What is Gellan Gum Powder - Global Market?

Gellan gum powder is a versatile ingredient that has gained significant attention in the global market due to its unique properties and wide range of applications. Derived from the bacterium Sphingomonas elodea, gellan gum is a polysaccharide that acts as a gelling agent, stabilizer, and thickener. It is particularly valued for its ability to form gels at low concentrations, making it an efficient and cost-effective option for manufacturers. The global market for gellan gum powder is driven by its increasing use in various industries, including food and beverages, pharmaceuticals, and personal care products. In the food industry, it is used to improve texture and stability in products like dairy alternatives, desserts, and beverages. Its compatibility with other ingredients and its ability to withstand different temperatures and pH levels make it a preferred choice for formulators. Additionally, the growing demand for plant-based and clean-label products has further fueled the market, as gellan gum is considered a natural and vegan-friendly ingredient. As consumers continue to seek healthier and more sustainable options, the demand for gellan gum powder is expected to rise, making it a key player in the global market landscape.

Low Acyl Gellan Gum, High Acyl Gellan Gum in the Gellan Gum Powder - Global Market:

Low acyl gellan gum and high acyl gellan gum are two distinct types of gellan gum that cater to different needs in the global market. Low acyl gellan gum is known for forming firm, brittle gels, which makes it ideal for applications requiring a strong gel structure. This type of gellan gum is often used in products like jelly desserts, confectionery, and certain dairy products where a firm texture is desired. Its ability to create clear gels also makes it suitable for applications where transparency is important, such as in certain beverages and desserts. On the other hand, high acyl gellan gum forms soft, elastic gels, which are more suitable for applications that require a flexible and resilient texture. This type of gellan gum is often used in products like sauces, dressings, and dairy alternatives where a smooth and creamy texture is preferred. The choice between low acyl and high acyl gellan gum depends on the specific requirements of the product being developed, including the desired texture, clarity, and stability. Both types of gellan gum offer excellent stability across a range of temperatures and pH levels, making them versatile ingredients for formulators. The global market for gellan gum powder is influenced by the growing demand for both low acyl and high acyl gellan gum, as manufacturers seek to create innovative products that meet consumer preferences for texture and quality. As the food and beverage industry continues to evolve, the demand for gellan gum is expected to grow, driven by its ability to enhance product appeal and functionality. Additionally, the increasing focus on clean-label and plant-based products has further boosted the market for gellan gum, as it is considered a natural and vegan-friendly ingredient. The versatility and functionality of both low acyl and high acyl gellan gum make them valuable components in the development of a wide range of products, from traditional foods to modern plant-based alternatives. As consumer preferences continue to shift towards healthier and more sustainable options, the demand for gellan gum is likely to increase, making it an essential ingredient in the global market.

Food Additives Industry, Daily-Chemical Industry, Pharmaceutical Industry, Others in the Gellan Gum Powder - Global Market:

Gellan gum powder finds extensive usage across various industries, each benefiting from its unique properties. In the food additives industry, gellan gum is prized for its ability to improve the texture and stability of a wide range of products. It is commonly used in dairy alternatives, desserts, and beverages to provide a desirable mouthfeel and consistency. Its ability to form gels at low concentrations makes it an efficient choice for manufacturers looking to enhance product quality without significantly increasing costs. In the daily-chemical industry, gellan gum is used as a stabilizer and thickener in products like shampoos, lotions, and creams. Its compatibility with other ingredients and its ability to maintain stability across different temperatures and pH levels make it a valuable component in personal care formulations. In the pharmaceutical industry, gellan gum is used as a controlled-release agent in drug delivery systems. Its ability to form gels and its biocompatibility make it suitable for use in oral and topical formulations, where it can help control the release of active ingredients over time. Additionally, gellan gum is used in other industries, such as agriculture and biotechnology, where its gelling properties are utilized in applications like seed coatings and microbial culture media. The versatility and functionality of gellan gum powder make it a valuable ingredient across these diverse industries, driving its demand in the global market. As consumer preferences continue to evolve, the demand for gellan gum is expected to grow, fueled by its ability to enhance product quality and meet the needs of various applications.

Gellan Gum Powder - Global Market Outlook:

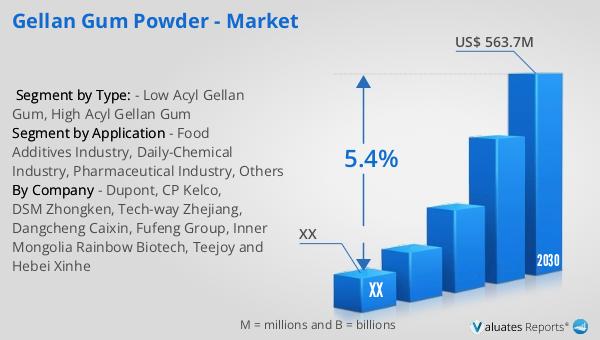

The global market for gellan gum powder was valued at approximately $392.1 million in 2023, with projections indicating a growth to around $563.7 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.4% during the forecast period from 2024 to 2030. The North American market, a significant contributor to the global landscape, was also valued at a substantial figure in 2023, with expectations of reaching even higher values by 2030. The growth in this region is anticipated to follow a similar upward trajectory, driven by increasing demand across various industries. The market's expansion is attributed to the rising popularity of gellan gum as a versatile ingredient in food, pharmaceuticals, and personal care products. Its ability to improve texture, stability, and overall product quality has made it a preferred choice for manufacturers seeking to meet consumer demands for healthier and more sustainable options. As the market continues to evolve, gellan gum powder is poised to play a crucial role in shaping the future of product development across multiple sectors.

| Report Metric | Details |

| Report Name | Gellan Gum Powder - Market |

| Forecasted market size in 2030 | US$ 563.7 million |

| CAGR | 5.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Dupont, CP Kelco, DSM Zhongken, Tech-way Zhejiang, Dangcheng Caixin, Fufeng Group, Inner Mongolia Rainbow Biotech, Teejoy and Hebei Xinhe |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |