What is Global Vacuum Ceramic Hands Market?

The Global Vacuum Ceramic Hands Market is a niche yet crucial segment within the broader industrial and technological landscape. These ceramic hands are specialized tools used primarily in the semiconductor industry for handling delicate wafers during manufacturing processes. The term "vacuum" refers to the method by which these hands grip and move the wafers, utilizing suction to ensure a secure hold without causing damage. Ceramic materials are chosen for their unique properties, such as high thermal resistance, electrical insulation, and minimal particle generation, which are essential in maintaining the integrity and cleanliness of semiconductor wafers. As the demand for semiconductors continues to rise, driven by advancements in technology and increased consumer electronics usage, the need for efficient and reliable wafer handling solutions like vacuum ceramic hands is also growing. These tools play a pivotal role in ensuring the precision and efficiency of semiconductor manufacturing, ultimately contributing to the production of high-quality electronic components that power a wide range of devices and applications. The market for vacuum ceramic hands is expected to expand as industries continue to innovate and seek out more sophisticated manufacturing solutions.

Alumina Wafer Hands, Silicon Carbide Wafer Hands, Corseed Wafer Hands in the Global Vacuum Ceramic Hands Market:

Alumina Wafer Hands, Silicon Carbide Wafer Hands, and Corseed Wafer Hands are integral components of the Global Vacuum Ceramic Hands Market, each offering distinct advantages tailored to specific applications within the semiconductor industry. Alumina Wafer Hands are crafted from aluminum oxide, a material known for its excellent thermal stability and electrical insulation properties. These characteristics make alumina an ideal choice for environments where high temperatures and electrical conductivity could pose challenges. Alumina Wafer Hands are particularly valued for their durability and resistance to wear, ensuring long-term performance in demanding manufacturing settings. They are often used in processes where maintaining the purity and integrity of the wafer is paramount, as alumina's low particle generation helps prevent contamination. Silicon Carbide Wafer Hands, on the other hand, are made from silicon carbide, a material renowned for its exceptional hardness and thermal conductivity. These properties make silicon carbide an excellent choice for applications requiring high strength and resistance to thermal shock. Silicon Carbide Wafer Hands are particularly suited for environments where rapid temperature changes occur, as they can withstand such fluctuations without compromising their structural integrity. Additionally, their high thermal conductivity allows for efficient heat dissipation, which is crucial in processes where temperature control is critical. This makes them a preferred option in high-temperature semiconductor manufacturing processes, where maintaining precise thermal conditions is essential for product quality. Corseed Wafer Hands, while less commonly known, offer unique benefits that cater to specific needs within the semiconductor industry. Corseed is a proprietary ceramic material designed to provide a balance between the properties of alumina and silicon carbide. It offers good thermal stability, electrical insulation, and mechanical strength, making it a versatile choice for various wafer handling applications. Corseed Wafer Hands are particularly advantageous in situations where a combination of properties is required, such as moderate thermal resistance coupled with high mechanical durability. This versatility allows them to be used in a wide range of semiconductor manufacturing processes, providing a reliable solution for handling delicate wafers without compromising on performance. Each type of wafer hand plays a crucial role in the semiconductor manufacturing process, ensuring that wafers are handled with precision and care. The choice between alumina, silicon carbide, and corseed wafer hands depends on the specific requirements of the manufacturing process, including factors such as temperature, mechanical stress, and the need for electrical insulation. As the semiconductor industry continues to evolve and demand for more advanced electronic components increases, the importance of selecting the right wafer handling tools becomes even more critical. By understanding the unique properties and advantages of each type of wafer hand, manufacturers can optimize their processes and ensure the production of high-quality semiconductor devices.

Semiconductor Wafer Transfer Robots, FPD Transfers Robots in the Global Vacuum Ceramic Hands Market:

The Global Vacuum Ceramic Hands Market finds significant applications in the areas of Semiconductor Wafer Transfer Robots and FPD (Flat Panel Display) Transfer Robots, both of which are critical components in modern manufacturing environments. Semiconductor Wafer Transfer Robots are designed to automate the handling and movement of semiconductor wafers during the manufacturing process. These robots utilize vacuum ceramic hands to securely grip and transport wafers between different stages of production, ensuring precision and minimizing the risk of damage. The use of vacuum ceramic hands in these robots is essential due to their ability to provide a secure grip without exerting excessive force, which could potentially damage the delicate wafers. Additionally, the ceramic material's low particle generation helps maintain a clean manufacturing environment, reducing the risk of contamination and ensuring the production of high-quality semiconductor devices. FPD Transfer Robots, on the other hand, are used in the manufacturing of flat panel displays, such as those found in televisions, monitors, and smartphones. These robots also rely on vacuum ceramic hands to handle the delicate glass substrates used in display production. The precision and reliability offered by vacuum ceramic hands are crucial in this context, as even minor imperfections or contamination can significantly impact the quality and performance of the final product. The use of ceramic materials in these hands ensures that the substrates are handled with care, minimizing the risk of scratches or other damage that could compromise the display's functionality. In both semiconductor and FPD manufacturing, the use of vacuum ceramic hands in transfer robots offers several advantages. Firstly, the automation of wafer and substrate handling reduces the reliance on manual labor, increasing efficiency and throughput in the manufacturing process. This is particularly important in industries where demand is high, and production volumes need to be maximized. Secondly, the precision and reliability of vacuum ceramic hands help ensure consistent product quality, reducing the likelihood of defects and improving overall yield. This is essential in maintaining competitiveness in the global market, where consumers demand high-quality electronic devices. Furthermore, the use of vacuum ceramic hands in transfer robots contributes to the overall safety and cleanliness of the manufacturing environment. By minimizing the risk of contamination and damage, these tools help maintain the integrity of the production process, ensuring that the final products meet stringent quality standards. As the demand for semiconductors and flat panel displays continues to grow, driven by advancements in technology and increasing consumer electronics usage, the importance of efficient and reliable manufacturing solutions like vacuum ceramic hands becomes even more pronounced. By leveraging the unique properties of ceramic materials, manufacturers can optimize their processes and meet the demands of a rapidly evolving market.

Global Vacuum Ceramic Hands Market Outlook:

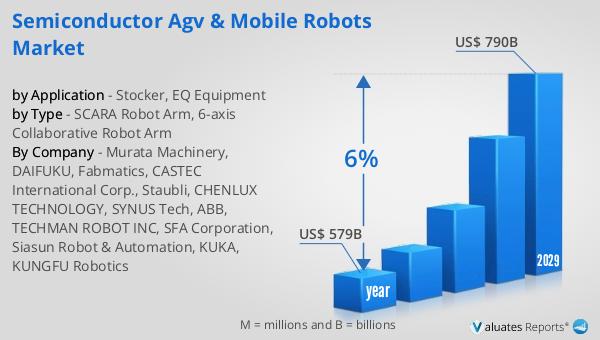

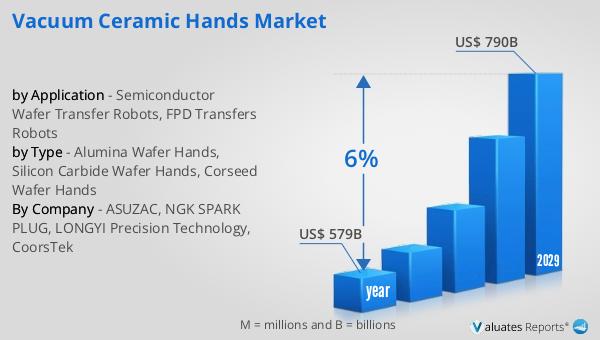

The global semiconductor market, valued at approximately $579 billion in 2022, is on a trajectory to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is indicative of the increasing demand for semiconductors, driven by advancements in technology and the proliferation of electronic devices across various sectors. As industries continue to innovate and integrate more sophisticated technologies into their products, the need for efficient and reliable semiconductor components becomes more critical. This upward trend in the semiconductor market underscores the importance of supporting industries, such as the Global Vacuum Ceramic Hands Market, which plays a vital role in the manufacturing process of these components. The projected growth in the semiconductor market highlights the expanding opportunities for manufacturers and suppliers within the industry. As the demand for semiconductors rises, so too does the need for advanced manufacturing solutions that can meet the stringent quality and efficiency requirements of modern production processes. Vacuum ceramic hands, with their unique properties and capabilities, are well-positioned to support this growth by providing reliable and precise wafer handling solutions that enhance the overall manufacturing process. By ensuring the safe and efficient handling of semiconductor wafers, vacuum ceramic hands contribute to the production of high-quality components that power a wide range of electronic devices. In conclusion, the anticipated growth in the global semiconductor market presents significant opportunities for the Global Vacuum Ceramic Hands Market. As the industry continues to evolve and demand for advanced electronic components increases, the importance of efficient and reliable manufacturing solutions becomes even more pronounced. By leveraging the unique properties of vacuum ceramic hands, manufacturers can optimize their processes and meet the demands of a rapidly changing market, ultimately contributing to the continued growth and success of the semiconductor industry.

| Report Metric | Details |

| Report Name | Vacuum Ceramic Hands Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | ASUZAC, NGK SPARK PLUG, LONGYI Precision Technology, CoorsTek |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |