What is Global Battery Test Instrument Market?

The Global Battery Test Instrument Market refers to the industry focused on the development, production, and distribution of devices used to test and analyze the performance, capacity, and efficiency of batteries. These instruments are crucial for ensuring the reliability and longevity of batteries used in various applications, from consumer electronics to industrial machinery. The market encompasses a wide range of products, including portable and stationary battery testers, which are used by manufacturers, service providers, and end-users to assess battery health, diagnose issues, and ensure optimal performance. The demand for battery test instruments is driven by the increasing adoption of battery-powered devices and the growing emphasis on renewable energy sources, which rely heavily on efficient energy storage solutions. As technology advances and the need for sustainable energy solutions grows, the Global Battery Test Instrument Market is expected to expand, offering innovative tools and technologies to meet the evolving needs of various industries.

Portable Battery Test Instrument, Stationary Battery Test Instrument in the Global Battery Test Instrument Market:

Portable Battery Test Instruments are compact, handheld devices designed for on-the-go testing and analysis of batteries. These instruments are widely used in field applications where mobility and convenience are essential. They are equipped with features such as voltage measurement, current measurement, and impedance testing, allowing users to quickly assess the health and performance of batteries in real-time. Portable battery testers are commonly used by technicians and engineers in industries such as automotive, telecommunications, and consumer electronics, where they need to diagnose battery issues and ensure optimal performance without the need for bulky equipment. These devices are particularly valuable in situations where batteries are installed in remote or hard-to-reach locations, as they enable efficient testing without the need for extensive disassembly or transportation of the battery. On the other hand, Stationary Battery Test Instruments are larger, more sophisticated systems designed for comprehensive testing and analysis of batteries in controlled environments. These instruments are typically used in laboratory settings, manufacturing facilities, and large-scale energy storage systems where detailed and accurate battery testing is required. Stationary battery testers offer advanced features such as automated testing, data logging, and integration with other testing equipment, providing a thorough assessment of battery performance, capacity, and lifespan. They are essential for battery manufacturers and researchers who need to conduct rigorous testing to ensure the quality and reliability of their products. Additionally, stationary battery testers are used in industries such as renewable energy and grid storage, where large-scale battery systems are deployed to store and manage energy generated from sources like solar and wind power. The Global Battery Test Instrument Market is characterized by a diverse range of products catering to different testing needs and applications. Portable battery testers offer the advantage of mobility and ease of use, making them ideal for field applications and quick diagnostics. They are designed to be user-friendly, with intuitive interfaces and robust construction to withstand the rigors of fieldwork. These instruments are often used in maintenance and service operations, where technicians need to quickly identify and address battery issues to minimize downtime and ensure the smooth operation of equipment and systems. In contrast, stationary battery testers provide a higher level of precision and automation, making them suitable for more detailed and comprehensive testing. These instruments are equipped with advanced features such as programmable test sequences, high-resolution measurement capabilities, and extensive data analysis tools. They are used in research and development, quality control, and production testing, where accurate and reliable battery performance data is critical. Stationary battery testers are also used in large-scale energy storage systems, where they help monitor and manage the performance of battery arrays to ensure efficient and reliable energy storage and distribution. Overall, the Global Battery Test Instrument Market offers a wide range of solutions to meet the diverse needs of various industries. Whether it's the portability and convenience of handheld testers or the precision and automation of stationary systems, these instruments play a crucial role in ensuring the performance, reliability, and longevity of batteries in a wide range of applications. As the demand for battery-powered devices and renewable energy solutions continues to grow, the market for battery test instruments is expected to expand, offering innovative and advanced tools to meet the evolving needs of the industry.

Automobile, Electronic, Telecom, Other in the Global Battery Test Instrument Market:

The usage of Global Battery Test Instruments spans across several key areas, including the automobile, electronic, telecom, and other sectors. In the automobile industry, battery test instruments are essential for ensuring the performance and reliability of batteries used in electric vehicles (EVs) and hybrid vehicles. These instruments help manufacturers and service providers assess battery health, diagnose issues, and optimize battery performance, which is crucial for the safety and efficiency of modern vehicles. With the increasing adoption of EVs and the growing emphasis on sustainable transportation, the demand for battery test instruments in the automotive sector is on the rise. These instruments are used throughout the battery lifecycle, from development and production to maintenance and end-of-life recycling, ensuring that batteries meet the stringent performance and safety standards required in the automotive industry. In the electronics sector, battery test instruments are used to evaluate the performance of batteries used in a wide range of consumer and industrial electronic devices. From smartphones and laptops to medical devices and industrial equipment, batteries are a critical component that determines the reliability and longevity of these products. Battery test instruments help manufacturers and service providers ensure that batteries meet the required performance specifications and provide reliable power to electronic devices. These instruments are used in research and development, quality control, and after-sales service, helping to identify and address battery issues and improve the overall performance and user experience of electronic products. The telecom industry also relies heavily on battery test instruments to ensure the reliability and performance of batteries used in telecommunications equipment and infrastructure. Batteries are a critical component of telecom networks, providing backup power to ensure uninterrupted service during power outages and other emergencies. Battery test instruments help telecom operators monitor and maintain the health of their battery systems, ensuring that they can provide reliable backup power when needed. These instruments are used in the installation, maintenance, and monitoring of battery systems in telecom networks, helping to prevent service disruptions and ensure the smooth operation of communication services. In addition to the automobile, electronics, and telecom sectors, battery test instruments are used in a variety of other industries and applications. For example, in the renewable energy sector, battery test instruments are used to evaluate the performance of batteries used in energy storage systems, which are essential for storing and managing energy generated from renewable sources like solar and wind power. These instruments help ensure that energy storage systems operate efficiently and reliably, supporting the integration of renewable energy into the grid and reducing reliance on fossil fuels. Battery test instruments are also used in industrial applications, where they help monitor and maintain the performance of batteries used in machinery, equipment, and backup power systems. Overall, the usage of Global Battery Test Instruments is widespread and diverse, spanning multiple industries and applications. These instruments play a crucial role in ensuring the performance, reliability, and safety of batteries, which are a critical component of modern technology and infrastructure. As the demand for battery-powered devices and renewable energy solutions continues to grow, the importance of battery test instruments in ensuring the optimal performance and longevity of batteries is expected to increase, driving further innovation and development in the Global Battery Test Instrument Market.

Global Battery Test Instrument Market Outlook:

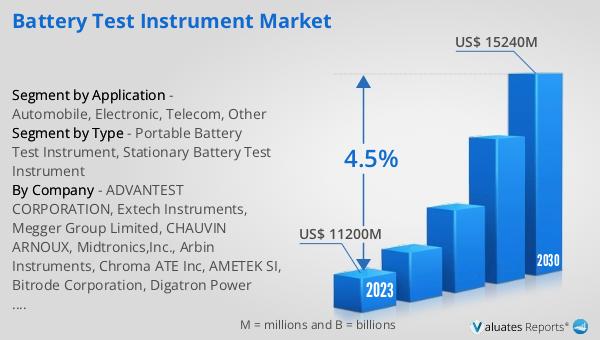

The global Battery Test Instrument market was valued at US$ 11,200 million in 2023 and is projected to reach US$ 15,240 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2030. This growth indicates a steady increase in the demand for battery test instruments, driven by the rising adoption of battery-powered devices and the growing emphasis on renewable energy solutions. The market's expansion is fueled by advancements in battery technology, the increasing use of electric vehicles, and the need for efficient energy storage systems. As industries continue to rely on batteries for various applications, the demand for reliable and accurate battery test instruments is expected to grow, supporting the development and deployment of innovative battery technologies. The projected growth of the market underscores the importance of battery test instruments in ensuring the performance, reliability, and safety of batteries across different sectors, including automotive, electronics, telecommunications, and renewable energy. With the ongoing advancements in battery technology and the increasing focus on sustainability, the Global Battery Test Instrument Market is poised for significant growth in the coming years.

| Report Metric | Details |

| Report Name | Battery Test Instrument Market |

| Accounted market size in 2023 | US$ 11200 million |

| Forecasted market size in 2030 | US$ 15240 million |

| CAGR | 4.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | ADVANTEST CORPORATION, Extech Instruments, Megger Group Limited, CHAUVIN ARNOUX, Midtronics,Inc., Arbin Instruments, Chroma ATE Inc, AMETEK SI, Bitrode Corporation, Digatron Power Electronics, EA Elektro-Automatik, HORIBA FuelCon GmbH, HEiNZINGER, Keysight |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |