What is In-vitro Fertilization (IVF) Incubators - Global Market?

In-vitro Fertilization (IVF) incubators are specialized devices used in the process of assisted reproduction. These incubators provide a controlled environment that mimics the conditions inside a human body, crucial for the development of embryos outside the body. The global market for IVF incubators is driven by the increasing prevalence of infertility, advancements in medical technology, and the growing acceptance of assisted reproductive technologies. These incubators are essential in maintaining the optimal temperature, humidity, and gas concentrations necessary for embryo culture. As more couples seek IVF treatments, the demand for reliable and efficient incubators continues to rise. The market is characterized by a variety of incubator types, each designed to meet specific needs within fertility clinics and research institutions. With ongoing research and development, the capabilities of these incubators are continually improving, offering better outcomes for patients undergoing IVF procedures. The global market for IVF incubators is poised for significant growth, reflecting the increasing reliance on these technologies in reproductive medicine.

Benchtop/Tabletop Incubators, Floor-Based Incubators in the In-vitro Fertilization (IVF) Incubators - Global Market:

Benchtop or tabletop incubators and floor-based incubators are two primary types of IVF incubators available in the global market, each serving distinct purposes and offering unique advantages. Benchtop incubators are compact and designed to fit on laboratory benches or tables, making them ideal for smaller clinics or laboratories with limited space. These incubators are often used for individual patient samples, allowing for personalized care and reducing the risk of cross-contamination. They are equipped with advanced features such as precise temperature control, CO2 and O2 regulation, and humidity management, ensuring optimal conditions for embryo development. The portability and ease of use of benchtop incubators make them a popular choice for clinics that require flexibility and efficiency in their operations. On the other hand, floor-based incubators are larger and designed to accommodate a higher volume of samples, making them suitable for larger fertility clinics or research institutions with a high throughput of IVF procedures. These incubators offer robust features, including advanced monitoring systems, alarm functions, and data logging capabilities, providing comprehensive oversight of the incubation process. Floor-based incubators are often equipped with multiple chambers, allowing for the simultaneous incubation of numerous samples, which is beneficial for clinics handling a large number of patients. The choice between benchtop and floor-based incubators depends on various factors, including the size of the clinic, the volume of IVF procedures, and the specific needs of the patients. Both types of incubators play a crucial role in the IVF process, ensuring that embryos are cultured in an environment that closely mimics the natural conditions of the human body. As the demand for IVF treatments continues to grow, the market for both benchtop and floor-based incubators is expected to expand, driven by technological advancements and the increasing need for efficient and reliable reproductive technologies. The global market for IVF incubators is characterized by innovation and competition, with manufacturers continually striving to enhance the performance and capabilities of their products. This dynamic market environment encourages the development of incubators that offer improved outcomes for patients, greater ease of use for clinicians, and enhanced efficiency for fertility clinics. As a result, both benchtop and floor-based incubators are essential components of the IVF process, contributing to the success of assisted reproductive technologies worldwide.

Fertility Clinics, Hospitals, Surgical Centers, Clinical Research Institutes, Others in the In-vitro Fertilization (IVF) Incubators - Global Market:

In-vitro Fertilization (IVF) incubators are utilized across various settings, including fertility clinics, hospitals, surgical centers, clinical research institutes, and other related facilities. In fertility clinics, these incubators are indispensable tools that support the entire IVF process. They provide a stable and controlled environment for the culture and development of embryos, ensuring that they are maintained under optimal conditions until they are ready for transfer to the uterus. The precision and reliability of IVF incubators are critical in fertility clinics, where the success of IVF treatments depends heavily on the quality of embryo culture. Hospitals also use IVF incubators, particularly those with specialized reproductive medicine departments. In these settings, incubators are part of a broader range of assisted reproductive technologies offered to patients. Hospitals may handle more complex cases, requiring advanced incubator features to support diverse patient needs. Surgical centers that offer IVF services also rely on these incubators to maintain the viability of embryos during the treatment process. The use of IVF incubators in surgical centers is often integrated with other medical procedures, necessitating high levels of precision and control. Clinical research institutes utilize IVF incubators for research and development purposes, exploring new techniques and technologies to improve IVF outcomes. In these settings, incubators are used to study embryo development, test new culture media, and evaluate the effects of various environmental conditions on embryo viability. The insights gained from research conducted in clinical research institutes contribute to the advancement of IVF technologies and practices. Other facilities, such as academic institutions and private laboratories, may also use IVF incubators for educational and experimental purposes. These incubators support a wide range of activities, from training future reproductive specialists to conducting experiments that enhance our understanding of human reproduction. Across all these settings, the use of IVF incubators is driven by the need to provide a controlled and supportive environment for embryo development, ensuring the highest possible success rates for IVF treatments. As the demand for assisted reproductive technologies continues to grow, the role of IVF incubators in these various settings becomes increasingly important, highlighting their significance in the global market.

In-vitro Fertilization (IVF) Incubators - Global Market Outlook:

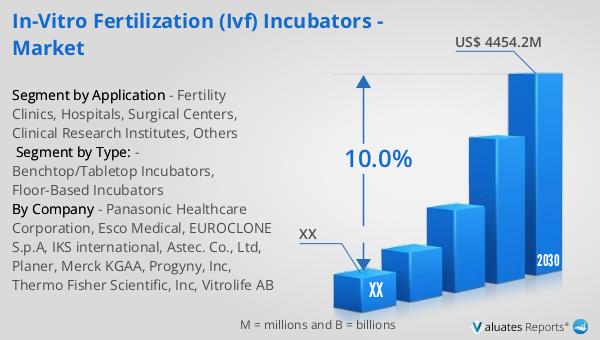

The global market for In-vitro Fertilization (IVF) incubators was valued at approximately $2,219.7 million in 2023. It is projected to grow significantly, reaching an estimated $4,454.2 million by 2030, with a compound annual growth rate (CAGR) of 10.0% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for IVF treatments and the technological advancements in incubator design and functionality. In North America, the market for IVF incubators was valued at a substantial amount in 2023, with expectations of continued growth through 2030. The CAGR for this region during the forecast period is indicative of the robust demand for IVF technologies and the presence of advanced healthcare infrastructure. The North American market is characterized by a high adoption rate of innovative reproductive technologies, driven by factors such as rising infertility rates and the availability of skilled healthcare professionals. As the global and regional markets for IVF incubators expand, manufacturers are focusing on developing products that offer enhanced performance, reliability, and ease of use, catering to the diverse needs of fertility clinics, hospitals, and research institutions. This dynamic market environment underscores the importance of IVF incubators in the field of reproductive medicine, highlighting their critical role in supporting successful IVF outcomes.

| Report Metric | Details |

| Report Name | In-vitro Fertilization (IVF) Incubators - Market |

| Forecasted market size in 2030 | US$ 4454.2 million |

| CAGR | 10.0% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Panasonic Healthcare Corporation, Esco Medical, EUROCLONE S.p.A, IKS international, Astec. Co., Ltd, Planer, Merck KGAA, Progyny, Inc, Thermo Fisher Scientific, Inc, Vitrolife AB |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |