What is Global Intelligent Spray System (Intelligent Spraying System) Market?

The Global Intelligent Spray System (Intelligent Spraying System) Market refers to the market for advanced spraying technologies that utilize sensors, data analytics, and automation to optimize the application of liquids such as pesticides, herbicides, and fertilizers. These systems are designed to enhance precision, reduce waste, and minimize environmental impact by ensuring that the right amount of liquid is applied to the right place at the right time. Intelligent spraying systems can be used in various sectors, including agriculture, forestry, and other industries that require precise liquid application. By leveraging technologies such as GPS, Lidar, and ultrasonic sensors, these systems can detect the presence of plants, pests, or other targets and adjust the spraying pattern accordingly. This not only improves the efficiency of the spraying process but also helps in reducing the overall usage of chemicals, thereby promoting sustainable practices. The market for these systems is growing as more industries recognize the benefits of precision spraying and seek to adopt these advanced technologies to improve their operations.

Targeted Spraying System Based on Ultrasonic Sensor, Smart Sprinkler System Based on Lidar Sensor in the Global Intelligent Spray System (Intelligent Spraying System) Market:

Targeted Spraying Systems based on ultrasonic sensors and Smart Sprinkler Systems based on Lidar sensors are two prominent technologies within the Global Intelligent Spray System Market. Targeted Spraying Systems utilize ultrasonic sensors to detect the presence of plants or pests and adjust the spraying mechanism accordingly. These sensors emit ultrasonic waves that bounce back upon hitting an object, allowing the system to determine the distance and presence of the target. This technology ensures that chemicals are only sprayed where needed, reducing waste and minimizing environmental impact. On the other hand, Smart Sprinkler Systems based on Lidar sensors use light detection and ranging technology to create detailed maps of the area to be sprayed. Lidar sensors emit laser pulses that reflect off surfaces, providing precise measurements of distance and shape. This data is used to create a 3D map of the terrain, enabling the system to adjust the spraying pattern for optimal coverage. Both technologies offer significant advantages in terms of precision and efficiency. By accurately targeting the application of liquids, these systems help in reducing the overall usage of chemicals, thereby promoting sustainable practices. Additionally, they can be integrated with data analytics and machine learning algorithms to further enhance their performance. For instance, historical data on pest infestations or plant growth can be used to predict future spraying needs, allowing for proactive management. These intelligent systems are also equipped with GPS technology, enabling them to navigate large areas with ease and ensure uniform coverage. The integration of these advanced technologies into spraying systems represents a significant advancement in the field of precision agriculture and other industries that require precise liquid application. As the demand for sustainable and efficient spraying solutions continues to grow, the adoption of these intelligent systems is expected to increase, driving further innovation and development in the market.

Agriculture, Forestry, Other in the Global Intelligent Spray System (Intelligent Spraying System) Market:

The usage of Global Intelligent Spray Systems in agriculture, forestry, and other areas is transforming traditional practices by introducing precision and efficiency. In agriculture, these systems are used to apply pesticides, herbicides, and fertilizers with high accuracy. By detecting the presence of crops and pests, intelligent spraying systems ensure that chemicals are only applied where needed, reducing waste and minimizing environmental impact. This not only helps in conserving resources but also promotes sustainable farming practices. Farmers can benefit from reduced input costs and improved crop yields, as the precise application of chemicals ensures that plants receive the right amount of nutrients and protection. In forestry, intelligent spraying systems are used to manage pests and diseases that threaten trees. By accurately targeting the application of chemicals, these systems help in preserving the health of forests while minimizing the impact on the surrounding environment. This is particularly important in maintaining biodiversity and protecting natural habitats. Other industries, such as landscaping and urban green spaces, also benefit from intelligent spraying systems. These systems can be used to maintain parks, gardens, and other public spaces by ensuring that plants receive the necessary care without overuse of chemicals. The ability to precisely control the application of liquids makes these systems ideal for managing large areas efficiently. Additionally, intelligent spraying systems can be used in industrial applications, such as cleaning and coating processes, where precise liquid application is crucial. The integration of advanced technologies, such as GPS, Lidar, and ultrasonic sensors, into these systems enhances their performance and reliability. By leveraging data analytics and machine learning, intelligent spraying systems can continuously improve their accuracy and efficiency, making them a valuable tool in various sectors. As the demand for sustainable and efficient solutions continues to grow, the adoption of intelligent spraying systems is expected to increase, driving further innovation and development in the market.

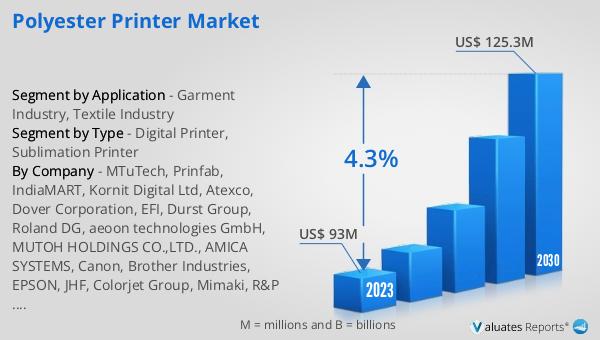

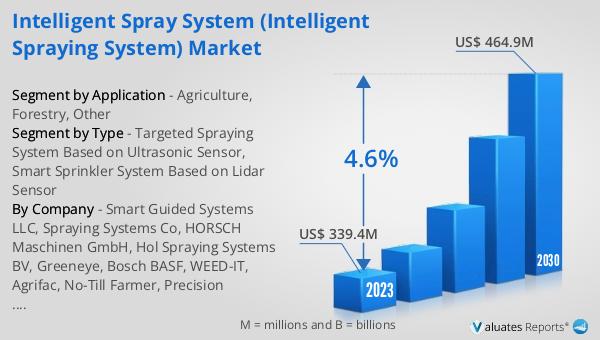

Global Intelligent Spray System (Intelligent Spraying System) Market Outlook:

The global Intelligent Spray System market, valued at US$ 339.4 million in 2023, is projected to reach US$ 464.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.6% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for precision spraying solutions across various industries, including agriculture, forestry, and other sectors. The adoption of advanced technologies, such as GPS, Lidar, and ultrasonic sensors, is enhancing the performance and efficiency of intelligent spraying systems, making them a preferred choice for many applications. These systems offer significant advantages in terms of reducing waste, minimizing environmental impact, and promoting sustainable practices. As industries continue to recognize the benefits of precision spraying, the market for intelligent spray systems is expected to expand further. The integration of data analytics and machine learning into these systems is also contributing to their growing popularity, as it allows for continuous improvement in accuracy and efficiency. With the increasing focus on sustainability and resource conservation, the demand for intelligent spraying systems is likely to continue rising, driving further innovation and development in the market.

| Report Metric | Details |

| Report Name | Intelligent Spray System (Intelligent Spraying System) Market |

| Accounted market size in 2023 | US$ 339.4 million |

| Forecasted market size in 2030 | US$ 464.9 million |

| CAGR | 4.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Smart Guided Systems LLC, Spraying Systems Co, HORSCH Maschinen GmbH, Hol Spraying Systems BV, Greeneye, Bosch BASF, WEED-IT, Agrifac, No-Till Farmer, Precision Planting,LLC, TeeJet Technologies, Mitra, Croplands, Australian Diversified Engineering Pty Ltd, LahakX, Fruit Growers News, Hexagon AB, Trimble Inc, Ibex Automation Ltd, AOM-Systems, AGCO Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |