What is Global Satellite Data Services Market?

The Global Satellite Data Services Market is a rapidly evolving sector that revolves around the collection, analysis, and dissemination of data obtained from satellites orbiting the Earth. These services are crucial for a wide range of applications, including environmental monitoring, urban planning, disaster management, and more. Satellites equipped with advanced sensors capture high-resolution images and other data types, which are then processed and analyzed to provide valuable insights. This market is driven by the increasing demand for real-time data and the growing need for accurate and timely information across various industries. The integration of satellite data with emerging technologies such as artificial intelligence and machine learning further enhances its utility, enabling more precise predictions and decision-making. As the world becomes more interconnected, the reliance on satellite data services is expected to grow, offering new opportunities for innovation and development in numerous fields. The market's expansion is also fueled by advancements in satellite technology, which have made data collection more efficient and cost-effective. Overall, the Global Satellite Data Services Market plays a pivotal role in shaping the future of data-driven decision-making across the globe.

Image Data, Data Analytics in the Global Satellite Data Services Market:

Image data and data analytics are integral components of the Global Satellite Data Services Market, providing essential insights and information for various applications. Image data refers to the visual information captured by satellites, which can include high-resolution photographs, thermal images, and multispectral data. These images are crucial for monitoring changes in the Earth's surface, such as deforestation, urban expansion, and natural disasters. By analyzing image data, organizations can gain a better understanding of environmental changes and make informed decisions. Data analytics, on the other hand, involves the processing and interpretation of satellite data to extract meaningful insights. This process often employs advanced algorithms and machine learning techniques to identify patterns and trends within the data. For instance, in agriculture, data analytics can be used to assess crop health, predict yields, and optimize resource allocation. In the energy sector, it can help in monitoring infrastructure and detecting anomalies. The integration of image data and data analytics allows for more accurate and timely information, enabling businesses and governments to respond effectively to various challenges. As technology continues to advance, the capabilities of satellite data services are expected to expand, offering even more sophisticated tools for analysis and decision-making. The combination of image data and data analytics is transforming the way we understand and interact with our world, providing a powerful tool for addressing complex global issues.

Energy & Power, Engineering & Infrastructure, Environmental, Agriculture, Maritime, Others in the Global Satellite Data Services Market:

The Global Satellite Data Services Market finds extensive applications across various sectors, including energy and power, engineering and infrastructure, environmental monitoring, agriculture, maritime, and others. In the energy and power sector, satellite data services are used to monitor and manage energy infrastructure, such as pipelines and power lines. They help in detecting leaks, assessing damage, and ensuring the efficient operation of energy systems. In engineering and infrastructure, satellite data provides valuable insights for urban planning, construction, and maintenance. It enables engineers to monitor structural integrity, assess land use, and plan for future developments. Environmental monitoring is another critical area where satellite data services play a vital role. They help in tracking climate change, monitoring natural disasters, and assessing the impact of human activities on the environment. In agriculture, satellite data is used to monitor crop health, optimize irrigation, and improve yield predictions. It provides farmers with the information needed to make informed decisions and enhance productivity. The maritime sector also benefits from satellite data services, which are used for navigation, monitoring sea traffic, and ensuring maritime safety. Additionally, satellite data services are used in various other fields, such as defense, telecommunications, and transportation, providing valuable insights and enhancing operational efficiency. Overall, the Global Satellite Data Services Market offers a wide range of applications that contribute to the advancement and sustainability of various industries.

Global Satellite Data Services Market Outlook:

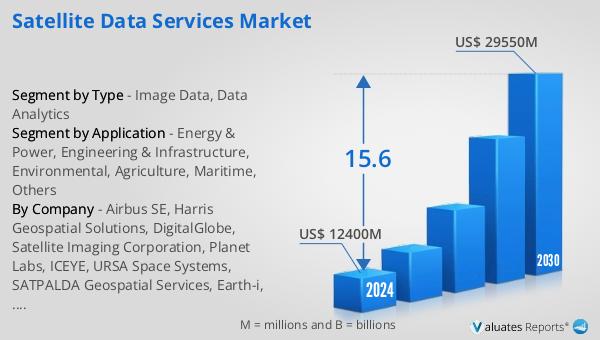

The Global Satellite Data Services Market is poised for significant growth in the coming years. According to market analysis, the market is expected to expand from $12,400 million in 2024 to $29,550 million by 2030, representing a compound annual growth rate (CAGR) of 15.6% during the forecast period. This growth is driven by the increasing demand for real-time data and the need for accurate and timely information across various industries. The integration of satellite data with emerging technologies such as artificial intelligence and machine learning is also contributing to the market's expansion. These technologies enhance the utility of satellite data, enabling more precise predictions and decision-making. Additionally, advancements in satellite technology have made data collection more efficient and cost-effective, further fueling the market's growth. As the world becomes more interconnected, the reliance on satellite data services is expected to increase, offering new opportunities for innovation and development in numerous fields. The Global Satellite Data Services Market is set to play a pivotal role in shaping the future of data-driven decision-making, providing valuable insights and information for a wide range of applications.

| Report Metric | Details |

| Report Name | Satellite Data Services Market |

| Accounted market size in 2024 | US$ 12400 million |

| Forecasted market size in 2030 | US$ 29550 million |

| CAGR | 15.6 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Airbus SE, Harris Geospatial Solutions, DigitalGlobe, Satellite Imaging Corporation, Planet Labs, ICEYE, URSA Space Systems, SATPALDA Geospatial Services, Earth-i, Land Info Worldwide Mapping |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |