What is Global High Flow Ventilator Market?

The Global High Flow Ventilator Market is a rapidly evolving segment within the medical device industry, focusing on devices that deliver high flow rates of oxygen to patients with respiratory distress. These ventilators are crucial in providing respiratory support to patients who cannot breathe adequately on their own, often due to conditions like chronic obstructive pulmonary disease (COPD), pneumonia, or COVID-19. High flow ventilators work by delivering a mixture of air and oxygen at a high flow rate, which helps to maintain adequate oxygen levels in the blood and reduce the work of breathing. The market for these devices has been expanding due to the increasing prevalence of respiratory diseases, advancements in technology, and the growing demand for non-invasive ventilation solutions. Additionally, the COVID-19 pandemic has significantly accelerated the demand for high flow ventilators, as they have been instrumental in managing severe respiratory cases. The market is characterized by a range of products, including portable and stationary units, catering to different healthcare settings such as hospitals, clinics, and home care. As healthcare systems worldwide continue to prioritize respiratory care, the Global High Flow Ventilator Market is expected to witness sustained growth and innovation.

Portable High Flow Ventilators, Trolley Mounted High Flow Ventilators in the Global High Flow Ventilator Market:

Portable High Flow Ventilators are a significant segment within the Global High Flow Ventilator Market, designed to offer flexibility and mobility in providing respiratory support. These devices are compact, lightweight, and easy to transport, making them ideal for use in various settings, including home care, emergency medical services, and field hospitals. Portable ventilators are equipped with advanced features such as battery operation, intuitive interfaces, and connectivity options, allowing healthcare providers to monitor and adjust treatment parameters remotely. They are particularly beneficial for patients who require continuous respiratory support but wish to maintain a level of independence and mobility. On the other hand, Trolley Mounted High Flow Ventilators are designed for more stationary use, typically in hospital settings. These ventilators are mounted on trolleys, allowing them to be easily moved within a healthcare facility. They are equipped with robust features, including advanced monitoring capabilities, customizable ventilation modes, and integration with hospital information systems. Trolley mounted ventilators are often used in intensive care units (ICUs), emergency departments, and operating rooms, where they provide critical respiratory support to patients with severe respiratory conditions. Both portable and trolley mounted high flow ventilators play a crucial role in the Global High Flow Ventilator Market, catering to the diverse needs of healthcare providers and patients. The choice between portable and trolley mounted ventilators depends on various factors, including the patient's condition, the healthcare setting, and the level of mobility required. As technology continues to advance, both types of ventilators are expected to incorporate more sophisticated features, enhancing their efficacy and ease of use. The growing demand for high flow ventilators, driven by the increasing prevalence of respiratory diseases and the need for effective respiratory support solutions, is expected to fuel the growth of the Global High Flow Ventilator Market in the coming years.

Hospital, Clinic, Ambulatory Surgical Centers in the Global High Flow Ventilator Market:

The usage of high flow ventilators in hospitals is critical, as these facilities are often the first point of care for patients with severe respiratory conditions. Hospitals utilize high flow ventilators in various departments, including intensive care units (ICUs), emergency departments, and general wards. In ICUs, high flow ventilators are used to provide life-saving respiratory support to critically ill patients, helping to stabilize their condition and improve their chances of recovery. In emergency departments, these ventilators are used to manage acute respiratory distress, providing immediate support to patients in critical condition. High flow ventilators are also used in general wards to support patients with less severe respiratory conditions, helping to prevent their condition from worsening and reducing the need for more invasive ventilation methods. Clinics also play a vital role in the Global High Flow Ventilator Market, as they provide outpatient care to patients with chronic respiratory conditions. High flow ventilators in clinics are used to manage patients with conditions such as COPD, asthma, and sleep apnea, providing them with the necessary respiratory support to maintain their quality of life. Clinics often use portable high flow ventilators, as they allow patients to receive treatment while maintaining their mobility and independence. Ambulatory Surgical Centers (ASCs) are another important area of usage for high flow ventilators. These centers provide surgical care on an outpatient basis, and high flow ventilators are used to support patients during and after surgery. In ASCs, high flow ventilators are used to manage patients with respiratory conditions that may be exacerbated by anesthesia or surgical procedures, ensuring their safety and comfort during the perioperative period. The use of high flow ventilators in ASCs helps to reduce the risk of postoperative complications and improve patient outcomes. Overall, the usage of high flow ventilators in hospitals, clinics, and ambulatory surgical centers is essential in providing effective respiratory support to patients with a wide range of conditions. As the demand for high flow ventilators continues to grow, these healthcare facilities are expected to play a crucial role in the Global High Flow Ventilator Market, driving innovation and improving patient care.

Global High Flow Ventilator Market Outlook:

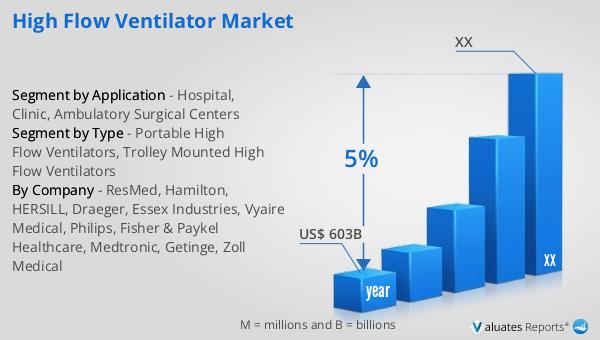

Our research indicates that the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, increasing healthcare expenditure, and the rising prevalence of chronic diseases. The medical device industry encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices, all of which play a crucial role in modern healthcare. As the demand for innovative and effective medical devices continues to rise, manufacturers are focusing on developing new technologies and improving existing products to meet the evolving needs of healthcare providers and patients. The growth of the medical device market is also supported by the increasing adoption of digital health solutions, which are transforming the way healthcare is delivered and managed. As healthcare systems worldwide continue to prioritize patient care and outcomes, the global medical device market is expected to witness sustained growth and innovation, providing new opportunities for manufacturers and healthcare providers alike.

| Report Metric | Details |

| Report Name | High Flow Ventilator Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | HERSILL, Draeger, Essex Industries, Vyaire Medical, Philips, Fisher & Paykel Healthcare, Medtronic, Getinge, Zoll Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |