What is Global Bare Alumina (Al2O3) Ceramic Substrate Market?

The Global Bare Alumina (Al2O3) Ceramic Substrate Market is a specialized segment within the broader ceramics industry, focusing on the production and application of alumina-based substrates. These substrates are primarily composed of aluminum oxide (Al2O3), a material known for its excellent thermal conductivity, electrical insulation properties, and mechanical strength. The market caters to various industries, including electronics, automotive, and telecommunications, where these substrates are used in the manufacturing of electronic components, circuit boards, and other high-performance applications. The demand for bare alumina ceramic substrates is driven by the increasing need for miniaturization and enhanced performance of electronic devices. As technology advances, the requirements for materials that can withstand high temperatures and provide reliable performance in demanding environments have become more critical. This market is characterized by continuous innovation and development, with manufacturers striving to improve the quality and performance of alumina substrates to meet the evolving needs of their customers. The global reach of this market indicates its significance in supporting technological advancements across various sectors, making it a vital component of the modern industrial landscape.

99.6% Alumina (Al2O3), 96% Alumina (Al2O3) in the Global Bare Alumina (Al2O3) Ceramic Substrate Market:

In the realm of the Global Bare Alumina (Al2O3) Ceramic Substrate Market, two significant variants of alumina are predominantly utilized: 99.6% Alumina and 96% Alumina. These percentages denote the purity levels of the alumina used in the substrates, which directly influence their properties and suitability for different applications. The 99.6% Alumina variant is known for its superior thermal and electrical insulation properties, making it ideal for high-performance applications where reliability and efficiency are paramount. This high-purity alumina is often used in the production of substrates for advanced electronic devices, where it provides excellent thermal management and electrical insulation, ensuring the longevity and performance of the components. On the other hand, the 96% Alumina variant, while slightly lower in purity, still offers substantial benefits in terms of mechanical strength and thermal stability. This variant is commonly used in applications where cost-effectiveness is a priority, without significantly compromising on performance. The choice between these two variants depends largely on the specific requirements of the application, with considerations such as operating temperature, electrical load, and environmental conditions playing a crucial role. Manufacturers in the Global Bare Alumina (Al2O3) Ceramic Substrate Market are continually exploring ways to enhance the properties of these materials, aiming to strike a balance between performance and cost. This ongoing research and development effort is essential in meeting the diverse needs of industries that rely on alumina substrates for their critical applications. As the demand for more efficient and reliable electronic components grows, the importance of these high-purity alumina substrates in the market is expected to increase, driving further innovation and development in this field.

DPC Ceramic Substrate, DBC Ceramic Substrate, Thin Film Ceramic Substrate, Thick Film Ceramic Substrate in the Global Bare Alumina (Al2O3) Ceramic Substrate Market:

The Global Bare Alumina (Al2O3) Ceramic Substrate Market finds extensive usage in various types of ceramic substrates, including DPC (Direct Plated Copper) Ceramic Substrate, DBC (Direct Bonded Copper) Ceramic Substrate, Thin Film Ceramic Substrate, and Thick Film Ceramic Substrate. Each of these substrates serves distinct purposes and is chosen based on the specific requirements of the application. DPC Ceramic Substrates are known for their excellent thermal conductivity and are often used in high-power applications where efficient heat dissipation is crucial. The direct plating of copper onto the alumina substrate enhances its thermal management capabilities, making it suitable for use in power electronics and LED lighting. DBC Ceramic Substrates, on the other hand, involve bonding a layer of copper directly onto the alumina substrate, providing a robust and reliable connection for high-power applications. This type of substrate is commonly used in power modules and automotive electronics, where durability and performance are critical. Thin Film Ceramic Substrates are characterized by their ability to support fine line circuitry, making them ideal for applications requiring high precision and miniaturization. These substrates are often used in the production of microelectronics and sensors, where space constraints and performance are key considerations. Thick Film Ceramic Substrates, in contrast, are used in applications where higher levels of electrical insulation and mechanical strength are required. These substrates are typically employed in the production of hybrid circuits and power resistors, where reliability and performance are essential. The versatility and adaptability of alumina ceramic substrates make them indispensable in a wide range of industries, supporting the development of advanced technologies and contributing to the overall growth of the Global Bare Alumina (Al2O3) Ceramic Substrate Market.

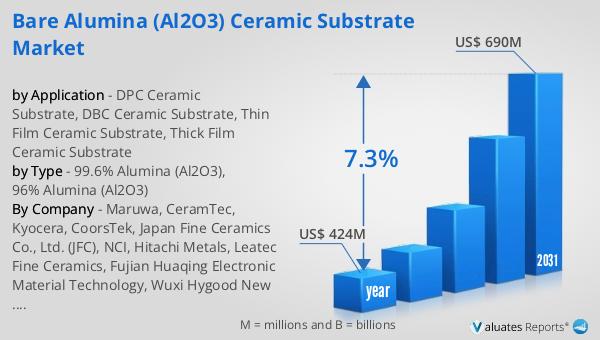

Global Bare Alumina (Al2O3) Ceramic Substrate Market Outlook:

The outlook for the Global Bare Alumina (Al2O3) Ceramic Substrate Market indicates a promising future, with significant growth anticipated over the coming years. In 2024, the market was valued at approximately US$ 424 million, reflecting its importance and demand across various industries. Looking ahead, projections suggest that the market will expand to reach a revised size of US$ 690 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 7.3% during the forecast period. Such a robust growth rate underscores the increasing reliance on alumina ceramic substrates in numerous applications, driven by the need for materials that offer superior thermal management, electrical insulation, and mechanical strength. The market's expansion is likely to be fueled by advancements in technology and the continuous push for miniaturization and enhanced performance in electronic devices. As industries such as electronics, automotive, and telecommunications continue to evolve, the demand for high-quality alumina substrates is expected to rise, further solidifying the market's position as a critical component of the global industrial landscape. This positive outlook highlights the potential for innovation and development within the market, as manufacturers strive to meet the growing needs of their customers and capitalize on emerging opportunities.

| Report Metric | Details |

| Report Name | Bare Alumina (Al2O3) Ceramic Substrate Market |

| Accounted market size in year | US$ 424 million |

| Forecasted market size in 2031 | US$ 690 million |

| CAGR | 7.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Maruwa, CeramTec, Kyocera, CoorsTek, Japan Fine Ceramics Co., Ltd. (JFC), NCI, Hitachi Metals, Leatec Fine Ceramics, Fujian Huaqing Electronic Material Technology, Wuxi Hygood New Technology, Zhejiang Xinna Ceramic New Material, Kallex Company, Sinoceram Technology (zhengzhou) Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |