What is Global LCD Segment Drivers Market?

The Global LCD Segment Drivers Market is a crucial component of the broader display technology industry, focusing on the electronic circuits that control the operation of liquid crystal displays (LCDs). These drivers are essential for managing the pixels on an LCD screen, ensuring that images are displayed correctly and efficiently. The market for LCD segment drivers is driven by the increasing demand for high-quality displays in various applications, including consumer electronics, automotive displays, and industrial equipment. As technology advances, there is a growing need for more sophisticated and efficient LCD drivers that can support higher resolutions and faster refresh rates. Additionally, the rise of smart devices and the Internet of Things (IoT) has further fueled the demand for advanced display technologies, thereby boosting the LCD segment drivers market. The market is characterized by rapid technological advancements and intense competition among key players, who are constantly innovating to meet the evolving needs of consumers and industries. As a result, the Global LCD Segment Drivers Market is poised for significant growth, driven by the continuous development of new applications and the increasing adoption of LCD technology across various sectors.

Max Segment Below 100, Max Segment 100-500, Max Segment Above 500 in the Global LCD Segment Drivers Market:

In the Global LCD Segment Drivers Market, the Max Segment Below 100, Max Segment 100-500, and Max Segment Above 500 represent different categories based on the capacity and performance of the drivers. The Max Segment Below 100 typically includes drivers that are designed for smaller, less complex displays. These drivers are often used in applications where cost-effectiveness and basic functionality are prioritized over high performance. They are commonly found in simple consumer electronics, such as digital watches, calculators, and basic mobile phones. Despite their limited capabilities, these drivers play a crucial role in ensuring the proper functioning of these devices by managing the display of basic information. On the other hand, the Max Segment 100-500 encompasses a broader range of drivers that cater to mid-range applications. This segment is the largest in the market, accounting for over 58% of the total share. These drivers are designed to support more complex displays with higher resolutions and faster refresh rates, making them suitable for a wide variety of applications, including mid-range smartphones, tablets, and automotive displays. The versatility and performance of these drivers make them highly sought after in the market, as they strike a balance between cost and functionality. Finally, the Max Segment Above 500 includes the most advanced drivers, which are designed for high-performance applications. These drivers are capable of supporting the most demanding display technologies, such as high-definition televisions, advanced gaming monitors, and professional-grade industrial equipment. They offer superior performance in terms of resolution, color accuracy, and refresh rates, making them ideal for applications where display quality is of utmost importance. The demand for these high-end drivers is driven by the increasing consumer preference for premium display experiences and the growing adoption of advanced technologies in various industries. Overall, the Global LCD Segment Drivers Market is characterized by a diverse range of products that cater to different needs and applications, with each segment playing a vital role in the overall growth and development of the market.

Automotive Industry, Industrial Industry, Consumer Electronics, Others in the Global LCD Segment Drivers Market:

The Global LCD Segment Drivers Market finds extensive usage across various industries, including the automotive, industrial, consumer electronics, and others. In the automotive industry, LCD segment drivers are crucial for the development of advanced display systems used in modern vehicles. These drivers enable the integration of high-resolution displays in dashboards, infotainment systems, and rear-seat entertainment units, enhancing the overall driving experience. As vehicles become more connected and autonomous, the demand for sophisticated display technologies continues to rise, driving the growth of the LCD segment drivers market in this sector. In the industrial industry, LCD segment drivers are used in a wide range of applications, from control panels and instrumentation displays to digital signage and interactive kiosks. These drivers are essential for ensuring the accurate and efficient operation of industrial equipment, providing operators with critical information and enhancing productivity. The increasing adoption of automation and smart technologies in industrial settings has further fueled the demand for advanced LCD segment drivers, as they enable the development of more intuitive and user-friendly interfaces. In the consumer electronics sector, LCD segment drivers are integral to the functioning of a wide array of devices, including smartphones, tablets, laptops, and televisions. As consumers continue to demand higher-quality displays with better resolution, color accuracy, and refresh rates, the need for advanced LCD segment drivers has grown significantly. These drivers play a crucial role in delivering the immersive visual experiences that consumers expect from their devices, driving innovation and competition in the market. Beyond these primary industries, LCD segment drivers are also used in various other applications, such as medical devices, wearable technology, and smart home systems. In the medical field, for example, these drivers are used in diagnostic equipment and patient monitoring systems, where accurate and reliable display of information is critical. Similarly, in the realm of wearable technology and smart home devices, LCD segment drivers enable the development of compact, energy-efficient displays that enhance the functionality and user experience of these products. Overall, the Global LCD Segment Drivers Market is characterized by its wide-ranging applications across multiple industries, each of which contributes to the market's growth and development.

Global LCD Segment Drivers Market Outlook:

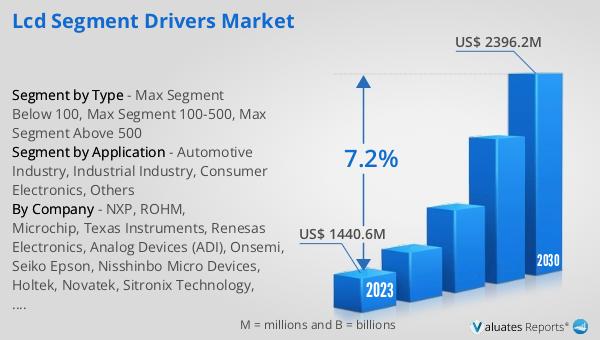

The worldwide market for LCD Segment Drivers was valued at approximately $1,685 million in 2024, with projections indicating it could expand to around $2,715 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 7.1% throughout the forecast period. The market is dominated by the top five manufacturers, who collectively hold over 47% of the market share. Japan stands out as the leading producer of LCD segment drivers, contributing more than 29% to the global production. Within the product categories, the Max Segment 100-500 emerges as the most significant, capturing over 58% of the market share. This segment's prominence is attributed to its versatility and ability to cater to a wide range of applications, from mid-range consumer electronics to automotive displays. The robust growth of the LCD segment drivers market is driven by the increasing demand for high-quality displays across various industries, as well as the continuous advancements in display technology. As the market evolves, key players are focusing on innovation and strategic partnerships to maintain their competitive edge and capitalize on emerging opportunities.

| Report Metric | Details |

| Report Name | LCD Segment Drivers Market |

| Accounted market size in year | US$ 1685 million |

| Forecasted market size in 2031 | US$ 2715 million |

| CAGR | 7.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | NXP, ROHM, Microchip, Texas Instruments, Renesas Electronics, Analog Devices (ADI), Onsemi, Seiko Epson, Nisshinbo Micro Devices, Holtek, Novatek, Sitronix Technology, UltraChip |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |