What is Global High Purity Indium Tin Oxide (ITO) Target (Purity Above 4N) Market?

The Global High Purity Indium Tin Oxide (ITO) Target market, specifically those with a purity above 4N, is a specialized segment within the materials industry that focuses on the production and distribution of ITO targets with high purity levels. These targets are essential components in the manufacturing of various electronic and optical devices. ITO is a mixture of indium oxide (In2O3) and tin oxide (SnO2) and is widely used due to its excellent electrical conductivity and optical transparency. The "4N" designation refers to a purity level of 99.99%, which is crucial for applications requiring minimal impurities to ensure optimal performance. The market for these high-purity ITO targets is driven by the increasing demand for advanced electronic devices, such as touch screens, flat-panel displays, and solar cells, where high transparency and conductivity are essential. As technology advances, the need for materials that can meet stringent performance criteria continues to grow, making the high-purity ITO target market a vital component of the broader electronics and materials sectors. The market's growth is also influenced by the ongoing research and development efforts aimed at improving the efficiency and performance of electronic devices.

5N, 6N, 7N, Others in the Global High Purity Indium Tin Oxide (ITO) Target (Purity Above 4N) Market:

In the realm of Global High Purity Indium Tin Oxide (ITO) Targets, the purity levels are categorized into different grades such as 5N, 6N, 7N, and others, each representing a higher degree of purity. The "N" in these designations stands for "nines," indicating the number of nines in the purity percentage. For instance, 5N signifies a purity of 99.999%, 6N is 99.9999%, and 7N is 99.99999%. These high-purity levels are crucial for applications that demand exceptional performance and minimal contamination. The 5N purity level is often used in applications where a balance between cost and performance is required. It is suitable for many consumer electronics and photovoltaic applications where high transparency and conductivity are necessary but where the absolute highest purity is not critical. As we move to 6N purity, the applications become more specialized. This level of purity is often required in high-end electronics and advanced optical devices where even the slightest impurity can affect performance. The 6N ITO targets are used in the production of high-resolution displays and sensitive touch panels, where clarity and precision are paramount. The 7N purity level represents the pinnacle of purity in ITO targets. This level is reserved for the most demanding applications, such as in research and development environments or in the production of cutting-edge technology where any impurity could lead to significant performance degradation. The production of 7N ITO targets involves highly sophisticated processes to ensure that the material meets the stringent purity requirements. Beyond these specific purity levels, there are other grades that may be used for niche applications or in experimental settings. These might include custom purity levels tailored to specific industrial needs or research purposes. The choice of purity level in ITO targets is often dictated by the specific requirements of the application, balancing the need for performance with cost considerations. As technology continues to evolve, the demand for higher purity levels is likely to increase, driving innovation and development in the production of ITO targets. This ongoing evolution highlights the importance of high-purity ITO targets in the advancement of modern technology, as they play a critical role in enabling the functionality and efficiency of a wide range of electronic and optical devices.

Photovoltaic, Consumer Electronics, Functional Glass, Other in the Global High Purity Indium Tin Oxide (ITO) Target (Purity Above 4N) Market:

The usage of Global High Purity Indium Tin Oxide (ITO) Targets with a purity above 4N spans several key areas, including photovoltaic, consumer electronics, functional glass, and other applications. In the photovoltaic sector, high-purity ITO targets are essential for the production of solar cells. Their excellent electrical conductivity and optical transparency make them ideal for use in thin-film solar panels, where they serve as a transparent conductive oxide layer. This layer is crucial for allowing sunlight to pass through while also conducting electricity, thereby improving the efficiency of solar cells. As the demand for renewable energy sources grows, the role of high-purity ITO targets in enhancing solar cell performance becomes increasingly important. In consumer electronics, high-purity ITO targets are widely used in the manufacturing of touch screens, flat-panel displays, and other electronic devices. The transparency and conductivity of ITO make it an ideal material for touch-sensitive surfaces, enabling the seamless interaction between users and their devices. High-purity ITO targets ensure that these devices operate with high precision and clarity, which is essential for delivering a superior user experience. The demand for high-quality displays and touch screens continues to drive the need for high-purity ITO targets in this sector. Functional glass is another area where high-purity ITO targets play a significant role. In this context, ITO is used to create coatings that provide anti-reflective, conductive, or other functional properties to glass surfaces. These coatings are used in a variety of applications, including architectural glass, automotive glass, and smart windows. The ability to control light transmission and conductivity in glass products is highly valued in industries seeking to enhance the performance and functionality of their products. Beyond these specific applications, high-purity ITO targets are also used in other areas such as research and development, where they are employed in the creation of advanced materials and devices. The versatility of ITO, combined with its unique properties, makes it a valuable material for a wide range of innovative applications. As technology continues to advance, the demand for high-purity ITO targets is expected to grow, driven by the need for materials that can meet the increasingly stringent performance requirements of modern electronic and optical devices.

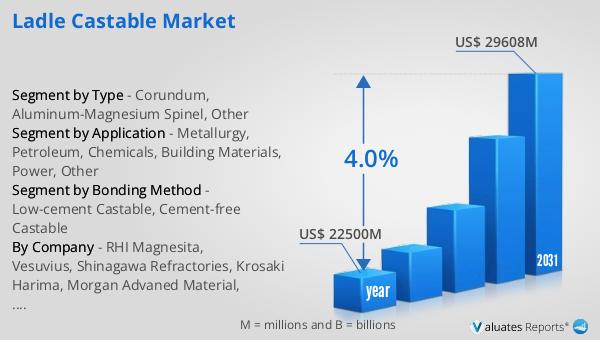

Global High Purity Indium Tin Oxide (ITO) Target (Purity Above 4N) Market Outlook:

The outlook for the global market of High Purity Indium Tin Oxide (ITO) Targets with a purity above 4N is promising, with significant growth anticipated over the coming years. The market is expected to expand from a valuation of US$ 658 million in 2024 to an impressive US$ 1250.8 million by 2030. This growth trajectory represents a robust Compound Annual Growth Rate (CAGR) of 11.3% during the forecast period. This upward trend is indicative of the increasing demand for high-purity ITO targets across various industries, driven by the need for advanced materials that can enhance the performance of electronic and optical devices. The growth in this market can be attributed to several factors, including the rising adoption of renewable energy technologies, the proliferation of consumer electronics, and the ongoing advancements in display technologies. As industries continue to seek materials that offer superior conductivity and transparency, high-purity ITO targets are poised to play a crucial role in meeting these demands. The market's expansion is also supported by the continuous research and development efforts aimed at improving the efficiency and performance of ITO targets, ensuring that they remain a vital component in the advancement of modern technology. This positive market outlook underscores the importance of high-purity ITO targets in the global materials industry and highlights their potential to drive innovation and growth in the years to come.

| Report Metric | Details |

| Report Name | High Purity Indium Tin Oxide (ITO) Target (Purity Above 4N) Market |

| Accounted market size in 2024 | US$ 658 million |

| Forecasted market size in 2030 | US$ 1250.8 million |

| CAGR | 11.3 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Mitsui Kinzoku, JX Nippon Mining & Metals, Tosoh, Vital, Lesker, American Elements, Stanford Advanced Materials, Premier Solutions, NC ELEMENTS, Rave Scientific, ENAM OPTOELECTRONIC MATERIAL, Guangxi Crystal Union Photoelectric Materials, Vital Thin Film Materials (Vital Group), Haohai Sputtering Targets (Haohai Metal Materials), OMAT Advanced Materials, Fujian Acetron New Materials, Wuhu Yingri Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |