What is Global Semiconductor Pressure Sensor Market?

The Global Semiconductor Pressure Sensor Market is a dynamic and rapidly evolving sector that plays a crucial role in various industries. These sensors are integral components in devices that require precise pressure measurement and control. They are used in a wide range of applications, from automotive and healthcare to industrial and consumer electronics. The market is driven by the increasing demand for advanced electronic devices and the growing need for automation in various sectors. Semiconductor pressure sensors are known for their accuracy, reliability, and ability to operate in harsh environments, making them ideal for critical applications. The market is characterized by continuous technological advancements, with manufacturers focusing on developing sensors with enhanced performance and reduced size. Additionally, the rise of the Internet of Things (IoT) and smart technologies has further fueled the demand for these sensors, as they are essential for monitoring and controlling various parameters in connected devices. As industries continue to embrace digital transformation, the Global Semiconductor Pressure Sensor Market is expected to witness significant growth, driven by innovations and the increasing adoption of smart technologies across different sectors.

MEMS Pressure Sensor, Diaphragm Pressure Sensor in the Global Semiconductor Pressure Sensor Market:

MEMS (Micro-Electro-Mechanical Systems) pressure sensors and diaphragm pressure sensors are two prominent types of sensors within the Global Semiconductor Pressure Sensor Market. MEMS pressure sensors are miniature devices that integrate mechanical and electrical components at a microscale. They are widely used due to their small size, low power consumption, and high sensitivity. These sensors operate by converting pressure into an electrical signal, which can then be measured and analyzed. MEMS pressure sensors are commonly found in automotive applications, such as tire pressure monitoring systems and engine control units, where precise pressure measurement is crucial for optimal performance and safety. They are also used in medical devices, such as blood pressure monitors and respiratory equipment, where accuracy and reliability are paramount. On the other hand, diaphragm pressure sensors utilize a flexible diaphragm that deforms under pressure, causing a change in capacitance or resistance, which is then converted into an electrical signal. These sensors are known for their robustness and ability to withstand high pressures, making them suitable for industrial applications, such as process control and monitoring in manufacturing plants. Diaphragm pressure sensors are also used in HVAC systems, where they help maintain optimal environmental conditions by monitoring and controlling air pressure. Both MEMS and diaphragm pressure sensors are integral to the Global Semiconductor Pressure Sensor Market, offering unique advantages that cater to different application needs. As technology continues to advance, these sensors are expected to become even more sophisticated, with improved performance and expanded capabilities, further driving their adoption across various industries.

Gas Supply System, Thin Film Deposition Apparatus, Semiconductor Cleaning Equipment, Etching Equipment, Others in the Global Semiconductor Pressure Sensor Market:

The Global Semiconductor Pressure Sensor Market finds extensive usage in several critical areas, including gas supply systems, thin film deposition apparatus, semiconductor cleaning equipment, etching equipment, and others. In gas supply systems, semiconductor pressure sensors are essential for monitoring and controlling gas flow and pressure, ensuring safe and efficient operation. These sensors help prevent leaks and maintain optimal pressure levels, which is crucial for the safe handling of gases used in various industrial processes. In thin film deposition apparatus, pressure sensors play a vital role in maintaining the precise pressure conditions required for the deposition of thin films on substrates. This process is critical in the manufacturing of semiconductors and other electronic components, where even slight deviations in pressure can affect the quality and performance of the final product. Semiconductor cleaning equipment also relies on pressure sensors to ensure the effective removal of contaminants from semiconductor wafers. Accurate pressure measurement is essential in these systems to achieve the desired cleaning results without damaging the delicate wafers. Similarly, in etching equipment, pressure sensors are used to control the etching process, which involves the removal of material from the surface of a semiconductor wafer. Precise pressure control is necessary to achieve the desired etching depth and pattern, which are critical for the functionality of the final semiconductor device. Beyond these specific applications, semiconductor pressure sensors are also used in various other areas, such as environmental monitoring, aerospace, and consumer electronics, where they provide reliable and accurate pressure measurement for a wide range of applications. As industries continue to advance and demand more sophisticated technologies, the role of semiconductor pressure sensors in these areas is expected to grow, driven by the need for precision, reliability, and efficiency in pressure measurement and control.

Global Semiconductor Pressure Sensor Market Outlook:

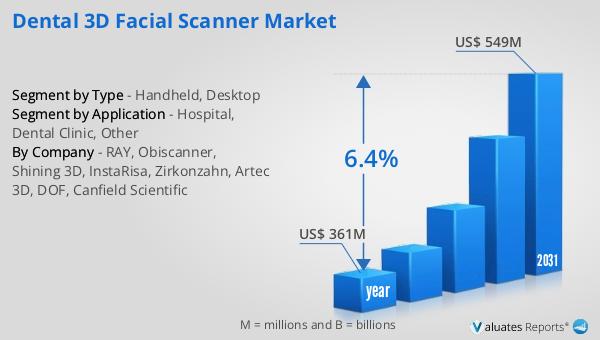

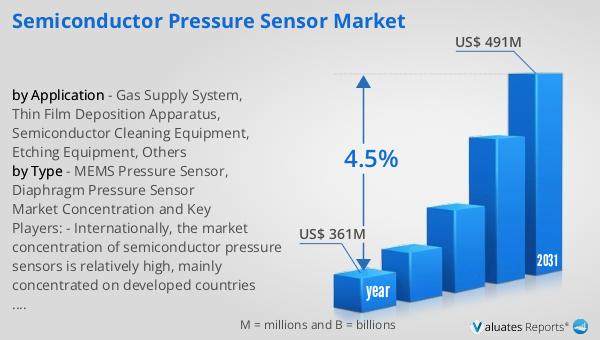

The global market for semiconductor pressure sensors was valued at $361 million in 2024 and is anticipated to expand to a revised size of $491 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.5% over the forecast period. This growth trajectory underscores the increasing demand for semiconductor pressure sensors across various industries. The market's expansion is driven by the rising adoption of these sensors in automotive, healthcare, and industrial applications, where precise pressure measurement is crucial. The automotive industry, in particular, is a significant contributor to this growth, as semiconductor pressure sensors are essential for various applications, including tire pressure monitoring systems, engine control units, and advanced driver-assistance systems (ADAS). In the healthcare sector, the demand for accurate and reliable pressure sensors is growing, driven by the increasing use of medical devices that require precise pressure measurement, such as blood pressure monitors and respiratory equipment. Additionally, the industrial sector is witnessing a surge in demand for semiconductor pressure sensors, as industries increasingly adopt automation and smart technologies to enhance efficiency and productivity. The market's growth is further supported by continuous technological advancements, with manufacturers focusing on developing sensors with enhanced performance, reduced size, and improved reliability. As the global market for semiconductor pressure sensors continues to evolve, it is expected to witness significant growth, driven by innovations and the increasing adoption of smart technologies across different sectors.

| Report Metric | Details |

| Report Name | Semiconductor Pressure Sensor Market |

| Accounted market size in year | US$ 361 million |

| Forecasted market size in 2031 | US$ 491 million |

| CAGR | 4.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | WIKA, Nidec, Nagano Keiki, Setra, MKS Instruments, Entegris, Brooks Instrument, WISE Control, OMEGA, Tem-Tech Lab (Azbil), Valcom |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |