What is Global Coated Carbon Foil Market?

The Global Coated Carbon Foil Market is a specialized segment within the broader materials industry, focusing on the production and application of carbon-coated foils. These foils are primarily used in energy storage devices, such as batteries and supercapacitors, due to their excellent electrical conductivity and stability. The market is driven by the increasing demand for efficient energy storage solutions, which are crucial for various applications, including electric vehicles, renewable energy systems, and portable electronic devices. Coated carbon foils are typically made by applying a thin layer of carbon onto metal substrates like copper or aluminum, enhancing their performance characteristics. This market is characterized by continuous innovation and development, as manufacturers strive to improve the efficiency and cost-effectiveness of these materials. The growth of the Global Coated Carbon Foil Market is also supported by the rising awareness of environmental sustainability, as these materials contribute to the development of cleaner energy technologies. As the demand for advanced energy storage solutions continues to rise, the market for coated carbon foils is expected to expand, offering numerous opportunities for manufacturers and investors alike.

Carbon Coated Copper Foil, Carbon Coated Aluminum Foil in the Global Coated Carbon Foil Market:

Carbon Coated Copper Foil and Carbon Coated Aluminum Foil are two significant products within the Global Coated Carbon Foil Market, each serving distinct roles in enhancing the performance of energy storage devices. Carbon Coated Copper Foil is primarily used in lithium-ion batteries, where it serves as a current collector for the anode. The carbon coating on the copper foil improves its electrical conductivity and provides a stable interface for lithium-ion intercalation, which is crucial for the efficient operation of the battery. This enhancement leads to better battery performance, including higher energy density, longer cycle life, and improved safety. The use of carbon-coated copper foil is particularly important in high-performance applications, such as electric vehicles and portable electronics, where battery efficiency and reliability are paramount. On the other hand, Carbon Coated Aluminum Foil is commonly used as a current collector for the cathode in lithium-ion batteries. Similar to its copper counterpart, the carbon coating on aluminum foil enhances its conductivity and stability, which is essential for the efficient transfer of electrons during the battery's charge and discharge cycles. This results in improved battery performance, including faster charging times and increased energy output. Carbon-coated aluminum foil is also used in supercapacitors, where it contributes to the high power density and rapid charge-discharge capabilities of these devices. The choice between copper and aluminum foils depends on the specific requirements of the application, with factors such as cost, weight, and performance playing a crucial role in the decision-making process. Both types of coated foils are integral to the development of advanced energy storage solutions, as they enable the creation of more efficient and reliable devices. The continuous advancement in coating technologies and materials science is expected to further enhance the performance of these foils, driving their adoption in various applications. As the demand for energy storage solutions continues to grow, the market for carbon-coated copper and aluminum foils is poised for significant expansion, offering numerous opportunities for innovation and growth.

Super Capacitor, Power Battery, Energy Storage Battery, Others in the Global Coated Carbon Foil Market:

The Global Coated Carbon Foil Market finds its applications in several key areas, including supercapacitors, power batteries, energy storage batteries, and other specialized uses. In the realm of supercapacitors, coated carbon foils play a crucial role in enhancing the performance of these high-power devices. Supercapacitors are known for their ability to deliver rapid bursts of energy, making them ideal for applications requiring quick charge and discharge cycles. The carbon coating on the foils improves their electrical conductivity and stability, which is essential for maintaining the high power density and efficiency of supercapacitors. This makes them suitable for use in applications such as regenerative braking systems in vehicles, where quick energy recovery and delivery are critical. In power batteries, which are commonly used in electric vehicles and other high-demand applications, coated carbon foils serve as current collectors that enhance the overall efficiency and reliability of the battery. The carbon coating provides a stable interface for ion transfer, reducing resistance and improving the battery's energy density and cycle life. This is particularly important in electric vehicles, where battery performance directly impacts the vehicle's range and efficiency. Energy storage batteries, used in renewable energy systems and grid storage applications, also benefit from the use of coated carbon foils. These batteries require materials that can withstand long cycles and maintain performance over time. The carbon coating on the foils ensures that they can handle the demands of frequent charge and discharge cycles, making them ideal for storing energy generated from renewable sources like solar and wind. Additionally, coated carbon foils are used in other specialized applications, such as in the development of flexible and wearable electronics, where their lightweight and conductive properties are highly valued. The versatility and performance enhancements provided by coated carbon foils make them indispensable in the development of advanced energy storage solutions, driving their adoption across various industries. As the demand for efficient and reliable energy storage continues to grow, the Global Coated Carbon Foil Market is expected to expand, offering new opportunities for innovation and application.

Global Coated Carbon Foil Market Outlook:

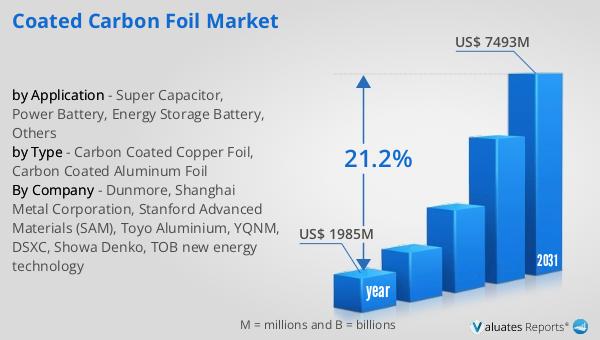

In 2024, the global market for Coated Carbon Foil was valued at approximately $1,985 million. Looking ahead, this market is anticipated to experience significant growth, reaching an estimated size of $7,493 million by 2031. This expansion represents a compound annual growth rate (CAGR) of 21.2% over the forecast period. This impressive growth trajectory underscores the increasing demand for coated carbon foils, driven by their critical role in enhancing the performance of energy storage devices. As industries continue to seek more efficient and sustainable energy solutions, the adoption of coated carbon foils is expected to rise, contributing to the market's robust growth. The market's expansion is also supported by ongoing advancements in coating technologies and materials science, which are continually improving the performance and cost-effectiveness of these materials. As a result, manufacturers and investors are presented with numerous opportunities to capitalize on this growing market, driving further innovation and development in the field. The projected growth of the Global Coated Carbon Foil Market highlights the importance of these materials in the future of energy storage and underscores their potential to contribute to a more sustainable and efficient energy landscape.

| Report Metric | Details |

| Report Name | Coated Carbon Foil Market |

| Accounted market size in year | US$ 1985 million |

| Forecasted market size in 2031 | US$ 7493 million |

| CAGR | 21.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dunmore, Shanghai Metal Corporation, Stanford Advanced Materials (SAM), Toyo Aluminium, YQNM, DSXC, Showa Denko, TOB new energy technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |