wireless automation helps in monitoring production processes, ensuring food safety, and optimizing supply chain management. Overall, the Global Process Industry Wireless Automation Market offers numerous benefits across various industries, driving the adoption of wireless technologies to enhance efficiency, safety, and productivity.

Global Process Industry Wireless Automation Market Outlook:

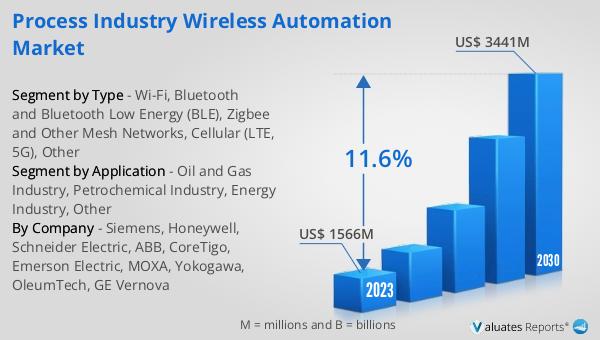

The outlook for the Global Process Industry Wireless Automation Market is promising, with significant growth anticipated in the coming years. The market is expected to expand from $1,781 million in 2024 to $3,800 million by 2031, reflecting a compound annual growth rate (CAGR) of 11.6% from 2025 to 2031. This growth is driven by the increasing demand for wireless automation solutions across various industries, including oil and gas, petrochemicals, energy, and more. The adoption of wireless technologies is fueled by the need for efficient and cost-effective solutions to manage complex industrial processes. As industries continue to embrace digital transformation, the demand for wireless automation technologies is expected to rise, offering numerous benefits such as improved operational efficiency, reduced downtime, and enhanced safety. The market is characterized by a diverse range of wireless communication technologies, each offering unique advantages for industrial applications. These technologies enable industries to achieve greater efficiency, flexibility, and reliability in their operations, driving the adoption of wireless automation solutions across various sectors. As the market continues to evolve, it is expected to play a vital role in the modernization of industrial processes worldwide, offering significant opportunities for growth and innovation.

| Report Metric | Details |

| Report Name | Process Industry Wireless Automation Market |

| Accounted market size in 2024 | US$ 1781 in million |

| Forecasted market size in 2031 | US$ 3800 million |

| CAGR | 11.6% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Sales by Region |

|

| By Company | Siemens, Honeywell, Schneider Electric, ABB, CoreTigo, Emerson Electric, MOXA, Yokogawa, OleumTech, GE Vernova |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |