What is Global Restaurant Service Robot Market?

The Global Restaurant Service Robot Market refers to the industry focused on the development, production, and deployment of robots designed specifically for use in restaurants. These robots are engineered to perform a variety of tasks that traditionally require human labor, such as serving food, delivering meals, and even preparing dishes. The market encompasses a wide range of robotic technologies, from simple automated systems to highly sophisticated machines equipped with artificial intelligence and machine learning capabilities. The primary goal of these robots is to enhance efficiency, reduce operational costs, and improve customer service in the restaurant industry. As technology advances and labor costs rise, the adoption of service robots in restaurants is expected to grow, making this market a significant area of interest for both technology developers and restaurant operators. The market is driven by factors such as the increasing demand for automation, the need for improved customer experiences, and the ongoing labor shortages in the hospitality sector.

Meal Delivery Service Robot, Food Making Robot in the Global Restaurant Service Robot Market:

Meal Delivery Service Robots and Food Making Robots are two prominent categories within the Global Restaurant Service Robot Market. Meal Delivery Service Robots are designed to transport food from the kitchen to the dining area, ensuring timely and efficient service. These robots are equipped with sensors and navigation systems that allow them to move autonomously within the restaurant, avoiding obstacles and delivering meals directly to customers' tables. They can be programmed to follow specific routes and schedules, reducing the need for human waitstaff and minimizing the risk of errors. These robots are particularly useful in large restaurants or those with complex layouts, where human servers might struggle to maintain efficiency. On the other hand, Food Making Robots are designed to assist in the kitchen, performing tasks such as chopping vegetables, cooking dishes, and even assembling meals. These robots can work alongside human chefs, taking on repetitive or labor-intensive tasks and allowing the chefs to focus on more creative aspects of cooking. Food Making Robots are equipped with advanced sensors and algorithms that enable them to follow recipes accurately and consistently, ensuring high-quality food production. They can also be programmed to handle multiple tasks simultaneously, increasing the overall productivity of the kitchen. The integration of these robots into restaurant operations can lead to significant cost savings, as they reduce the need for human labor and minimize food waste. Additionally, they can help maintain high standards of hygiene and food safety, as they are less prone to contamination compared to human workers. The adoption of Meal Delivery Service Robots and Food Making Robots is expected to grow as restaurants seek to improve efficiency, reduce costs, and enhance the dining experience for their customers.

Restaurant, Kitchen in the Global Restaurant Service Robot Market:

The usage of Global Restaurant Service Robots in restaurants and kitchens is transforming the way these establishments operate. In the dining area, service robots are being used to greet customers, take orders, and deliver food to tables. These robots are equipped with touchscreens or voice recognition systems that allow customers to place their orders directly, reducing the need for human waitstaff. They can also provide information about the menu, answer customer queries, and even process payments. This not only enhances the customer experience but also allows restaurants to operate with fewer staff, reducing labor costs. In the kitchen, robots are being used to perform a variety of tasks, from food preparation to cooking and plating. These robots can chop vegetables, mix ingredients, cook dishes, and even assemble complex meals with precision and consistency. They are equipped with advanced sensors and algorithms that enable them to follow recipes accurately, ensuring that each dish is prepared to the same high standard every time. This not only improves the quality of the food but also increases the efficiency of the kitchen, as robots can work continuously without the need for breaks. Additionally, robots can help maintain high standards of hygiene and food safety, as they are less prone to contamination compared to human workers. The integration of robots into restaurant operations can also lead to significant cost savings, as they reduce the need for human labor and minimize food waste. Overall, the usage of Global Restaurant Service Robots in restaurants and kitchens is revolutionizing the industry, making it more efficient, cost-effective, and customer-friendly.

Global Restaurant Service Robot Market Outlook:

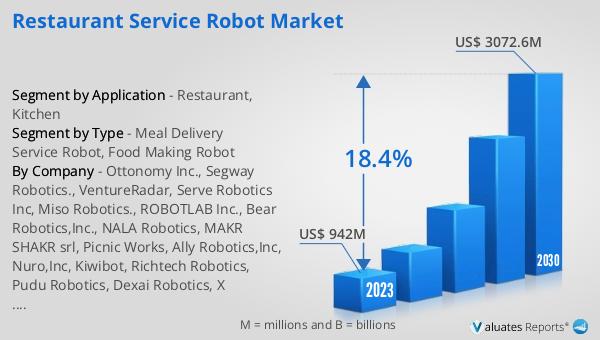

The global Restaurant Service Robot market was valued at US$ 942 million in 2023 and is anticipated to reach US$ 3072.6 million by 2030, witnessing a CAGR of 18.4% during the forecast period 2024-2030. This significant growth reflects the increasing adoption of automation and robotics in the restaurant industry. As labor costs continue to rise and the demand for efficient, high-quality service grows, more and more restaurants are turning to robotic solutions to meet these challenges. The market's rapid expansion is also driven by advancements in technology, which have made robots more affordable, reliable, and capable of performing a wider range of tasks. From meal delivery and food preparation to customer service and order processing, robots are becoming an integral part of restaurant operations. This trend is expected to continue as restaurants seek to improve efficiency, reduce costs, and enhance the overall dining experience for their customers. The projected growth of the Restaurant Service Robot market underscores the transformative impact of robotics on the hospitality industry and highlights the potential for further innovation and development in this field.

| Report Metric | Details |

| Report Name | Restaurant Service Robot Market |

| Accounted market size in 2023 | US$ 942 million |

| Forecasted market size in 2030 | US$ 3072.6 million |

| CAGR | 18.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Ottonomy Inc., Segway Robotics., VentureRadar, Serve Robotics Inc, Miso Robotics., ROBOTLAB Inc., Bear Robotics,Inc., NALA Robotics, MAKR SHAKR srl, Picnic Works, Ally Robotics,Inc, Nuro,Inc, Kiwibot, Richtech Robotics, Pudu Robotics, Dexai Robotics, X Robotics,Inc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |