What is Global Aircraft Fuel Gauging System Market?

The Global Aircraft Fuel Gauging System Market is a specialized segment within the aviation industry that focuses on the development, production, and implementation of systems used to measure and monitor the fuel levels in aircraft. These systems are crucial for ensuring the safe and efficient operation of aircraft, as they provide pilots and ground crew with accurate information about fuel quantity, helping to prevent fuel exhaustion and optimize fuel management. The market encompasses a range of technologies and solutions, including both traditional mechanical systems and advanced electronic systems that utilize sensors and digital displays. As the aviation industry continues to grow, driven by increasing air travel demand and advancements in aircraft technology, the need for reliable and precise fuel gauging systems becomes even more critical. This market is influenced by factors such as regulatory requirements, technological advancements, and the ongoing push for more fuel-efficient and environmentally friendly aircraft. Companies operating in this market are continually innovating to improve the accuracy, reliability, and ease of use of their fuel gauging systems, ensuring they meet the evolving needs of both commercial and military aviation sectors.

Contact Type, Contactless Type in the Global Aircraft Fuel Gauging System Market:

In the Global Aircraft Fuel Gauging System Market, there are two primary types of systems: contact type and contactless type. Contact type fuel gauging systems are traditional systems that rely on physical contact with the fuel to measure its level. These systems typically use float-based mechanisms, where a float moves up and down with the fuel level, and this movement is translated into a readable measurement. The advantage of contact type systems is their simplicity and reliability, as they have been used for many years and are well-understood by industry professionals. However, they can be susceptible to wear and tear over time, and their mechanical nature may limit their precision compared to more modern systems. On the other hand, contactless type fuel gauging systems represent a more advanced approach, utilizing technologies such as capacitance, ultrasonic, or radar to measure fuel levels without direct contact. These systems offer several benefits, including higher accuracy, reduced maintenance needs, and the ability to function effectively in a wider range of environmental conditions. Capacitance-based systems, for example, measure changes in capacitance caused by the presence of fuel, providing a precise and reliable measurement. Ultrasonic systems use sound waves to determine fuel levels, while radar systems employ electromagnetic waves. The contactless approach is particularly advantageous in modern aircraft, where precision and reliability are paramount. As aircraft technology continues to evolve, the demand for contactless fuel gauging systems is expected to grow, driven by their ability to integrate seamlessly with other advanced avionics systems and provide real-time data to pilots and ground crew. Both contact and contactless systems play vital roles in the aviation industry, and the choice between them often depends on factors such as the specific requirements of the aircraft, cost considerations, and the desired level of technological sophistication. Companies in the Global Aircraft Fuel Gauging System Market are continually working to enhance the capabilities of both types of systems, ensuring they meet the diverse needs of the aviation sector.

Civil Aviation, Military Aviation in the Global Aircraft Fuel Gauging System Market:

The usage of Global Aircraft Fuel Gauging System Market in civil aviation is pivotal for ensuring the safety and efficiency of commercial flights. In civil aviation, accurate fuel gauging is essential for flight planning, as it allows airlines to optimize fuel loads, reduce costs, and minimize environmental impact. Fuel gauging systems provide pilots with real-time data on fuel levels, enabling them to make informed decisions about fuel management during flights. This is particularly important for long-haul flights, where precise fuel calculations are necessary to ensure the aircraft can reach its destination without the need for unscheduled refueling stops. Additionally, fuel gauging systems help airlines comply with regulatory requirements related to fuel management and safety. In military aviation, the role of fuel gauging systems is equally critical. Military aircraft often operate in challenging environments and under demanding conditions, where accurate fuel management is crucial for mission success. Fuel gauging systems in military aviation must be robust and reliable, capable of providing precise measurements even in extreme conditions. These systems support a wide range of military operations, from routine training flights to complex combat missions, where fuel availability can be a determining factor in mission outcomes. Furthermore, military aircraft may require specialized fuel gauging systems that can accommodate unique fuel types or configurations, adding another layer of complexity to their design and implementation. Overall, the Global Aircraft Fuel Gauging System Market plays a vital role in both civil and military aviation, providing the tools necessary for safe, efficient, and effective fuel management across a wide range of aircraft and operational scenarios.

Global Aircraft Fuel Gauging System Market Outlook:

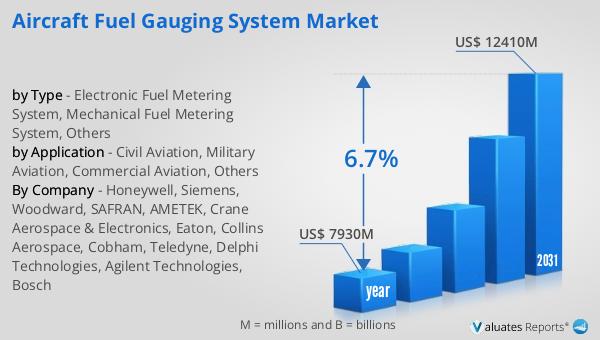

The global market for Aircraft Fuel Gauging Systems was valued at $281 million in 2024, and it is anticipated to expand to a revised size of $410 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.4% over the forecast period. This growth trajectory underscores the increasing demand for advanced fuel gauging systems in the aviation industry, driven by factors such as the rising number of aircraft in operation, advancements in aviation technology, and the need for more efficient fuel management solutions. As airlines and military organizations continue to prioritize safety, efficiency, and environmental sustainability, the adoption of sophisticated fuel gauging systems is expected to rise. These systems not only enhance the accuracy of fuel measurements but also integrate seamlessly with other avionics systems, providing comprehensive data to pilots and ground crew. The projected growth of the market highlights the ongoing innovation and development within the industry, as companies strive to meet the evolving needs of their customers and address the challenges of modern aviation. With a focus on improving accuracy, reliability, and ease of use, the Global Aircraft Fuel Gauging System Market is poised for significant expansion in the coming years, offering numerous opportunities for stakeholders across the aviation sector.

| Report Metric | Details |

| Report Name | Aircraft Fuel Gauging System Market |

| Accounted market size in year | US$ 281 million |

| Forecasted market size in 2031 | US$ 410 million |

| CAGR | 5.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Safran Group, AMETEK, Crane Aerospace & Electronics, Eaton Corporation, RTX Corporation, Liquid Measurement Systems, Parker Hannifin |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |