What is Global Semiconductor and Integrated Circuit Market?

The global semiconductor and integrated circuit market is a vast and dynamic industry that plays a crucial role in the functioning of modern technology. Semiconductors are materials that have electrical conductivity between a conductor and an insulator, making them essential for creating integrated circuits (ICs). These ICs are the building blocks of electronic devices, enabling the processing and storage of data. The market encompasses a wide range of products, including microprocessors, memory chips, and various types of ICs, each serving different functions in electronic devices. The demand for semiconductors and ICs is driven by the rapid advancement of technology and the increasing need for more powerful and efficient electronic devices. This market is characterized by continuous innovation and fierce competition among key players, who strive to develop smaller, faster, and more energy-efficient components. The global semiconductor and IC market is integral to numerous industries, including consumer electronics, automotive, telecommunications, and healthcare, making it a critical component of the global economy. As technology continues to evolve, the semiconductor and IC market is expected to grow, driven by emerging trends such as the Internet of Things (IoT), artificial intelligence (AI), and 5G connectivity.

Logic IC, Memory IC, Analog IC, Micro IC, Semiconductor Discretes, Optoelectronics, Sensors in the Global Semiconductor and Integrated Circuit Market:

Logic ICs, Memory ICs, Analog ICs, Micro ICs, Semiconductor Discretes, Optoelectronics, and Sensors are all vital components of the global semiconductor and integrated circuit market, each serving distinct roles in the functionality of electronic devices. Logic ICs are fundamental to digital circuits, performing essential operations such as data processing, decision-making, and control functions. They are the brains behind computing devices, enabling complex computations and the execution of software applications. Memory ICs, on the other hand, are responsible for storing data and instructions that devices need to operate. They come in various forms, including volatile memory like RAM, which temporarily holds data for quick access, and non-volatile memory like flash, which retains data even when the power is off. Analog ICs are crucial for interfacing digital systems with the real world, as they handle continuous signals such as sound, light, and temperature. These ICs are used in applications ranging from audio amplifiers to power management systems. Micro ICs, or microcontrollers, are compact integrated circuits that contain a processor, memory, and input/output peripherals on a single chip. They are used in a wide range of applications, from household appliances to industrial automation, providing control and processing capabilities. Semiconductor discretes, such as diodes and transistors, are individual semiconductor devices that perform specific functions like switching, amplifying, or rectifying electrical signals. They are essential components in power electronics and signal processing. Optoelectronics involves the use of semiconductor devices that emit, detect, or control light. This includes components like LEDs, photodiodes, and laser diodes, which are used in applications ranging from lighting to fiber-optic communications. Sensors, another critical category, are devices that detect changes in physical conditions or chemical compositions and convert them into electrical signals. They are used in a wide array of applications, including automotive systems, industrial automation, and consumer electronics, providing critical data for monitoring and control. Each of these components plays a unique role in the semiconductor and IC market, contributing to the development of advanced electronic systems that power modern technology.

Mobile Devices, PCs/Laptop/Tablet, Automotive, Industrial & Medical, Servers & Data Center & AI, Network Infrastructure, Appliances/Consumer Goods/IoT, Aerospace & Defense, Government and Others in the Global Semiconductor and Integrated Circuit Market:

The global semiconductor and integrated circuit market finds extensive usage across various sectors, each leveraging the unique capabilities of these components to enhance functionality and performance. In mobile devices, semiconductors and ICs are crucial for enabling high-speed processing, efficient power management, and advanced connectivity features. They support the operation of smartphones and tablets, providing the computational power needed for applications, multimedia, and communication. PCs, laptops, and tablets also rely heavily on semiconductors and ICs for processing power, memory storage, and graphics capabilities, enabling users to perform complex tasks and run sophisticated software applications. In the automotive industry, semiconductors are integral to the development of advanced driver-assistance systems (ADAS), infotainment systems, and electric vehicle powertrains. They enable features such as collision avoidance, navigation, and energy-efficient propulsion. The industrial and medical sectors utilize semiconductors and ICs for automation, control systems, and diagnostic equipment, enhancing efficiency and precision in manufacturing and healthcare. Servers, data centers, and AI applications demand high-performance semiconductors to handle vast amounts of data and complex computations, supporting cloud computing, machine learning, and big data analytics. Network infrastructure relies on semiconductors for high-speed data transmission and connectivity, facilitating communication across global networks. In the realm of appliances, consumer goods, and IoT, semiconductors enable smart functionalities, connectivity, and energy efficiency, transforming everyday objects into intelligent devices. The aerospace and defense sectors use semiconductors for navigation, communication, and surveillance systems, ensuring reliability and performance in critical applications. Government and other sectors also benefit from semiconductors in various applications, from public safety to infrastructure management. Overall, the global semiconductor and IC market is a cornerstone of modern technology, driving innovation and progress across multiple industries.

Global Semiconductor and Integrated Circuit Market Outlook:

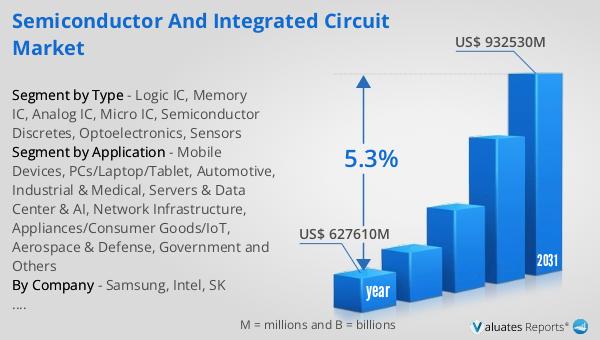

The global semiconductor and integrated circuit market was valued at $627.61 billion in 2024 and is anticipated to expand to $932.53 billion by 2031, reflecting a compound annual growth rate (CAGR) of 5.3% over the forecast period. The market's growth is driven by the increasing demand for advanced electronic devices and the continuous evolution of technology. In terms of business models, the fabless semiconductor segment generated $217.6 billion in revenue in 2023 and is expected to reach $500 billion by 2030, growing at a CAGR of 9.57% from 2024 to 2030. Meanwhile, the integrated device manufacturer (IDM) semiconductor segment recorded $345.3 billion in revenue in 2023, with projections to reach $574.5 billion by 2030, at a CAGR of 5.89% during the same period. The market is dominated by major players such as Intel, Samsung, NVIDIA, Qualcomm, Broadcom, SK Hynix, AMD, Texas Instruments, Infineon, STMicroelectronics, Micron Technology, MediaTek, NXP, and Western Digital. These top ten companies collectively held 55% of the global market share in 2023, with the top ten players accounting for approximately 74.4% of the market. In terms of chip segments, logic ICs were the largest in 2023, holding a 33% share, followed by memory, analog, and micro ICs. The analog IC market is projected to grow from $86 billion in 2023 to $113.96 billion by 2030, at a CAGR of 4.93% from 2024 to 2030. The micro IC market is expected to increase from $82.5 billion in 2023 to $122.4 billion by 2030, with a CAGR of 5.98% during the forecast period. The logic IC market is anticipated to grow from $190.6 billion in 2023 to $419.4 billion by 2030, at a CAGR of 9.49% from 2024 to 2030. The memory IC market is projected to expand from $98.9 billion in 2023 to $284 billion by 2030, at a CAGR of 7.87% during the forecast period. The semiconductor discretes market is expected to grow from $38.19 billion in 2023 to $50.8 billion by 2030, at a CAGR of 5.93% from 2024 to 2030.

| Report Metric | Details |

| Report Name | Semiconductor and Integrated Circuit Market |

| Accounted market size in year | US$ 627610 million |

| Forecasted market size in 2031 | US$ 932530 million |

| CAGR | 5.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Samsung, Intel, SK Hynix, Micron Technology, Texas Instruments (TI), STMicroelectronics, Kioxia, Sony Semiconductor Solutions Corporation (SSS), Infineon, NXP, Analog Devices, Inc. (ADI), Renesas Electronics, Microchip Technology, Onsemi, Western Digital (WD), NVIDIA, Qualcomm, Broadcom, Advanced Micro Devices, Inc. (AMD), MediaTek, Marvell Technology Group, Novatek Microelectronics Corp., Tsinghua Unigroup, Realtek Semiconductor Corporation, OmniVision Technology, Inc, Monolithic Power Systems, Inc. (MPS), Cirrus Logic, Inc., Socionext Inc., LX Semicon, HiSilicon Technologies, Synaptics, Allegro MicroSystems, Himax Technologies, Semtech, Global Unichip Corporation (GUC), Hygon Information Technology, GigaDevice, Silicon Motion, Ingenic Semiconductor, Raydium, Goodix Limited, Sitronix, Nordic Semiconductor, Silergy, Shanghai Fudan Microelectronics Group, Alchip Technologies, FocalTech, MegaChips Corporation, Elite Semiconductor Microelectronics Technology, SGMICRO, Winbond, Nanya Technology, Macronix, Mitsubishi Electric, Toshiba, Skyworks Solutions Inc, Vishay Technologies, Diodes Incorporated, ROHM, Nexperia, Hangzhou Silan Microelectronics, CR Micro, Fuji Electric, Yangzhou Yangjie Electronic Technology, Littelfuse, Alpha and Omega Semiconductor, Sanan Optoelectronics, Maxscend Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |