What is Global Earthquake Resistant Ductile Iron Pipe Market?

The Global Earthquake Resistant Ductile Iron Pipe Market is a specialized segment within the broader infrastructure and construction industry. These pipes are designed to withstand seismic activities, making them crucial in regions prone to earthquakes. Ductile iron pipes are known for their strength, durability, and flexibility, which are essential characteristics for maintaining the integrity of pipelines during seismic events. The market for these pipes is driven by the increasing need for resilient infrastructure that can endure natural disasters, ensuring the continuous supply of water, gas, and other essential services. As urbanization and industrialization continue to expand globally, the demand for earthquake-resistant ductile iron pipes is expected to grow. These pipes are not only used in new construction projects but also in the retrofitting of existing infrastructure to enhance their earthquake resilience. The market is characterized by technological advancements aimed at improving the performance and cost-effectiveness of these pipes. Manufacturers are focusing on innovation to meet the stringent safety standards and regulations imposed by governments and international bodies. Overall, the Global Earthquake Resistant Ductile Iron Pipe Market plays a vital role in safeguarding infrastructure and ensuring the safety and well-being of communities in earthquake-prone areas.

DN 80mm-300mm, DN 350mm-1000mm, DN 1100mm-1200mm, DN 1400mm-2000mm, Others in the Global Earthquake Resistant Ductile Iron Pipe Market:

The Global Earthquake Resistant Ductile Iron Pipe Market is segmented based on the diameter of the pipes, which determines their specific applications and suitability for different projects. The DN 80mm-300mm segment includes smaller diameter pipes that are typically used in residential and small commercial applications. These pipes are ideal for distributing water and gas in urban areas where space is limited, and flexibility is crucial to accommodate ground movements during earthquakes. The DN 350mm-1000mm segment encompasses medium-sized pipes that are commonly used in municipal water supply systems, sewage networks, and industrial applications. These pipes offer a balance between strength and flexibility, making them suitable for a wide range of infrastructure projects. The DN 1100mm-1200mm segment includes larger diameter pipes that are often used in major water transmission projects, such as aqueducts and large-scale irrigation systems. These pipes are designed to handle high volumes of water and withstand significant pressure, ensuring the reliability of critical infrastructure during seismic events. The DN 1400mm-2000mm segment represents the largest diameter pipes, which are used in specialized applications such as large-scale water transfer projects, flood control systems, and major industrial installations. These pipes are engineered to provide maximum strength and durability, capable of withstanding the most severe seismic forces. The "Others" category includes pipes with non-standard diameters or those designed for specific applications, such as custom projects or unique environmental conditions. Each segment of the Global Earthquake Resistant Ductile Iron Pipe Market is tailored to meet the specific needs of different infrastructure projects, ensuring that pipelines remain operational and secure during and after earthquakes. The market's segmentation allows for targeted solutions that address the diverse requirements of various industries and regions, contributing to the overall resilience and sustainability of global infrastructure.

Wastewater Treatment, Offshore, Gas and Oil, Mining, Other in the Global Earthquake Resistant Ductile Iron Pipe Market:

The Global Earthquake Resistant Ductile Iron Pipe Market finds extensive usage across various sectors, each with unique requirements and challenges. In wastewater treatment, these pipes are essential for transporting sewage and treated water, ensuring that wastewater systems remain operational during seismic events. The flexibility and strength of ductile iron pipes make them ideal for handling the dynamic loads and ground movements associated with earthquakes, preventing leaks and maintaining the integrity of wastewater infrastructure. In offshore applications, earthquake-resistant ductile iron pipes are used in the construction of underwater pipelines and structures. These pipes must withstand not only seismic forces but also the harsh marine environment, including corrosion and pressure from water currents. Their durability and resistance to external forces make them a reliable choice for offshore oil and gas exploration, as well as other marine infrastructure projects. In the gas and oil industry, these pipes are crucial for the safe and efficient transportation of hydrocarbons. Earthquake-resistant ductile iron pipes help prevent pipeline failures and leaks, which can have catastrophic environmental and economic consequences. Their ability to absorb seismic energy and maintain structural integrity ensures the continuous flow of oil and gas, even in earthquake-prone regions. In mining, these pipes are used to transport water, slurry, and other materials essential for mining operations. The rugged conditions of mining sites, combined with the risk of seismic activity, require pipes that can withstand both physical and environmental stresses. Earthquake-resistant ductile iron pipes provide the necessary durability and flexibility to support mining operations, ensuring the safety and efficiency of material transport. The "Other" category includes various applications where earthquake-resistant ductile iron pipes are used, such as in agriculture, construction, and industrial processes. These pipes offer a versatile solution for any project requiring robust and reliable pipeline infrastructure capable of withstanding seismic forces. Overall, the Global Earthquake Resistant Ductile Iron Pipe Market plays a critical role in ensuring the resilience and reliability of infrastructure across multiple sectors, safeguarding essential services and resources in the face of natural disasters.

Global Earthquake Resistant Ductile Iron Pipe Market Outlook:

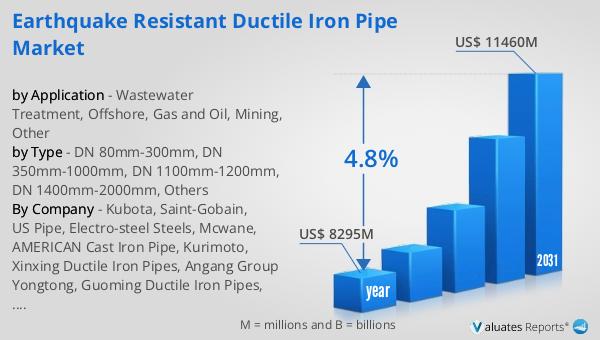

In 2024, the global market for Earthquake Resistant Ductile Iron Pipes was valued at approximately $8,295 million. This market is anticipated to expand significantly, reaching an estimated size of $11,460 million by 2031. This growth trajectory reflects a compound annual growth rate (CAGR) of 4.8% over the forecast period. The increasing demand for resilient infrastructure, particularly in earthquake-prone regions, is a key driver of this market expansion. As urbanization and industrialization continue to rise, the need for durable and flexible pipeline solutions becomes more critical. Earthquake-resistant ductile iron pipes offer a reliable option for maintaining the integrity of essential services such as water, gas, and sewage systems during seismic events. The market's growth is also supported by technological advancements and innovations aimed at enhancing the performance and cost-effectiveness of these pipes. Manufacturers are investing in research and development to meet the stringent safety standards and regulations imposed by governments and international bodies. This focus on innovation ensures that the market remains competitive and capable of addressing the evolving needs of infrastructure projects worldwide. Overall, the Global Earthquake Resistant Ductile Iron Pipe Market is poised for steady growth, driven by the increasing emphasis on infrastructure resilience and sustainability.

| Report Metric | Details |

| Report Name | Earthquake Resistant Ductile Iron Pipe Market |

| Accounted market size in year | US$ 8295 million |

| Forecasted market size in 2031 | US$ 11460 million |

| CAGR | 4.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Kubota, Saint-Gobain, US Pipe, Electro-steel Steels, Mcwane, AMERICAN Cast Iron Pipe, Kurimoto, Xinxing Ductile Iron Pipes, Angang Group Yongtong, Guoming Ductile Iron Pipes, Jindal SAW, Tubos |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |