What is Global Cooled Thermal Imaging Imagers Market?

The Global Cooled Thermal Imaging Imagers Market is a specialized segment within the broader thermal imaging industry, focusing on devices that utilize cooled infrared detectors to capture thermal images. These imagers are designed to detect infrared radiation, which is emitted by all objects based on their temperature, and convert it into a visible image. The cooling mechanism, often involving cryogenic coolers, enhances the sensitivity and resolution of these devices, allowing them to detect minute temperature differences and produce high-quality images even in challenging conditions. This makes them particularly valuable in applications requiring precise thermal measurements and detailed imaging, such as in military operations, scientific research, and industrial inspections. The market for these advanced imaging systems is driven by the increasing demand for high-performance thermal imaging solutions across various sectors, including defense, automotive, and aerospace. As technology advances, these imagers are becoming more compact, efficient, and accessible, further expanding their potential applications and market reach. The growth of this market is also supported by the rising awareness of the benefits of thermal imaging technology in enhancing safety, security, and operational efficiency across different industries.

Handheld, Mounted in the Global Cooled Thermal Imaging Imagers Market:

In the Global Cooled Thermal Imaging Imagers Market, devices can be categorized based on their form factor, primarily into handheld and mounted systems. Handheld thermal imagers are portable devices that offer flexibility and ease of use, making them ideal for field operations and situations where mobility is crucial. These devices are commonly used by military personnel, firefighters, and maintenance technicians who need to quickly assess situations and make informed decisions on the spot. Handheld imagers are designed to be lightweight and ergonomic, ensuring that users can operate them comfortably over extended periods. They often come equipped with features such as high-resolution displays, intuitive controls, and connectivity options for data sharing and analysis. On the other hand, mounted thermal imaging systems are typically installed on vehicles, aircraft, or fixed structures, providing continuous monitoring and surveillance capabilities. These systems are essential in applications where constant observation is required, such as border security, perimeter surveillance, and infrastructure monitoring. Mounted imagers are designed to withstand harsh environmental conditions and can be integrated with other systems for enhanced functionality, such as automated tracking and alarm systems. The choice between handheld and mounted systems depends on the specific requirements of the application, with each offering distinct advantages in terms of mobility, coverage, and operational efficiency. As the demand for thermal imaging technology continues to grow, manufacturers are focusing on developing innovative solutions that cater to the diverse needs of users across different sectors. This includes advancements in sensor technology, image processing algorithms, and user interface design, all aimed at enhancing the performance and usability of both handheld and mounted thermal imagers. Additionally, the integration of artificial intelligence and machine learning capabilities is opening new possibilities for automated analysis and decision-making, further expanding the potential applications of these devices. As a result, the Global Cooled Thermal Imaging Imagers Market is poised for significant growth, driven by the increasing adoption of these advanced imaging solutions in various industries.

Military, Automotive, Aerospace, Others in the Global Cooled Thermal Imaging Imagers Market:

The usage of Global Cooled Thermal Imaging Imagers Market spans several critical areas, including military, automotive, aerospace, and others, each benefiting from the unique capabilities of these advanced imaging systems. In the military sector, cooled thermal imaging imagers are indispensable tools for surveillance, target acquisition, and reconnaissance missions. Their ability to detect heat signatures in complete darkness or through smoke and fog provides a tactical advantage, enabling military personnel to operate effectively in challenging environments. These imagers are often integrated into weapon systems, vehicles, and drones, enhancing situational awareness and operational effectiveness. In the automotive industry, thermal imaging technology is increasingly being used to improve safety and driver assistance systems. Cooled thermal imagers can detect pedestrians, animals, and other obstacles on the road, even in low-light conditions, reducing the risk of accidents. They are also used in the development and testing of automotive components, helping engineers identify thermal anomalies and optimize performance. In the aerospace sector, cooled thermal imaging imagers play a crucial role in aircraft maintenance and inspection. They enable technicians to detect potential issues such as overheating components or insulation failures, ensuring the safety and reliability of aircraft operations. Additionally, these imagers are used in satellite and space exploration missions, where they provide valuable data for scientific research and environmental monitoring. Beyond these primary sectors, cooled thermal imaging imagers are also used in various other applications, including industrial inspections, firefighting, and medical diagnostics. In industrial settings, they help identify equipment malfunctions and prevent costly downtime by detecting heat-related issues before they escalate. Firefighters use thermal imagers to locate hotspots and navigate through smoke-filled environments, improving their ability to save lives and protect property. In the medical field, thermal imaging is used as a non-invasive diagnostic tool, providing insights into conditions such as inflammation and circulatory disorders. The versatility and effectiveness of cooled thermal imaging imagers make them an invaluable asset across a wide range of industries, driving their adoption and market growth.

Global Cooled Thermal Imaging Imagers Market Outlook:

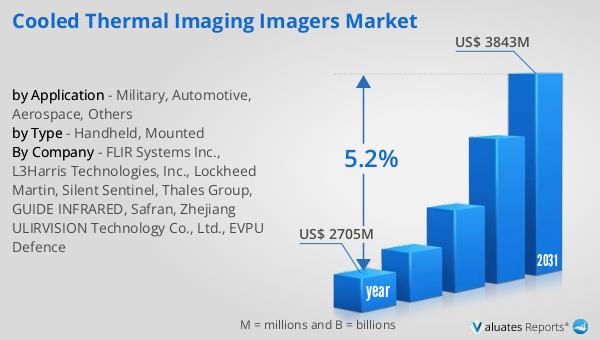

The outlook for the Global Cooled Thermal Imaging Imagers Market indicates a promising trajectory, with the market valued at approximately US$ 2705 million in 2024. It is anticipated to expand to a revised size of US$ 3843 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.2% over the forecast period. This growth is driven by the increasing demand for high-performance thermal imaging solutions across various sectors, including defense, automotive, and aerospace. The enhanced capabilities of cooled thermal imagers, such as their ability to detect minute temperature differences and produce high-resolution images, make them particularly valuable in applications requiring precise thermal measurements and detailed imaging. As technology continues to advance, these imagers are becoming more compact, efficient, and accessible, further expanding their potential applications and market reach. The rising awareness of the benefits of thermal imaging technology in enhancing safety, security, and operational efficiency across different industries is also contributing to the market's growth. Manufacturers are focusing on developing innovative solutions that cater to the diverse needs of users, including advancements in sensor technology, image processing algorithms, and user interface design. The integration of artificial intelligence and machine learning capabilities is opening new possibilities for automated analysis and decision-making, further expanding the potential applications of these devices. As a result, the Global Cooled Thermal Imaging Imagers Market is poised for significant growth, driven by the increasing adoption of these advanced imaging solutions in various industries.

| Report Metric | Details |

| Report Name | Cooled Thermal Imaging Imagers Market |

| Accounted market size in year | US$ 2705 million |

| Forecasted market size in 2031 | US$ 3843 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | FLIR Systems Inc., L3Harris Technologies, Inc., Lockheed Martin, Silent Sentinel, Thales Group, GUIDE INFRARED, Safran, Zhejiang ULIRVISION Technology Co., Ltd., EVPU Defence |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |