What is Simply Lancet - Global Market?

Simply Lancet - Global Market is a comprehensive term that refers to the worldwide market for lancets, which are small medical devices used to obtain blood samples. These devices are crucial in various medical settings, particularly for individuals who need to monitor their blood glucose levels regularly, such as those with diabetes. The global market for lancets is driven by the increasing prevalence of diabetes and other chronic conditions that require regular blood testing. Additionally, advancements in lancet technology, such as the development of less painful and more efficient devices, have contributed to the market's growth. The market is characterized by a wide range of products, including different sizes and types of lancets, catering to diverse consumer needs. Companies in this market are continually innovating to improve the comfort and ease of use of their products, which is a significant factor in consumer choice. The Simply Lancet - Global Market is also influenced by regulatory standards and healthcare policies across different regions, which can impact the availability and adoption of these devices. Overall, the market is poised for growth as healthcare needs evolve and more people require regular blood testing for various health conditions.

1.5 mm, 1.8 mm, 2.0 mm, 2.2 mm, Others in the Simply Lancet - Global Market:

The Simply Lancet - Global Market offers a variety of lancet sizes, each designed to meet specific needs and preferences. The 1.5 mm lancet is typically used for individuals who require minimal penetration for blood sampling, making it ideal for those with delicate skin or for pediatric use. This size is often preferred in settings where the goal is to minimize discomfort while still obtaining an adequate blood sample. The 1.8 mm lancet provides slightly deeper penetration, which can be beneficial for individuals who have thicker skin or require a larger blood sample. This size strikes a balance between comfort and efficacy, making it a popular choice in both clinical and home settings. The 2.0 mm lancet is designed for more robust blood sampling needs, often used in situations where a larger volume of blood is necessary for testing. This size is commonly used in hospitals and clinics where precise and reliable blood samples are crucial for accurate diagnostics. The 2.2 mm lancet offers the deepest penetration among the standard sizes, suitable for individuals with particularly tough skin or when a substantial blood sample is required. This size is less commonly used but is essential in specific medical scenarios where other sizes may not suffice. Beyond these standard sizes, the market also includes other lancet sizes and types, catering to niche needs and preferences. These may include adjustable lancets, which allow users to customize the depth of penetration, or specialty lancets designed for specific medical conditions or testing requirements. The diversity in lancet sizes and types reflects the market's commitment to addressing the varied needs of healthcare providers and patients, ensuring that everyone can find a suitable option for their blood sampling needs. As the Simply Lancet - Global Market continues to evolve, the focus remains on enhancing user comfort, improving sampling efficiency, and expanding the range of available options to meet the growing demand for personalized healthcare solutions.

Hospital, Clinic, Others in the Simply Lancet - Global Market:

The usage of Simply Lancet - Global Market products spans various healthcare settings, including hospitals, clinics, and other medical facilities. In hospitals, lancets are an essential tool for obtaining blood samples from patients for a wide range of diagnostic tests. They are used in various departments, including emergency rooms, intensive care units, and outpatient services, where quick and reliable blood sampling is crucial for patient care. The use of lancets in hospitals is often characterized by a need for high-quality, sterile devices that can provide accurate results with minimal discomfort to patients. In clinics, lancets are commonly used for routine blood tests, such as glucose monitoring for diabetic patients. Clinics often serve as the primary point of care for many individuals, making the availability of reliable lancets essential for effective patient management. The use of lancets in clinics is typically focused on ease of use and patient comfort, as many patients may need to perform self-testing regularly. Beyond hospitals and clinics, lancets are also used in other settings, such as home healthcare and community health programs. In these contexts, the emphasis is often on user-friendly designs that enable individuals to perform blood tests independently. This is particularly important for patients with chronic conditions who need to monitor their health regularly. The Simply Lancet - Global Market also caters to specialized medical fields, such as veterinary medicine, where lancets are used for blood sampling in animals. The versatility of lancets makes them a valuable tool in various healthcare applications, supporting the ongoing need for accurate and efficient blood testing across different settings. As healthcare continues to evolve, the demand for high-quality lancets is expected to grow, driven by the increasing prevalence of chronic diseases and the need for regular health monitoring.

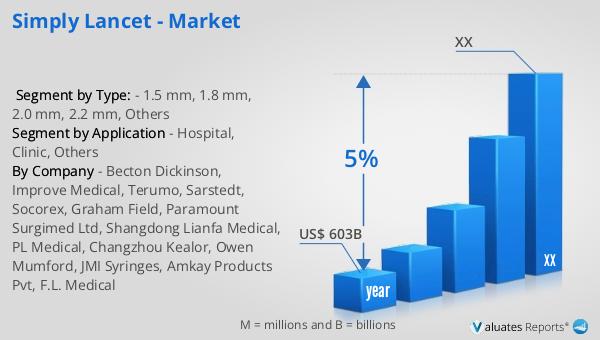

Simply Lancet - Global Market Outlook:

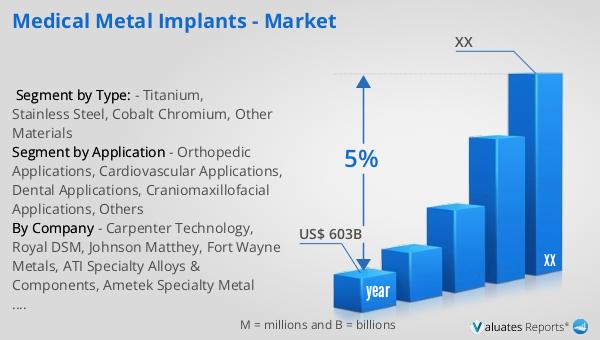

The global market for medical devices, including lancets, is experiencing significant growth. According to our research, the market is valued at approximately US$ 603 billion in 2023. This substantial market size reflects the critical role that medical devices play in modern healthcare, providing essential tools for diagnosis, treatment, and monitoring of various health conditions. The market is projected to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including technological advancements, increasing healthcare needs, and the rising prevalence of chronic diseases that require regular monitoring and management. The demand for innovative and efficient medical devices is also fueled by an aging global population, which requires more frequent medical interventions and monitoring. Additionally, the expansion of healthcare infrastructure in emerging markets is contributing to the increased adoption of medical devices, including lancets. As healthcare systems worldwide strive to improve patient outcomes and reduce costs, the role of medical devices in achieving these goals becomes increasingly important. The Simply Lancet - Global Market is a key component of this broader medical device landscape, providing essential tools for blood sampling and monitoring that support effective healthcare delivery. As the market continues to grow, companies are focusing on developing new and improved lancet designs that enhance user comfort and sampling efficiency, meeting the evolving needs of healthcare providers and patients alike.

| Report Metric | Details |

| Report Name | Simply Lancet - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Becton Dickinson, Improve Medical, Terumo, Sarstedt, Socorex, Graham Field, Paramount Surgimed Ltd, Shangdong Lianfa Medical, PL Medical, Changzhou Kealor, Owen Mumford, JMI Syringes, Amkay Products Pvt, F.L. Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |