What is Global Coextruded Multilayer Films Market?

The Global Coextruded Multilayer Films Market is a dynamic and evolving sector within the packaging industry, characterized by its innovative approach to creating films with multiple layers. These films are produced through a process called coextrusion, where different layers of materials are combined to form a single film with enhanced properties. This technique allows manufacturers to tailor the film's characteristics, such as strength, barrier properties, and flexibility, to meet specific requirements. The market for these films is driven by the growing demand for efficient and sustainable packaging solutions across various industries, including food and pharmaceuticals. Coextruded multilayer films offer significant advantages over traditional single-layer films, such as improved protection against moisture, oxygen, and other environmental factors, which helps in extending the shelf life of products. Additionally, these films are lightweight and can be designed to be recyclable, aligning with the increasing consumer preference for eco-friendly packaging options. As industries continue to seek innovative ways to enhance product safety and reduce environmental impact, the Global Coextruded Multilayer Films Market is poised for significant growth, offering versatile solutions that cater to diverse packaging needs.

Three-Layer Film, Five-Layer Film, Seven-Layer Film, Nine-Layer Film, Eleven-Layer Film, Other in the Global Coextruded Multilayer Films Market:

In the realm of coextruded multilayer films, the number of layers plays a crucial role in determining the film's properties and applications. Three-layer films are among the most common and are typically used for applications that require basic barrier properties and mechanical strength. These films are often employed in packaging solutions where cost-effectiveness is a priority, and the need for advanced barrier properties is minimal. The three-layer structure usually consists of a core layer sandwiched between two outer layers, each serving a specific function, such as providing strength or acting as a barrier to moisture. Five-layer films take the concept a step further by incorporating additional layers that enhance the film's barrier properties and mechanical strength. These films are often used in applications where moderate barrier properties are required, such as in the packaging of dry foods or products that need protection from moisture and oxygen. The additional layers allow for the inclusion of materials that can improve the film's resistance to punctures and tears, making them suitable for more demanding packaging applications. Seven-layer films are designed for applications that require high barrier properties and enhanced mechanical strength. These films are commonly used in the packaging of perishable goods, such as meats and cheeses, where maintaining freshness and extending shelf life are critical. The seven-layer structure allows for the incorporation of specialized materials that provide excellent barrier properties against gases and moisture, ensuring that the packaged products remain fresh for longer periods. Nine-layer films represent a further advancement in coextruded multilayer film technology, offering superior barrier properties and mechanical strength. These films are often used in high-performance packaging applications, such as vacuum packaging and modified atmosphere packaging, where maintaining product integrity is essential. The nine-layer structure allows for the inclusion of multiple functional layers, each designed to address specific packaging challenges, such as providing a barrier to oxygen, moisture, and light. Eleven-layer films are at the forefront of coextruded multilayer film technology, offering unparalleled barrier properties and mechanical strength. These films are used in the most demanding packaging applications, where maintaining product quality and extending shelf life are of utmost importance. The eleven-layer structure allows for the incorporation of a wide range of materials, each selected for its specific properties, such as providing a barrier to gases, moisture, and light, or enhancing the film's strength and flexibility. Other multilayer films, which may have more than eleven layers, are designed for specialized applications that require unique combinations of properties. These films are often used in niche markets where specific packaging challenges need to be addressed, such as in the packaging of highly sensitive products or in applications where extreme environmental conditions are a factor. The ability to customize the film's properties by varying the number and type of layers makes coextruded multilayer films a versatile solution for a wide range of packaging needs.

Food Packaging, Pharmaceutical Packaging, Others in the Global Coextruded Multilayer Films Market:

The Global Coextruded Multilayer Films Market finds extensive usage in various sectors, with food packaging being one of the most significant areas of application. In the food industry, these films are used to package a wide range of products, from fresh produce to processed foods. The multilayer structure of these films provides excellent barrier properties, protecting the contents from moisture, oxygen, and other environmental factors that can lead to spoilage. This helps in extending the shelf life of food products, reducing food waste, and ensuring that consumers receive fresh and high-quality products. Additionally, coextruded multilayer films can be designed to be transparent, allowing consumers to see the product inside, which is an important factor in purchasing decisions. In the pharmaceutical industry, coextruded multilayer films are used for packaging a variety of products, including tablets, capsules, and medical devices. The films provide a high level of protection against moisture, oxygen, and light, which can degrade the quality and efficacy of pharmaceutical products. By maintaining the integrity of the packaging, these films help ensure that patients receive safe and effective medications. Furthermore, the ability to customize the film's properties allows manufacturers to meet specific regulatory requirements and standards, which is crucial in the highly regulated pharmaceutical industry. Beyond food and pharmaceuticals, coextruded multilayer films are used in a variety of other applications, such as in the packaging of personal care products, electronics, and industrial goods. In the personal care industry, these films are used to package products like shampoos, lotions, and creams, providing a barrier against moisture and contaminants. In the electronics industry, coextruded multilayer films are used to package sensitive components, protecting them from static electricity and environmental factors that can cause damage. In industrial applications, these films are used to package a wide range of products, from chemicals to automotive parts, providing protection during storage and transportation. The versatility of coextruded multilayer films makes them an ideal solution for a wide range of packaging needs. Their ability to provide superior barrier properties, mechanical strength, and customization options allows manufacturers to meet the specific requirements of different industries. As the demand for efficient and sustainable packaging solutions continues to grow, the Global Coextruded Multilayer Films Market is well-positioned to provide innovative solutions that cater to the diverse needs of various sectors.

Global Coextruded Multilayer Films Market Outlook:

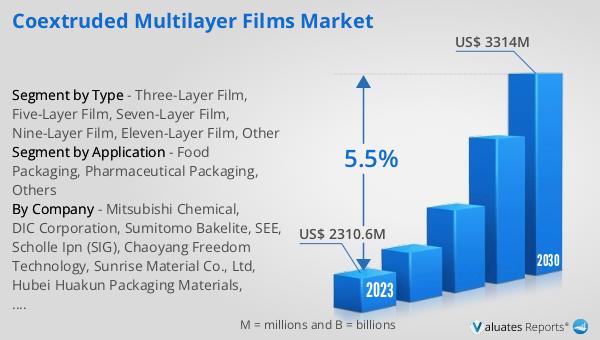

The global market for Coextruded Multilayer Films was valued at $2,526 million in 2024 and is anticipated to grow to a revised size of $3,648 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.5% over the forecast period. The market is dominated by the top four manufacturers, who collectively hold a share exceeding 81%. Among the various product types, the three-layer film segment emerges as the largest, accounting for over 40% of the market share. This segment's prominence is attributed to its cost-effectiveness and sufficient barrier properties for a wide range of applications. In terms of application, food packaging stands out as the largest segment, capturing over 46% of the market share. The demand for coextruded multilayer films in food packaging is driven by the need for efficient packaging solutions that extend shelf life and maintain product quality. As industries continue to prioritize sustainability and efficiency in packaging, the Global Coextruded Multilayer Films Market is expected to witness significant growth, offering versatile solutions that cater to the diverse needs of various sectors.

| Report Metric | Details |

| Report Name | Coextruded Multilayer Films Market |

| Accounted market size in year | US$ 2526 million |

| Forecasted market size in 2031 | US$ 3648 million |

| CAGR | 5.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Mitsubishi Chemical, DIC Corporation, Sumitomo Bakelite, SEE, Scholle Ipn (SIG), Chaoyang Freedom Technology, Sunrise Material Co., Ltd, Hubei Huakun Packaging Materials, Jiangsu Best New Medical Material Co, Ltd.(BEST), Chuangfa Materials, Wenzhou Chuangjia Packaging Material Co., Ltd., Green Packaging Material (Jiangyin) Co., Ltd., Henan Yinfeng Plastic Co., Ltd., Shandong Ujoin Medical Technology Co., Ltd., Luoyang Shengpeng New Material Technology, Baixin New Material |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |