What is Global Petroleum Sponge Coke Market?

The Global Petroleum Sponge Coke Market is a significant segment within the broader petroleum industry, focusing on the production and distribution of sponge coke, a byproduct of the oil refining process. Sponge coke is a type of petroleum coke characterized by its porous structure, which resembles a sponge. This material is primarily produced during the thermal cracking process in refineries, where heavy crude oil is broken down into lighter products. The global market for sponge coke is driven by its applications in various industries, including energy, metallurgy, and manufacturing. As a solid carbon material, sponge coke is used as a fuel source and as a raw material in the production of aluminum, steel, and other metals. The market is influenced by factors such as crude oil prices, refining capacities, and environmental regulations. With the increasing demand for energy and industrial materials, the Global Petroleum Sponge Coke Market is expected to grow, offering opportunities for stakeholders across the supply chain. The market's dynamics are shaped by technological advancements, regional production capacities, and the evolving needs of end-user industries. As such, it remains a crucial component of the global energy and materials landscape.

High-Sulfur Petroleum Sponge Coke, Middle-Sulfur Petroleum Sponge Coke, Low-Sulfur Petroleum Sponge Coke in the Global Petroleum Sponge Coke Market:

High-Sulfur Petroleum Sponge Coke, Middle-Sulfur Petroleum Sponge Coke, and Low-Sulfur Petroleum Sponge Coke are distinct categories within the Global Petroleum Sponge Coke Market, each defined by their sulfur content and specific applications. High-Sulfur Petroleum Sponge Coke contains a higher percentage of sulfur, typically above 3%, making it less desirable for certain applications due to environmental concerns. However, it is often used in industries where sulfur emissions are less of a concern or where sulfur can be removed during processing. This type of coke is commonly utilized in power generation and cement industries, where it serves as a cost-effective fuel source. Middle-Sulfur Petroleum Sponge Coke, with sulfur content ranging between 1% and 3%, strikes a balance between cost and environmental impact. It is used in applications where moderate sulfur levels are acceptable, such as in some metallurgical processes and in the production of certain chemicals. This category of sponge coke is often preferred for its versatility and relatively lower environmental footprint compared to high-sulfur variants. Low-Sulfur Petroleum Sponge Coke, containing less than 1% sulfur, is the most environmentally friendly option among the three. It is highly sought after in industries where stringent environmental regulations are in place, such as in the production of aluminum and other non-ferrous metals. The low sulfur content minimizes emissions of sulfur dioxide, a major pollutant, making it a preferred choice for applications requiring cleaner combustion. The demand for low-sulfur sponge coke is driven by the increasing focus on reducing industrial emissions and adhering to environmental standards. Each type of petroleum sponge coke serves specific market needs, influenced by factors such as cost, availability, and regulatory requirements. The choice between high, middle, and low-sulfur sponge coke depends on the intended application, environmental considerations, and economic factors. As industries continue to evolve and prioritize sustainability, the demand for low-sulfur options is expected to rise, while high-sulfur variants may face challenges due to tightening environmental regulations. The Global Petroleum Sponge Coke Market is thus characterized by a diverse range of products catering to different industrial needs, with sulfur content being a key differentiator.

Solid Fuel, Other in the Global Petroleum Sponge Coke Market:

The Global Petroleum Sponge Coke Market finds its usage in various areas, with solid fuel being one of the primary applications. As a solid fuel, sponge coke is utilized in power plants and industrial boilers, where it serves as an efficient and cost-effective energy source. Its high carbon content and calorific value make it an attractive option for energy generation, particularly in regions with abundant supply and less stringent environmental regulations. In addition to power generation, sponge coke is used in the cement industry as a fuel for kilns, contributing to the production of clinker, the primary component of cement. The use of sponge coke in these applications is driven by its availability, cost-effectiveness, and energy efficiency. Beyond its role as a solid fuel, sponge coke has other applications in various industries. It is used as a raw material in the production of aluminum, where it serves as a carbon source in the electrolytic reduction of alumina. The low-sulfur variant of sponge coke is particularly favored in this application due to its minimal environmental impact. Additionally, sponge coke is used in the steel industry as a reducing agent in blast furnaces, where it helps convert iron ore into molten iron. Its high carbon content and low ash levels make it suitable for this purpose, contributing to the efficiency of the steelmaking process. Sponge coke is also employed in the production of titanium dioxide, a white pigment used in paints, coatings, and plastics. In this application, sponge coke acts as a reducing agent, facilitating the conversion of titanium ore into titanium dioxide. The versatility of sponge coke extends to its use in the production of electrodes for electric arc furnaces, where it is processed into calcined petroleum coke. This form of coke is essential in the production of graphite electrodes, which are used in steelmaking and other metallurgical processes. The Global Petroleum Sponge Coke Market thus plays a crucial role in supporting various industrial activities, with its applications spanning energy generation, metallurgy, and chemical production. The market's growth is influenced by factors such as industrial demand, environmental regulations, and technological advancements, which shape the usage patterns of sponge coke across different sectors. As industries continue to seek cost-effective and efficient energy sources, the demand for sponge coke is expected to remain robust, with its applications evolving to meet changing market needs.

Global Petroleum Sponge Coke Market Outlook:

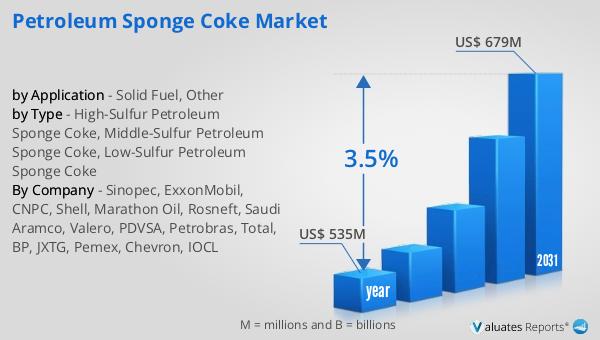

The global market for Petroleum Sponge Coke was valued at $535 million in 2024 and is anticipated to expand to a revised size of $679 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.5% over the forecast period. This growth trajectory underscores the increasing demand for sponge coke across various industries, driven by its applications as a solid fuel and raw material in metallurgical and chemical processes. The market's expansion is supported by factors such as rising energy needs, industrial growth, and the ongoing shift towards more sustainable and efficient energy sources. As industries continue to evolve and adapt to changing environmental regulations, the demand for low-sulfur sponge coke is expected to rise, contributing to the market's overall growth. The projected increase in market size highlights the importance of sponge coke as a critical component in the global energy and materials landscape, with its applications spanning power generation, metallurgy, and chemical production. The market's growth is also influenced by technological advancements and regional production capacities, which shape the supply and demand dynamics of sponge coke. As such, the Global Petroleum Sponge Coke Market is poised for continued expansion, offering opportunities for stakeholders across the supply chain to capitalize on the growing demand for this versatile material.

| Report Metric | Details |

| Report Name | Petroleum Sponge Coke Market |

| Accounted market size in year | US$ 535 million |

| Forecasted market size in 2031 | US$ 679 million |

| CAGR | 3.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Sinopec, ExxonMobil, CNPC, Shell, Marathon Oil, Rosneft, Saudi Aramco, Valero, PDVSA, Petrobras, Total, BP, JXTG, Pemex, Chevron, IOCL |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |