What is Global Bidets Market?

The global bidets market is an intriguing segment of the sanitary ware industry, characterized by its diverse range of products designed to enhance personal hygiene. Bidets, which originated in Europe, have gained popularity worldwide due to their ability to provide a more thorough cleaning experience compared to traditional toilet paper. The market encompasses various types of bidets, including conventional bidets, bidet showers, and add-on bidets, each catering to different consumer preferences and installation requirements. The increasing awareness of personal hygiene, coupled with the growing emphasis on water conservation, has driven the demand for bidets globally. Additionally, the rising trend of smart homes and the integration of advanced technologies in bathroom fixtures have further propelled the market's growth. As consumers become more health-conscious and environmentally aware, the bidets market is expected to continue its upward trajectory, offering innovative solutions that cater to both residential and commercial sectors. The market's expansion is also supported by the increasing adoption of bidets in regions like Asia-Pacific and Europe, where cultural preferences and environmental concerns align with the benefits offered by bidet systems.

Conventional Bidets, Bidet Shower, Add-on Bidets in the Global Bidets Market:

Conventional bidets, bidet showers, and add-on bidets represent the core segments of the global bidets market, each offering unique features and benefits. Conventional bidets are standalone fixtures typically installed next to the toilet. They resemble a low sink or basin and are designed for users to straddle or sit on, allowing for a thorough cleaning of the genital and anal areas. These bidets are popular in Europe and parts of Asia, where they are considered a standard bathroom fixture. Conventional bidets offer a high level of hygiene and are often equipped with temperature controls and adjustable water pressure, providing a customizable experience for users. Bidet showers, also known as handheld bidets or shattafs, are more versatile and can be easily installed in existing bathrooms. They consist of a nozzle attached to a hose, allowing users to direct the water stream precisely where needed. Bidet showers are particularly popular in the Middle East and Southeast Asia, where they are valued for their convenience and ease of use. They are also a cost-effective option for those looking to upgrade their bathroom hygiene without significant renovations. Add-on bidets, on the other hand, are designed to be attached to existing toilet seats, offering a seamless integration into the bathroom. These bidets are often equipped with advanced features such as heated seats, air dryers, and deodorizers, providing a luxurious experience for users. Add-on bidets are gaining popularity in North America and Europe, where consumers are increasingly seeking modern and efficient bathroom solutions. The global bidets market is driven by the growing awareness of personal hygiene and the increasing demand for eco-friendly products. As consumers become more conscious of their environmental impact, bidets offer a sustainable alternative to toilet paper, reducing waste and conserving water. Additionally, the integration of smart technologies in bidet systems has further enhanced their appeal, offering features such as remote controls, customizable settings, and self-cleaning functions. The market is also influenced by cultural factors, with bidets being more prevalent in regions where water-based cleaning is preferred over paper-based methods. As the bidets market continues to evolve, manufacturers are focusing on innovation and product development to cater to the diverse needs of consumers worldwide. This includes the introduction of compact and space-saving designs, as well as the incorporation of advanced technologies to enhance user experience. The market's growth is also supported by the increasing adoption of bidets in commercial settings, such as hotels, restaurants, and public restrooms, where hygiene and comfort are paramount. Overall, the global bidets market is poised for significant growth, driven by the increasing demand for hygienic and sustainable bathroom solutions.

Household, Commercial in the Global Bidets Market:

The usage of bidets in the global market spans across both household and commercial sectors, each with distinct applications and benefits. In households, bidets are primarily used to enhance personal hygiene and provide a more comfortable and efficient cleaning experience. They are particularly popular among families with young children, elderly individuals, and those with mobility issues, as they offer a gentle and thorough cleaning method that reduces the need for excessive wiping. Bidets are also favored by environmentally conscious consumers who seek to reduce their reliance on toilet paper and minimize their environmental footprint. The integration of bidets in residential bathrooms is often seen as a mark of luxury and modernity, with many homeowners opting for advanced models that offer features such as heated seats, adjustable water pressure, and air dryers. In the commercial sector, bidets are increasingly being adopted in hotels, restaurants, and public restrooms to enhance the overall hygiene and comfort of guests and patrons. The hospitality industry, in particular, has recognized the value of bidets in providing a superior guest experience, with many luxury hotels incorporating bidet systems in their bathroom amenities. Bidets in commercial settings are often designed to be durable and easy to maintain, ensuring they can withstand frequent use while maintaining high standards of cleanliness. The use of bidets in public restrooms is also gaining traction, as businesses and municipalities seek to improve sanitation and reduce the spread of germs. The COVID-19 pandemic has further highlighted the importance of hygiene, leading to an increased demand for bidets in both household and commercial settings. As consumers and businesses prioritize cleanliness and health, the bidets market is expected to see continued growth and innovation. Manufacturers are responding to this demand by developing new products that cater to the specific needs of different user groups, such as compact bidets for small bathrooms and touchless models for public restrooms. The versatility and adaptability of bidets make them a valuable addition to any bathroom, offering a sustainable and hygienic solution that aligns with the evolving preferences of consumers and businesses alike.

Global Bidets Market Outlook:

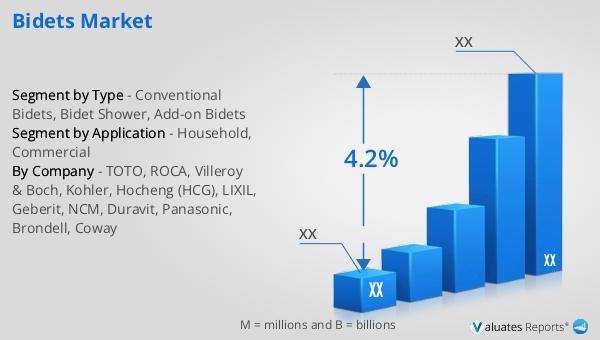

In 2024, the global bidets market was valued at approximately USD 4,317 million, with projections indicating a rise to around USD 5,735 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.2% from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold about 55% of the market share. The Asia-Pacific region emerges as the largest market, accounting for roughly 45% of the global share, followed by Europe with about 30%. Within the product categories, conventional bidets lead the market, capturing approximately 55% of the share. This data highlights the significant role of conventional bidets in the market, driven by their widespread acceptance and usage in various regions. The strong presence of the Asia-Pacific market can be attributed to cultural preferences and the increasing adoption of bidets in countries like Japan and South Korea, where hygiene and water conservation are prioritized. Europe's substantial market share reflects the region's long-standing tradition of using bidets as a standard bathroom fixture. The projected growth of the bidets market underscores the increasing demand for hygienic and sustainable bathroom solutions, as well as the ongoing innovation and product development by manufacturers to meet the diverse needs of consumers worldwide.

| Report Metric | Details |

| Report Name | Bidets Market |

| CAGR | 4.2% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | TOTO, ROCA, Villeroy & Boch, Kohler, Hocheng (HCG), LIXIL, Geberit, NCM, Duravit, Panasonic, Brondell, Coway |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |