What is Semiconductor Ceramic Components - Global Market?

Semiconductor ceramic components are crucial elements in the global market, playing a vital role in the functioning of various electronic devices. These components are made from ceramic materials that possess excellent electrical insulation properties, high thermal stability, and resistance to wear and corrosion. They are used in a wide range of applications, including microelectronics, telecommunications, automotive, and consumer electronics. The global market for semiconductor ceramic components is driven by the increasing demand for advanced electronic devices and the growing adoption of semiconductors in various industries. As technology continues to evolve, the need for more efficient and reliable semiconductor components is expected to rise, further propelling the market growth. The market is characterized by continuous innovation and development, with manufacturers focusing on enhancing the performance and durability of ceramic components to meet the ever-changing demands of the industry. The integration of these components in modern electronic devices not only improves their functionality but also extends their lifespan, making them indispensable in the current technological landscape.

Photosensitive, Heat Sensitive, Pressure Sensitive, Moisture Sensitive, Gas Sensitive in the Semiconductor Ceramic Components - Global Market:

In the realm of semiconductor ceramic components, sensitivity to various environmental factors such as light, heat, pressure, moisture, and gas plays a significant role in their functionality and application. Photosensitive components are designed to respond to light exposure, making them essential in devices like cameras and optical sensors. These components can detect changes in light intensity and convert them into electrical signals, enabling precise control and measurement in various applications. Heat-sensitive components, on the other hand, are crucial in temperature regulation and monitoring systems. They can detect temperature changes and adjust the performance of electronic devices accordingly, ensuring optimal operation and preventing overheating. Pressure-sensitive components are used in applications where pressure measurement is critical, such as in automotive and industrial systems. They can detect changes in pressure and provide accurate readings, which are essential for maintaining safety and efficiency. Moisture-sensitive components are vital in environments where humidity levels need to be monitored and controlled. These components can detect moisture levels and trigger appropriate responses to prevent damage to electronic devices. Lastly, gas-sensitive components are used in applications where gas detection is necessary, such as in environmental monitoring and safety systems. They can detect the presence of specific gases and provide real-time data for analysis and decision-making. The integration of these sensitive components in semiconductor ceramic components enhances their functionality and expands their application range, making them indispensable in various industries.

300mm Wafer, 200mm Wafer, Others in the Semiconductor Ceramic Components - Global Market:

Semiconductor ceramic components are extensively used in the production of wafers, which are the foundational elements in semiconductor manufacturing. In the context of 300mm wafers, these components play a crucial role in ensuring the precision and efficiency of the manufacturing process. The larger size of 300mm wafers allows for the production of more chips per wafer, which increases productivity and reduces costs. Semiconductor ceramic components are used in various stages of the wafer manufacturing process, including deposition, etching, and polishing. They provide the necessary insulation and stability required for the precise fabrication of semiconductor devices. In the case of 200mm wafers, semiconductor ceramic components are equally important. Although smaller than 300mm wafers, 200mm wafers are still widely used in the industry due to their cost-effectiveness and compatibility with existing manufacturing equipment. The use of ceramic components in 200mm wafer production ensures the reliability and performance of the final semiconductor devices. Additionally, semiconductor ceramic components are used in other wafer sizes and types, catering to specific applications and requirements. These components provide the necessary support and functionality for the efficient production of semiconductor devices, regardless of the wafer size. The versatility and reliability of semiconductor ceramic components make them indispensable in the global market, supporting the continuous advancement of semiconductor technology.

Semiconductor Ceramic Components - Global Market Outlook:

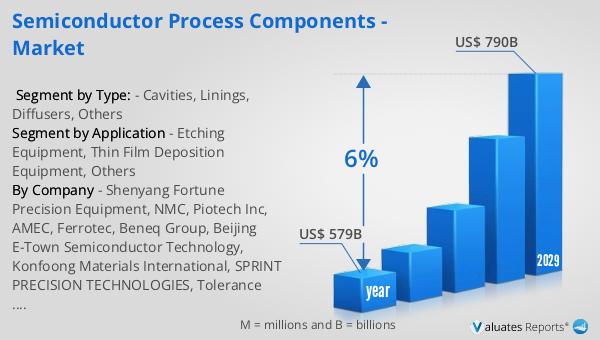

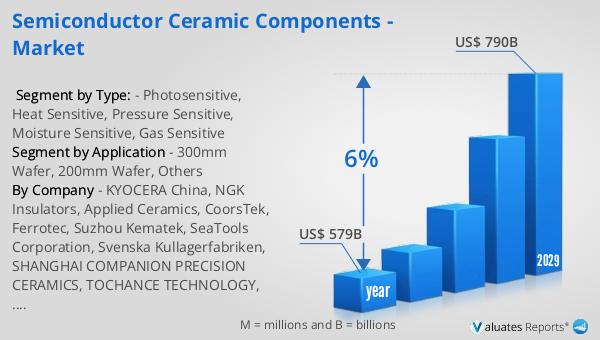

The global semiconductor market was valued at approximately $579 billion in 2022, and it is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for semiconductors across various industries, including consumer electronics, automotive, telecommunications, and healthcare. The rapid advancement of technology and the growing adoption of digital devices are key factors contributing to the expansion of the semiconductor market. As industries continue to embrace digital transformation, the need for more efficient and powerful semiconductor components is expected to rise. This demand is further fueled by the increasing integration of artificial intelligence, the Internet of Things (IoT), and 5G technology, which require advanced semiconductor solutions. The market's growth is also supported by continuous innovation and development in semiconductor technology, with manufacturers focusing on enhancing the performance and efficiency of their products. As a result, the global semiconductor market is poised for significant growth in the coming years, driven by the increasing demand for advanced electronic devices and the continuous evolution of technology.

| Report Metric | Details |

| Report Name | Semiconductor Ceramic Components - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | KYOCERA China, NGK Insulators, Applied Ceramics, CoorsTek, Ferrotec, Suzhou Kematek, SeaTools Corporation, Svenska Kullagerfabriken, SHANGHAI COMPANION PRECISION CERAMICS, TOCHANCE TECHNOLOGY, XIDE Technology, JAPAN FINE CERAMICS, COREWAY OPTECH, Hangzhou Semiconductor Wafer, Electronics Notes, Maruwa, NGK Spark Plug, SCHOTT Electronic Packaging, NEO Tech, AdTech Ceramics, Ametek, ECRI Microelectronics, SoarTech, Semiconductor Enclosures Inc(SEI) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |