What is N-BK7 Optical Component - Global Market?

N-BK7 is a type of optical glass that is widely used in the production of various optical components due to its excellent transmission and mechanical properties. It is a borosilicate crown glass with a high level of purity and homogeneity, making it ideal for precision optics. The global market for N-BK7 optical components is driven by its extensive applications in industries such as medical, aerospace, defense, and semiconductor manufacturing. These components are essential in creating lenses, mirrors, prisms, windows, and filters, which are integral to various optical systems. The demand for N-BK7 optical components is increasing as industries continue to advance technologically, requiring more sophisticated optical solutions. The market is characterized by a growing need for high-quality optical components that can withstand different environmental conditions while maintaining performance. As a result, manufacturers are focusing on innovation and improving the quality of N-BK7 optical components to meet the evolving needs of various sectors. The global market is expected to grow steadily, driven by technological advancements and the increasing adoption of optical technologies across different industries.

Lenses, Mirros, Optical Prisms, Windows, Filters, Others in the N-BK7 Optical Component - Global Market:

N-BK7 optical components are essential in various optical applications due to their versatility and excellent optical properties. Lenses made from N-BK7 are widely used in imaging systems, including cameras, microscopes, and telescopes, due to their high transmission and low absorption of light. These lenses are crucial in focusing and directing light, enabling clear and precise imaging. Mirrors made from N-BK7 are used in laser systems, optical instruments, and scientific research. They provide high reflectivity and durability, making them suitable for applications requiring precise light manipulation. Optical prisms made from N-BK7 are used to bend, reflect, and disperse light in various optical systems. They are essential in applications such as spectroscopy, telecommunications, and laser systems, where precise light control is necessary. Windows made from N-BK7 are used to protect sensitive optical components while allowing light to pass through with minimal distortion. They are used in various applications, including laser systems, scientific instruments, and industrial equipment. Filters made from N-BK7 are used to selectively transmit or block specific wavelengths of light. They are used in applications such as photography, scientific research, and telecommunications, where precise control of light is required. Other N-BK7 optical components include beam splitters, waveplates, and polarizers, which are used in various optical systems to manipulate light in specific ways. The versatility and excellent optical properties of N-BK7 make it a preferred choice for a wide range of optical applications.

Medical & Life Sciences, Aerospace and Defense, Semiconductor Manufacturing, Others in the N-BK7 Optical Component - Global Market:

N-BK7 optical components are widely used in various industries due to their excellent optical properties and versatility. In the medical and life sciences sector, N-BK7 components are used in imaging systems, diagnostic equipment, and laser systems. They enable precise imaging and light manipulation, which are crucial for accurate diagnosis and treatment. In the aerospace and defense industry, N-BK7 components are used in optical systems for navigation, targeting, and surveillance. They provide high performance and durability, essential for applications in harsh environments. In semiconductor manufacturing, N-BK7 components are used in lithography systems, inspection equipment, and laser systems. They enable precise light control, which is crucial for the production of high-quality semiconductor devices. Other industries that use N-BK7 optical components include telecommunications, scientific research, and industrial manufacturing. In telecommunications, N-BK7 components are used in optical communication systems to enable high-speed data transmission. In scientific research, they are used in various optical instruments for precise light manipulation and measurement. In industrial manufacturing, N-BK7 components are used in laser systems and optical sensors for precise measurement and control. The versatility and excellent optical properties of N-BK7 make it a preferred choice for a wide range of applications across different industries.

N-BK7 Optical Component - Global Market Outlook:

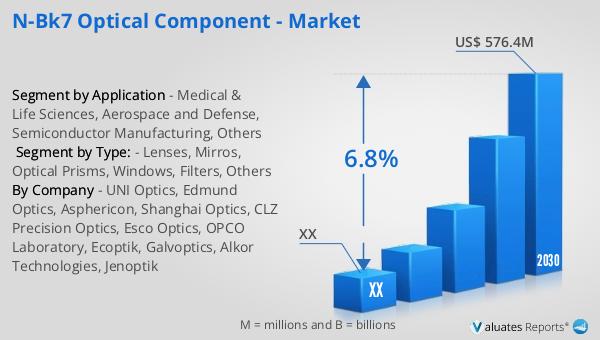

The global market for N-BK7 optical components was valued at approximately $357 million in 2023. It is projected to grow to a revised size of $576.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.8% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for high-quality optical components across various industries, including medical, aerospace, defense, and semiconductor manufacturing. The North American market for N-BK7 optical components was also valued significantly in 2023, with expectations of substantial growth by 2030. The market's expansion is attributed to technological advancements and the increasing adoption of optical technologies in various applications. As industries continue to advance and require more sophisticated optical solutions, the demand for N-BK7 optical components is expected to rise. Manufacturers are focusing on innovation and improving the quality of these components to meet the evolving needs of different sectors. The global market is poised for steady growth, driven by the increasing adoption of optical technologies and the need for high-quality optical components.

| Report Metric | Details |

| Report Name | N-BK7 Optical Component - Market |

| Forecasted market size in 2030 | US$ 576.4 million |

| CAGR | 6.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | UNI Optics, Edmund Optics, Asphericon, Shanghai Optics, CLZ Precision Optics, Esco Optics, OPCO Laboratory, Ecoptik, Galvoptics, Alkor Technologies, Jenoptik |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |