What is Global Coating Service for Semiconductor and FPD (Flat Panel Display) Market?

The global Coating Service for Semiconductor and FPD (Flat Panel Display) market is a specialized sector that focuses on providing advanced coating solutions for semiconductor devices and flat panel displays. These coatings are essential for enhancing the performance, durability, and efficiency of electronic components. The market encompasses a wide range of services, including the application of protective coatings, anti-reflective coatings, and conductive coatings, among others. These coatings are crucial in protecting sensitive electronic components from environmental factors such as moisture, dust, and chemical exposure, thereby extending their lifespan and improving their functionality. The demand for these services is driven by the rapid advancements in technology and the increasing need for high-performance electronic devices in various industries, including consumer electronics, automotive, healthcare, and telecommunications. As the semiconductor and flat panel display industries continue to evolve, the need for specialized coating services is expected to grow, making this market a vital component of the global electronics manufacturing ecosystem.

in the Global Coating Service for Semiconductor and FPD (Flat Panel Display) Market:

In the Global Coating Service for Semiconductor and FPD (Flat Panel Display) market, various types of coatings are utilized by different customers based on their specific needs and applications. One of the most common types is the protective coating, which is used to shield semiconductor devices and flat panel displays from physical damage and environmental contaminants. These coatings are typically made from materials such as silicon dioxide, silicon nitride, and various polymers, which provide excellent barrier properties and mechanical strength. Another important type is the anti-reflective coating, which is designed to reduce glare and improve the visibility of flat panel displays. These coatings are often made from multi-layered thin films that can effectively minimize light reflection and enhance the display's contrast and color accuracy. Conductive coatings are also widely used in this market, particularly in applications where electrical conductivity is required. These coatings are typically made from materials such as indium tin oxide (ITO) and other conductive polymers, which can provide excellent electrical performance while maintaining transparency. Additionally, there are specialty coatings such as hydrophobic and oleophobic coatings, which are used to repel water and oil, respectively. These coatings are particularly useful in applications where the devices are exposed to harsh environmental conditions or require easy cleaning. Customers in the semiconductor and flat panel display industries often choose these coatings based on factors such as the specific requirements of their applications, the desired performance characteristics, and the cost-effectiveness of the coating solutions. As a result, the market for coating services is highly diverse and dynamic, with a wide range of options available to meet the varying needs of different customers.

Semiconductor Equipment Parts, FPD (Flat Panel Display) in the Global Coating Service for Semiconductor and FPD (Flat Panel Display) Market:

The usage of Global Coating Service for Semiconductor and FPD (Flat Panel Display) Market in semiconductor equipment parts and flat panel displays is extensive and multifaceted. In the semiconductor industry, coating services are essential for the fabrication and protection of semiconductor equipment parts. These parts, which include wafers, photomasks, and various other components, require precise and reliable coatings to ensure their optimal performance and longevity. Protective coatings are applied to prevent contamination and damage during the manufacturing process, while anti-reflective coatings are used to enhance the efficiency of photolithography processes by reducing unwanted reflections and improving light transmission. Conductive coatings are also crucial in semiconductor equipment, as they enable the creation of electrical pathways and connections within the devices. In the flat panel display industry, coating services play a vital role in enhancing the visual quality and durability of displays. Anti-reflective coatings are commonly used to improve the readability and color accuracy of displays by minimizing glare and reflections. Additionally, protective coatings are applied to safeguard the delicate display surfaces from scratches, impacts, and environmental factors. Hydrophobic and oleophobic coatings are also used to make the display surfaces resistant to water and oil, making them easier to clean and maintain. The application of these coatings requires advanced technologies and precise control to achieve the desired performance characteristics. As a result, coating service providers in this market invest heavily in research and development to continuously improve their coating solutions and meet the evolving demands of the semiconductor and flat panel display industries. Overall, the usage of coating services in these areas is critical for ensuring the high performance, reliability, and longevity of semiconductor equipment parts and flat panel displays.

Global Coating Service for Semiconductor and FPD (Flat Panel Display) Market Outlook:

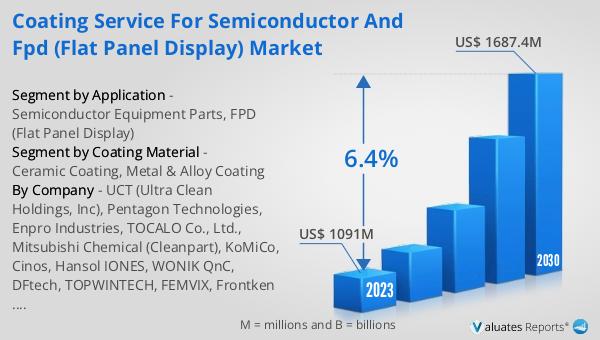

The global Coating Service for Semiconductor and FPD (Flat Panel Display) market was valued at US$ 1091 million in 2023 and is anticipated to reach US$ 1687.4 million by 2030, witnessing a CAGR of 6.4% during the forecast period from 2024 to 2030. The market is characterized by a high level of competition, with the top three players holding a combined market share of about 45%, while the top ten players account for over 70% of the market. This competitive landscape is driven by the continuous advancements in coating technologies and the increasing demand for high-performance electronic devices. The leading companies in this market are focused on expanding their product portfolios, enhancing their technological capabilities, and strengthening their global presence to maintain their competitive edge. As the semiconductor and flat panel display industries continue to grow, the demand for specialized coating services is expected to rise, further driving the market's growth. The market outlook indicates a positive trend, with significant opportunities for innovation and development in the coming years.

| Report Metric | Details |

| Report Name | Coating Service for Semiconductor and FPD (Flat Panel Display) Market |

| Accounted market size in 2023 | US$ 1091 million |

| Forecasted market size in 2030 | US$ 1687.4 million |

| CAGR | 6.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Coating Material |

|

| Segment by Application |

|

| By Region |

|

| By Company | UCT (Ultra Clean Holdings, Inc), Pentagon Technologies, Enpro Industries, TOCALO Co., Ltd., Mitsubishi Chemical (Cleanpart), KoMiCo, Cinos, Hansol IONES, WONIK QnC, DFtech, TOPWINTECH, FEMVIX, Frontken Corporation Berhad, Value Engineering Co., Ltd, KERTZ HIGH TECH, Hung Jie Technology Corporation, Oerlikon Balzers, Beneq, APS Materials, Inc., SilcoTek, Alumiplate, YMC Co., Ltd., ASSET Solutions, Inc., Jiangsu Kaiweitesi Semiconductor Technology Co., Ltd., HCUT Co., Ltd, Ferrotec (Anhui) Technology Development Co., Ltd, Shanghai Companion, Wuhu Tongchao Precision Machinery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |