What is Global Portable UAV Countermeasure Equipment Market?

The Global Portable UAV Countermeasure Equipment Market refers to the industry focused on developing and supplying portable devices designed to detect, intercept, and neutralize unmanned aerial vehicles (UAVs), commonly known as drones. These countermeasure systems are essential for addressing the growing concerns related to unauthorized or malicious drone activities. They are used in various sectors, including military, commercial, and civilian applications, to ensure security and privacy. The market encompasses a wide range of technologies, such as radio frequency jammers, GPS spoofers, and drone-catching nets, all aimed at mitigating the risks posed by rogue drones. As drone technology advances and becomes more accessible, the demand for effective countermeasure equipment is expected to rise, driving innovation and growth in this market. The Global Portable UAV Countermeasure Equipment Market is characterized by rapid technological advancements and increasing investments from both government and private sectors, aiming to enhance the capabilities and effectiveness of these systems.

To Monitor, To Intercept in the Global Portable UAV Countermeasure Equipment Market:

To monitor and intercept UAVs, the Global Portable UAV Countermeasure Equipment Market employs a variety of sophisticated technologies and strategies. Monitoring involves the detection and tracking of UAVs using radar systems, radio frequency (RF) detectors, and optical sensors. These systems can identify the presence of a drone, determine its location, and track its movements in real-time. Radar systems are particularly effective in detecting drones at long ranges, while RF detectors can identify the communication signals between the drone and its operator. Optical sensors, including cameras and infrared detectors, provide visual confirmation and can be used to track drones in various environmental conditions. Once a UAV is detected, interception strategies come into play. These strategies aim to neutralize the threat posed by the drone, either by disabling it or capturing it. One common method is the use of RF jammers, which disrupt the communication link between the drone and its operator, causing the drone to lose control and either land or return to its point of origin. GPS spoofers are another effective tool, misleading the drone's navigation system and causing it to deviate from its intended path. In some cases, physical interception methods are employed, such as deploying nets to capture the drone or using trained birds of prey to intercept it mid-flight. The choice of interception method depends on the specific threat scenario and the operational environment. For instance, in urban areas, non-destructive methods like RF jamming and GPS spoofing are preferred to avoid collateral damage. In contrast, in open or rural areas, physical interception methods may be more feasible. The integration of artificial intelligence (AI) and machine learning (ML) technologies is also enhancing the capabilities of UAV countermeasure systems. AI and ML algorithms can analyze vast amounts of data from various sensors to identify patterns and predict the behavior of drones, enabling more effective monitoring and interception. Additionally, these technologies can automate the decision-making process, allowing for faster and more accurate responses to drone threats. The development of portable UAV countermeasure equipment is driven by the need for flexibility and mobility. Portable systems can be easily transported and deployed in various locations, making them ideal for use in dynamic and rapidly changing environments. These systems are often designed to be user-friendly, with intuitive interfaces and automated functions that reduce the need for specialized training. The market for portable UAV countermeasure equipment is also influenced by regulatory and legal considerations. Governments and regulatory bodies are establishing guidelines and frameworks for the use of countermeasure systems to ensure they are used responsibly and do not interfere with legitimate drone operations. Compliance with these regulations is essential for manufacturers and operators of UAV countermeasure equipment. In summary, the Global Portable UAV Countermeasure Equipment Market is focused on developing advanced technologies and strategies for monitoring and intercepting UAVs. These systems employ a combination of radar, RF detectors, optical sensors, RF jammers, GPS spoofers, and physical interception methods to detect, track, and neutralize drone threats. The integration of AI and ML technologies is further enhancing the effectiveness of these systems, while the need for portability and regulatory compliance drives innovation in the market.

Military Use, Commercial, Civilian Use in the Global Portable UAV Countermeasure Equipment Market:

The usage of Global Portable UAV Countermeasure Equipment spans across military, commercial, and civilian sectors, each with distinct requirements and applications. In the military domain, these systems are crucial for protecting sensitive installations, personnel, and assets from hostile drones. Military forces use portable UAV countermeasure equipment to safeguard bases, forward operating locations, and critical infrastructure from surveillance, reconnaissance, and potential attacks by enemy drones. These systems are also deployed during military operations to provide a protective shield against drone threats, ensuring the safety of troops and mission success. The ability to quickly deploy and relocate these portable systems makes them highly valuable in dynamic and unpredictable combat environments. In the commercial sector, the demand for UAV countermeasure equipment is driven by the need to protect critical infrastructure, such as airports, power plants, and communication networks, from unauthorized drone activities. Airports, in particular, face significant risks from drones that can disrupt flight operations and pose safety hazards to aircraft. Portable countermeasure systems enable airport authorities to detect and neutralize drones that enter restricted airspace, ensuring the safety and efficiency of flight operations. Similarly, power plants and communication networks use these systems to prevent drones from causing disruptions or damage to their operations. The commercial sector also includes industries such as oil and gas, where drones can be used for industrial espionage or sabotage. Portable UAV countermeasure equipment provides a flexible and effective solution for protecting these critical assets. In the civilian sector, the use of UAV countermeasure equipment is growing as drones become more prevalent in everyday life. Public safety agencies, such as police and fire departments, use these systems to manage drone activities during emergencies, public events, and large gatherings. For example, during a major public event, portable countermeasure systems can be deployed to monitor and intercept unauthorized drones that may pose security risks or disrupt the event. Additionally, these systems are used to protect privacy and prevent unauthorized surveillance by drones in residential areas. Homeowners and private security firms can use portable UAV countermeasure equipment to detect and neutralize drones that intrude on private property, ensuring privacy and security. The versatility and portability of these systems make them suitable for a wide range of civilian applications, from protecting individual homes to securing large public spaces. The integration of advanced technologies, such as AI and ML, further enhances the effectiveness of UAV countermeasure systems in all sectors. These technologies enable more accurate detection, tracking, and interception of drones, reducing the risk of false alarms and improving response times. The development of user-friendly interfaces and automated functions also makes these systems accessible to a broader range of users, from highly trained military personnel to civilian homeowners. In conclusion, the Global Portable UAV Countermeasure Equipment Market serves a diverse range of applications across military, commercial, and civilian sectors. In the military domain, these systems protect sensitive installations and support operational security. In the commercial sector, they safeguard critical infrastructure and prevent industrial espionage. In the civilian sector, they enhance public safety, protect privacy, and secure private property. The portability, flexibility, and advanced technological capabilities of these systems make them indispensable tools for addressing the growing challenges posed by unauthorized and malicious drone activities.

Global Portable UAV Countermeasure Equipment Market Outlook:

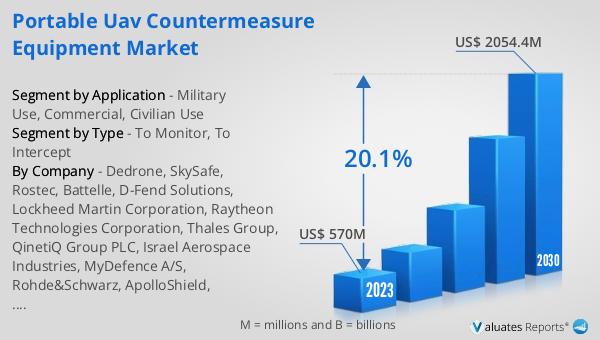

The global Portable UAV Countermeasure Equipment market was valued at $570 million in 2023 and is projected to reach $2,054.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 20.1% during the forecast period from 2024 to 2030. This significant growth underscores the increasing demand for effective solutions to counter the rising threats posed by unauthorized and malicious drone activities. The market's expansion is driven by advancements in technology, increased investments from both government and private sectors, and the growing awareness of the need for robust UAV countermeasure systems. As drone technology continues to evolve and become more accessible, the potential risks associated with their misuse also rise, necessitating the development of more sophisticated and portable countermeasure equipment. The projected growth of the market highlights the critical importance of these systems in ensuring security and privacy across various sectors, including military, commercial, and civilian applications. The substantial increase in market value over the forecast period indicates a strong and sustained demand for innovative and effective UAV countermeasure solutions.

| Report Metric | Details |

| Report Name | Portable UAV Countermeasure Equipment Market |

| Accounted market size in 2023 | US$ 570 million |

| Forecasted market size in 2030 | US$ 2054.4 million |

| CAGR | 20.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dedrone, SkySafe, Rostec, Battelle, D-Fend Solutions, Lockheed Martin Corporation, Raytheon Technologies Corporation, Thales Group, QinetiQ Group PLC, Israel Aerospace Industries, MyDefence A/S, Rohde&Schwarz, ApolloShield, DroneShield Limited |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |