What is Global Safety Glasses Market?

The Global Safety Glasses Market is a crucial segment within the personal protective equipment (PPE) industry, focusing on providing eye protection across various sectors. Safety glasses are designed to shield the eyes from hazards such as flying debris, chemical splashes, and harmful radiation. These glasses are essential in environments where eye injuries are a significant risk, including industrial, construction, and laboratory settings. The market for safety glasses is driven by stringent safety regulations and an increasing awareness of workplace safety. Technological advancements have led to the development of more comfortable and effective safety glasses, incorporating features like anti-fog coatings, UV protection, and impact resistance. The market is diverse, with products ranging from basic protective eyewear to advanced models with prescription lenses and specialized coatings. As industries continue to prioritize employee safety, the demand for high-quality safety glasses is expected to grow, making this market a vital component of occupational health and safety strategies worldwide. The global reach of this market ensures that safety glasses are available to meet the needs of various industries, contributing to the reduction of workplace injuries and enhancing overall productivity.

Polycarbonate Lens, Plastic (CR39) Lens, Trivex Lens, Others in the Global Safety Glasses Market:

Polycarbonate lenses are a popular choice in the Global Safety Glasses Market due to their exceptional impact resistance and lightweight nature. These lenses are made from a type of plastic that is highly durable, making them ideal for environments where there is a risk of flying debris or other physical hazards. Polycarbonate lenses also offer excellent UV protection, which is crucial for outdoor work environments. Their lightweight nature ensures comfort during prolonged use, which is a significant advantage in industries where workers are required to wear safety glasses for extended periods. Plastic (CR39) lenses, on the other hand, are known for their optical clarity and scratch resistance. CR39 is a type of plastic that provides clear vision and is less prone to scratching compared to other materials. This makes CR39 lenses suitable for environments where visual clarity is paramount, such as in laboratories or precision manufacturing. However, they are not as impact-resistant as polycarbonate lenses, which limits their use in high-risk environments. Trivex lenses are a relatively new addition to the safety glasses market, offering a balance between the optical clarity of CR39 and the impact resistance of polycarbonate. Trivex is a lightweight material that provides excellent visual clarity and is highly resistant to impact and chemicals. This makes Trivex lenses suitable for a wide range of applications, including chemical processing and construction. The versatility of Trivex lenses makes them an attractive option for industries that require both clarity and protection. Other materials used in safety glasses include glass and acrylic, each with its own set of advantages and limitations. Glass lenses offer superior optical clarity and scratch resistance but are heavier and more prone to shattering upon impact. Acrylic lenses are lightweight and provide good optical clarity but are less durable than polycarbonate or Trivex lenses. The choice of lens material in safety glasses depends on the specific requirements of the industry and the nature of the hazards present. As the Global Safety Glasses Market continues to evolve, manufacturers are focusing on developing lenses that offer a combination of comfort, clarity, and protection to meet the diverse needs of various industries.

Manufacturing Industry, Construction Industry, Oil & Gas Industry, Chemicals Industry, Mining Industry, Pharmaceutical Industry, Others in the Global Safety Glasses Market:

The Global Safety Glasses Market plays a vital role in ensuring safety across several industries, each with unique requirements for eye protection. In the manufacturing industry, safety glasses are essential to protect workers from flying debris, sparks, and chemical splashes. The use of machinery and tools in manufacturing environments poses significant risks to eye safety, making protective eyewear a critical component of workplace safety protocols. In the construction industry, safety glasses are used to shield workers from dust, debris, and UV radiation. Construction sites are dynamic environments with multiple hazards, and safety glasses help prevent eye injuries that can result from exposure to these elements. The oil and gas industry also relies heavily on safety glasses to protect workers from chemical splashes, flying particles, and intense light. The nature of work in this industry involves handling hazardous materials and operating in challenging environments, making eye protection a priority. In the chemicals industry, safety glasses are used to protect against chemical splashes and fumes. Workers in this industry are often exposed to corrosive substances, and safety glasses provide a barrier that helps prevent eye injuries. The mining industry presents unique challenges, with workers exposed to dust, debris, and low-light conditions. Safety glasses in mining are designed to offer protection against these hazards while ensuring visibility in dimly lit environments. The pharmaceutical industry also requires safety glasses to protect workers from chemical exposure and biological hazards. In this industry, precision and cleanliness are paramount, and safety glasses help maintain a safe working environment. Other industries, such as agriculture and food processing, also benefit from the use of safety glasses to protect against various hazards. The versatility of safety glasses makes them an indispensable tool in promoting workplace safety across diverse sectors. As industries continue to prioritize employee safety, the demand for high-quality safety glasses is expected to grow, further driving the expansion of the Global Safety Glasses Market.

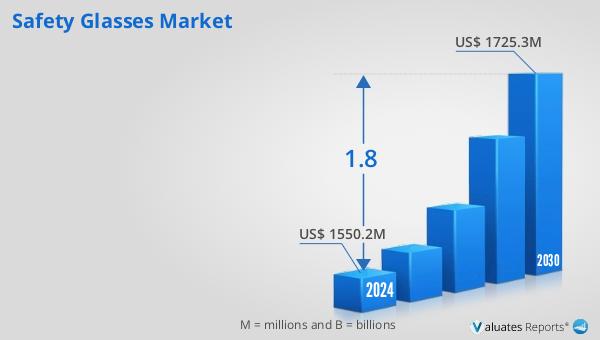

Global Safety Glasses Market Outlook:

In 2024, the global market for safety glasses was valued at approximately US$ 1,575 million, with projections indicating an increase to around US$ 1,782 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 1.8% during the forecast period from 2025 to 2031. The market is characterized by a competitive landscape, with the top five companies collectively holding about 30% of the market share. North America emerges as the largest regional market, accounting for approximately 36% of the global share. This is followed by Europe, which holds a share of about 34%, and the Asia Pacific region, contributing around 20% to the market. The steady growth of the safety glasses market can be attributed to increasing awareness of workplace safety and stringent regulatory requirements across various industries. As companies continue to invest in employee safety and compliance with safety standards, the demand for high-quality safety glasses is expected to rise. The market's expansion is further supported by technological advancements in lens materials and design, which enhance the comfort and effectiveness of safety glasses. As a result, the Global Safety Glasses Market is poised for continued growth, driven by the need for reliable eye protection solutions across diverse industrial sectors.

| Report Metric | Details |

| Report Name | Safety Glasses Market |

| Forecasted market size in 2031 | approximately US$ 1782 million |

| CAGR | 1.8% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | 3M, Honeywell, MCR Safety, Kimberly-Clark, MSA, Radians, Yamamoto Kogaku, Bolle Safety, Gateway Safety, Dräger, Midori Anzen, DEWALT, Delta Plus, Uvex Safety Group, Protective Industrial Products, Carhartt, Pyramex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |