What is Global Soft Ice Cream Machines Market?

The Global Soft Ice Cream Machines Market is a dynamic and evolving sector that caters to the increasing demand for soft serve ice cream across the world. These machines are essential for producing the creamy, smooth texture that defines soft ice cream, a popular treat enjoyed by people of all ages. The market encompasses a variety of machine types, including both multi-cylinder and single-cylinder models, each designed to meet different production needs and capacities. The growth of this market is driven by several factors, including the rising popularity of soft serve ice cream, the expansion of the food and beverage industry, and technological advancements in machine design and efficiency. Additionally, the market is influenced by regional preferences and the increasing trend of out-of-home dessert consumption. As consumer preferences continue to evolve, manufacturers are focusing on innovation and customization to cater to diverse tastes and dietary requirements, such as offering machines that can produce dairy-free or low-sugar options. The market's competitive landscape is characterized by the presence of several key players who are constantly striving to enhance their product offerings and expand their market reach. Overall, the Global Soft Ice Cream Machines Market is poised for steady growth, driven by both consumer demand and technological advancements.

Multi Cylinder, Single Cylinder in the Global Soft Ice Cream Machines Market:

In the Global Soft Ice Cream Machines Market, the distinction between multi-cylinder and single-cylinder machines is significant, as each type serves different operational needs and customer preferences. Multi-cylinder machines are designed to handle larger volumes of ice cream production, making them ideal for high-demand environments such as large restaurants, busy ice cream parlors, and commercial catering services. These machines typically feature multiple freezing cylinders, allowing them to produce different flavors simultaneously, which is a major advantage for businesses looking to offer a variety of options to their customers. The ability to produce large quantities of soft serve quickly and efficiently makes multi-cylinder machines a popular choice in the market, particularly in regions with high consumer demand for diverse ice cream flavors. On the other hand, single-cylinder machines are more compact and are often used in smaller establishments or for specific applications where space is limited, or the demand for ice cream is not as high. These machines are typically easier to operate and maintain, making them suitable for small cafes, kiosks, or mobile food vendors. Despite their smaller size, single-cylinder machines are capable of producing high-quality soft serve, and they are often favored by businesses that prioritize simplicity and cost-effectiveness. The choice between multi-cylinder and single-cylinder machines often depends on factors such as the scale of operation, budget constraints, and the specific needs of the business. Manufacturers in the Global Soft Ice Cream Machines Market are continually innovating to improve the efficiency, reliability, and versatility of both types of machines, ensuring that they meet the evolving demands of the food service industry. As a result, businesses have a wide range of options to choose from, allowing them to select the machine that best fits their operational requirements and customer preferences. The ongoing advancements in technology and design are expected to further enhance the capabilities of both multi-cylinder and single-cylinder machines, contributing to the overall growth and diversification of the market.

Catering Industry, Entertainment Venue, Shop, Others in the Global Soft Ice Cream Machines Market:

The Global Soft Ice Cream Machines Market finds extensive usage across various sectors, including the catering industry, entertainment venues, shops, and other areas, each with its unique requirements and customer base. In the catering industry, soft ice cream machines are a valuable asset, providing a quick and efficient way to serve large numbers of guests at events such as weddings, corporate functions, and parties. The ability to offer a variety of flavors and toppings enhances the appeal of soft serve ice cream, making it a popular choice for caterers looking to add a sweet touch to their menus. Entertainment venues, such as amusement parks, cinemas, and sports arenas, also benefit from the presence of soft ice cream machines, as they provide a convenient and enjoyable treat for visitors. The portability and ease of use of these machines make them ideal for high-traffic areas where quick service is essential. In retail settings, such as ice cream shops and cafes, soft ice cream machines are a staple, allowing businesses to offer a consistent and high-quality product that attracts repeat customers. The ability to customize flavors and create unique combinations is a significant advantage for shops looking to differentiate themselves in a competitive market. Additionally, other areas, such as educational institutions, hospitals, and corporate cafeterias, are increasingly incorporating soft ice cream machines into their offerings, recognizing the appeal of this versatile dessert. The adaptability of soft ice cream machines to various environments and their ability to cater to diverse consumer preferences make them a valuable addition to any food service operation. As the demand for soft serve ice cream continues to grow, the Global Soft Ice Cream Machines Market is expected to expand its presence across these sectors, driven by the need for efficient, reliable, and innovative solutions that meet the evolving tastes and expectations of consumers.

Global Soft Ice Cream Machines Market Outlook:

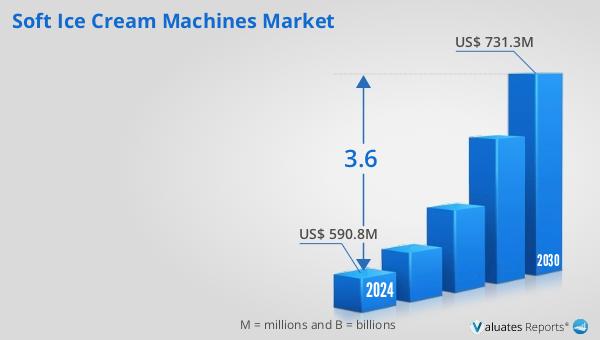

In 2024, the global market size for Soft Ice Cream Machines was valued at approximately US$ 610 million, with projections indicating a growth to around US$ 780 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.6% during the forecast period from 2025 to 2031. The market is dominated by the top three manufacturers, who collectively hold about 60% of the market share, highlighting the competitive nature of the industry. Among the various product types, multi-cylinder machines represent the largest segment, accounting for approximately 93% of the market share. This dominance is likely due to their ability to produce large volumes of ice cream efficiently, catering to high-demand environments. In terms of application, the catering industry emerges as the largest sector, with a share of about 40%. This is indicative of the significant role that soft ice cream machines play in catering services, where the ability to serve large numbers of guests quickly and efficiently is crucial. The market's growth trajectory is influenced by several factors, including technological advancements, changing consumer preferences, and the expansion of the food and beverage industry. As the demand for soft serve ice cream continues to rise, the Global Soft Ice Cream Machines Market is poised for steady growth, driven by both consumer demand and technological advancements.

| Report Metric | Details |

| Report Name | Soft Ice Cream Machines Market |

| Forecasted market size in 2031 | approximately US$ 780 million |

| CAGR | 3.6% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Middleby, Ali Group, Nissei, Stoelting, Gel Matic, DONPER, Spaceman, Guangzhuo Guangshen, Spelor Electrical Appliances, SaniServ, Oceanpower |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |