What is Global Semiconductor Package Solder Balls Market?

The Global Semiconductor Package Solder Balls Market is a crucial segment within the electronics manufacturing industry, focusing on the production and distribution of solder balls used in semiconductor packaging. Solder balls are tiny spheres of solder that serve as electrical connections between the semiconductor chip and the package or between the package and the printed circuit board (PCB). These components are essential for ensuring reliable electrical connections and mechanical stability in electronic devices. The market for semiconductor package solder balls is driven by the increasing demand for miniaturized and high-performance electronic devices, such as smartphones, tablets, and laptops. As technology advances, the need for more efficient and compact packaging solutions grows, leading to a higher demand for solder balls. Additionally, the shift towards lead-free solder balls due to environmental regulations and the push for sustainable manufacturing practices further influences the market dynamics. The global market is characterized by a mix of established players and new entrants, all striving to innovate and meet the evolving needs of the electronics industry. As a result, the Global Semiconductor Package Solder Balls Market is poised for significant growth, driven by technological advancements and the increasing adoption of electronic devices worldwide.

Lead-Free Solder Balls, Lead Solder Balls in the Global Semiconductor Package Solder Balls Market:

Lead-Free Solder Balls and Lead Solder Balls are two primary types of solder balls used in the Global Semiconductor Package Solder Balls Market, each with distinct characteristics and applications. Lead-Free Solder Balls are increasingly becoming the standard in the industry due to environmental concerns and regulatory requirements. These solder balls are made from a combination of metals such as tin, silver, and copper, which provide a reliable and environmentally friendly alternative to traditional lead-based solder balls. The shift towards lead-free options is largely driven by the Restriction of Hazardous Substances (RoHS) directive, which limits the use of certain hazardous materials in electronic products. Lead-Free Solder Balls offer several advantages, including improved thermal and mechanical properties, making them suitable for high-temperature applications and ensuring long-term reliability in electronic devices. On the other hand, Lead Solder Balls, traditionally composed of a tin-lead alloy, have been widely used in the electronics industry for decades due to their excellent solderability and cost-effectiveness. Despite their declining popularity due to environmental concerns, lead solder balls are still used in specific applications where their unique properties are required. For instance, they are preferred in certain military and aerospace applications where reliability and performance are critical, and the use of lead-free alternatives may not meet the stringent requirements. The choice between lead-free and lead solder balls depends on various factors, including the specific application, regulatory requirements, and cost considerations. Manufacturers must carefully evaluate these factors to select the appropriate type of solder ball for their needs. As the industry continues to evolve, the demand for lead-free solder balls is expected to increase, driven by the growing emphasis on sustainability and the need for environmentally friendly manufacturing practices. However, lead solder balls will likely remain in use for niche applications where their unique properties are indispensable. The ongoing research and development efforts in the field aim to enhance the performance and reliability of both lead-free and lead solder balls, ensuring they meet the ever-changing demands of the electronics industry. As a result, the Global Semiconductor Package Solder Balls Market is characterized by continuous innovation and adaptation to meet the diverse needs of electronic device manufacturers worldwide.

BGA, CSP, Other in the Global Semiconductor Package Solder Balls Market:

The usage of the Global Semiconductor Package Solder Balls Market is prominently seen in various packaging technologies, including Ball Grid Array (BGA), Chip Scale Package (CSP), and other advanced packaging solutions. In BGA, solder balls play a critical role in providing electrical connections between the semiconductor chip and the printed circuit board. BGA is widely used in applications where high performance and reliability are essential, such as in computer processors, graphics cards, and networking equipment. The use of solder balls in BGA packaging ensures efficient heat dissipation and robust mechanical support, which are crucial for the optimal functioning of high-performance electronic devices. Chip Scale Package (CSP) is another area where solder balls are extensively used. CSP is a type of surface mount packaging that allows for a smaller footprint and higher density of components on the PCB. This packaging technology is particularly popular in consumer electronics, such as smartphones and tablets, where space is at a premium. Solder balls in CSP provide the necessary electrical connections while maintaining the compact size and lightweight nature of the package. The demand for CSP is driven by the increasing trend towards miniaturization and the need for more powerful yet compact electronic devices. Apart from BGA and CSP, solder balls are also used in other advanced packaging solutions, such as wafer-level packaging and flip-chip technology. These packaging methods are employed in applications that require high-speed performance and enhanced thermal management, such as in telecommunications and automotive electronics. The use of solder balls in these advanced packaging solutions ensures reliable electrical connections and efficient heat dissipation, which are critical for the performance and longevity of electronic devices. As the electronics industry continues to evolve, the demand for innovative packaging solutions that can accommodate the increasing complexity and functionality of electronic devices is expected to grow. The Global Semiconductor Package Solder Balls Market plays a vital role in meeting this demand by providing high-quality solder balls that enable the development of advanced packaging technologies. The ongoing advancements in packaging technologies and the increasing adoption of electronic devices worldwide are expected to drive the growth of the Global Semiconductor Package Solder Balls Market in the coming years.

Global Semiconductor Package Solder Balls Market Outlook:

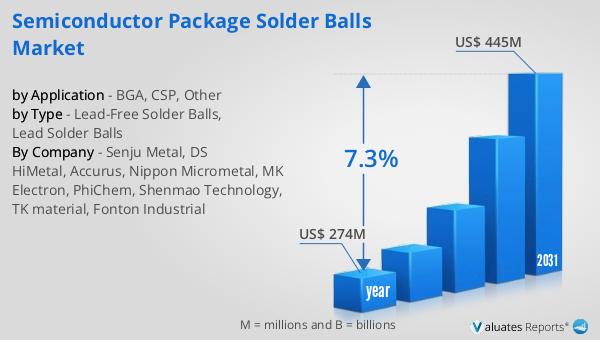

In 2024, the global market for Semiconductor Package Solder Balls was valued at approximately $274 million. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach an estimated size of $445 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 7.3% throughout the forecast period. The expansion of this market can be attributed to several factors, including the rising demand for electronic devices, advancements in semiconductor packaging technologies, and the increasing shift towards environmentally friendly manufacturing practices. As electronic devices become more sophisticated and compact, the need for reliable and efficient solder balls in semiconductor packaging becomes increasingly critical. The market's growth is also supported by the ongoing research and development efforts aimed at enhancing the performance and reliability of solder balls, ensuring they meet the evolving needs of the electronics industry. As a result, the Global Semiconductor Package Solder Balls Market is poised for substantial growth, driven by technological advancements and the increasing adoption of electronic devices worldwide.

| Report Metric | Details |

| Report Name | Semiconductor Package Solder Balls Market |

| Accounted market size in year | US$ 274 million |

| Forecasted market size in 2031 | US$ 445 million |

| CAGR | 7.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Senju Metal, DS HiMetal, Accurus, Nippon Micrometal, MK Electron, PhiChem, Shenmao Technology, TK material, Fonton Industrial |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |