What is Global Linear Inductive Encoder Market?

The Global Linear Inductive Encoder Market is a specialized segment within the broader field of position sensing and measurement technology. Linear inductive encoders are devices that use electromagnetic induction to measure linear displacement or position. These encoders are highly valued for their precision, reliability, and robustness in various industrial applications. They are commonly used in environments where traditional optical encoders might fail due to dust, oil, or other contaminants. The market for these devices is driven by the increasing demand for automation and precision in manufacturing processes, as well as advancements in technology that have made these encoders more affordable and versatile. Industries such as automotive, aerospace, electronics, and healthcare are significant consumers of linear inductive encoders, leveraging their capabilities to enhance the accuracy and efficiency of their operations. As industries continue to evolve and seek more sophisticated solutions for position sensing, the global linear inductive encoder market is expected to grow, offering new opportunities for innovation and application.

Sensing Increment, Absolute Increment in the Global Linear Inductive Encoder Market:

Sensing increment and absolute increment are two critical concepts in the Global Linear Inductive Encoder Market. Sensing increment, also known as incremental encoding, involves measuring the change in position from a known reference point. This type of encoding is particularly useful in applications where relative movement needs to be tracked, such as in motor control systems or conveyor belts. Incremental encoders generate a series of pulses as the position changes, and these pulses are counted to determine the distance moved. The primary advantage of incremental encoders is their simplicity and cost-effectiveness, making them suitable for a wide range of industrial applications. On the other hand, absolute increment, or absolute encoding, provides a unique position value for each point along the measurement range. This means that even if the system loses power, the exact position can be determined immediately upon restart without needing to return to a reference point. Absolute encoders are essential in applications where precision and reliability are paramount, such as in robotics, medical devices, and aerospace systems. They offer higher accuracy and are less susceptible to errors caused by signal loss or interference. The choice between incremental and absolute encoders depends on the specific requirements of the application, including factors like accuracy, cost, and environmental conditions. Both types of encoders play a vital role in the global linear inductive encoder market, catering to diverse needs across various industries. As technology advances, the capabilities of both incremental and absolute encoders continue to improve, offering enhanced performance and new possibilities for their use.

Motor, Mobile Device, Others in the Global Linear Inductive Encoder Market:

The Global Linear Inductive Encoder Market finds extensive usage in various areas, including motors, mobile devices, and other applications. In the realm of motors, linear inductive encoders are crucial for precise control and positioning. They are used in servo motors, stepper motors, and other types of electric motors to ensure accurate movement and positioning. This is particularly important in industries like manufacturing, where precision is key to maintaining product quality and operational efficiency. Linear inductive encoders help in monitoring and controlling the motor's position, speed, and direction, enabling automated systems to function smoothly and accurately. In mobile devices, linear inductive encoders are used to enhance the functionality and user experience. For instance, they can be found in smartphones, tablets, and other portable electronics, where they help in detecting and measuring linear movements. This can be used for features like touch sensitivity, gesture recognition, and other interactive functionalities. The compact size and high precision of linear inductive encoders make them ideal for integration into mobile devices, where space and accuracy are critical. Beyond motors and mobile devices, linear inductive encoders are used in a wide range of other applications. These include medical devices, where they are used for precise positioning in imaging equipment, surgical robots, and other healthcare technologies. In the aerospace industry, they are used for navigation and control systems, ensuring the accurate positioning of aircraft components. Additionally, they are employed in the automotive industry for applications like throttle control, braking systems, and suspension systems. The versatility and reliability of linear inductive encoders make them suitable for various demanding environments, contributing to their widespread adoption across different sectors.

Global Linear Inductive Encoder Market Outlook:

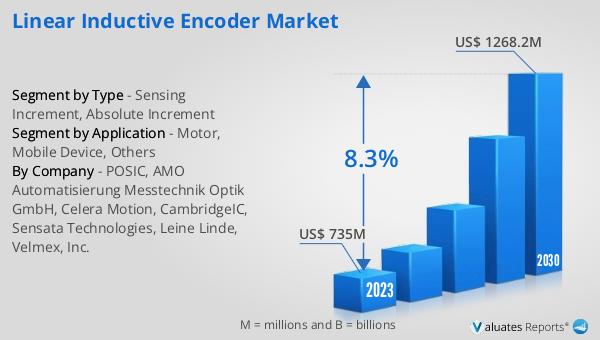

The global Linear Inductive Encoder market, valued at US$ 735 million in 2023, is projected to grow significantly, reaching an estimated US$ 1268.2 million by 2030. This growth represents a compound annual growth rate (CAGR) of 8.3% over the forecast period from 2024 to 2030. The increasing demand for precision and automation in various industries is a key driver of this market expansion. Linear inductive encoders are becoming more popular due to their ability to provide accurate and reliable position measurements in challenging environments. Industries such as automotive, aerospace, electronics, and healthcare are increasingly adopting these encoders to enhance their operational efficiency and product quality. The advancements in technology have also made linear inductive encoders more affordable and versatile, further boosting their adoption. As industries continue to evolve and seek more sophisticated solutions for position sensing, the global linear inductive encoder market is expected to witness substantial growth, offering new opportunities for innovation and application.

| Report Metric | Details |

| Report Name | Linear Inductive Encoder Market |

| Accounted market size in 2023 | US$ 735 million |

| Forecasted market size in 2030 | US$ 1268.2 million |

| CAGR | 8.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | POSIC, AMO Automatisierung Messtechnik Optik GmbH, Celera Motion, CambridgeIC, Sensata Technologies, Leine Linde, Velmex, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |