What is Global Thermoelectric Cooler (TEC) Modules Market?

The Global Thermoelectric Cooler (TEC) Modules Market is a rapidly evolving sector that focuses on the development and distribution of thermoelectric cooling modules. These modules are semiconductor-based devices that use the Peltier effect to create a heat flux between the junction of two different types of materials. They are primarily used for precise temperature control and cooling applications across various industries. The market is driven by the increasing demand for energy-efficient cooling solutions and the growing adoption of TEC modules in consumer electronics, automotive, medical, and industrial applications. The versatility and efficiency of TEC modules make them an attractive option for a wide range of cooling needs, from small-scale electronic devices to large industrial systems. As technology advances, the market is expected to see significant growth, driven by innovations in materials and manufacturing processes that enhance the performance and reliability of these modules.

Single Stage Module, Multiple Modules, Others (Micromodules, Etc.) in the Global Thermoelectric Cooler (TEC) Modules Market:

Single Stage Modules, Multiple Modules, and Others (Micromodules, etc.) are the primary categories within the Global Thermoelectric Cooler (TEC) Modules Market. Single Stage Modules are the most common type and are widely used due to their simplicity and efficiency. These modules consist of a single thermoelectric couple and are ideal for applications requiring moderate cooling. They are often used in consumer electronics, where precise temperature control is essential for the optimal performance of devices such as smartphones, laptops, and gaming consoles. Single Stage Modules are also popular in medical devices, where maintaining a stable temperature is crucial for the accuracy and reliability of diagnostic equipment. Multiple Modules, on the other hand, consist of several thermoelectric couples connected in series or parallel to achieve higher cooling capacities. These modules are used in applications that require more substantial cooling power, such as industrial machinery, automotive climate control systems, and aerospace equipment. The ability to combine multiple modules allows for greater flexibility in designing cooling systems that can handle varying thermal loads. Other categories, such as Micromodules, are specialized versions of TEC modules designed for specific applications. Micromodules are typically smaller and more compact, making them suitable for use in miniature electronic devices and other applications where space is limited. These modules are often used in advanced communication systems, where precise temperature control is necessary to ensure the stability and performance of sensitive components. The versatility of TEC modules, combined with ongoing advancements in materials and manufacturing techniques, continues to drive innovation in this market. As a result, TEC modules are becoming increasingly efficient, reliable, and cost-effective, making them an attractive option for a wide range of cooling applications. The growing demand for energy-efficient and environmentally friendly cooling solutions further fuels the development and adoption of TEC modules across various industries. As the market continues to evolve, it is expected that new and improved TEC modules will emerge, offering even greater performance and efficiency for a diverse array of applications.

Consumer Electronics, Communication, Medical Experiment, Automobile, Industrial, Aerospace Defense, Others in the Global Thermoelectric Cooler (TEC) Modules Market:

The usage of Global Thermoelectric Cooler (TEC) Modules Market spans across several key areas, including Consumer Electronics, Communication, Medical Experiment, Automobile, Industrial, Aerospace Defense, and Others. In Consumer Electronics, TEC modules are used to manage the heat generated by devices such as smartphones, laptops, and gaming consoles. By maintaining optimal operating temperatures, these modules help enhance the performance and longevity of electronic components. In the Communication sector, TEC modules are crucial for cooling sensitive equipment such as laser diodes and photodetectors, ensuring stable operation and high signal quality. Medical Experiment applications benefit from TEC modules by providing precise temperature control for diagnostic devices, laboratory instruments, and medical storage units. This ensures the accuracy and reliability of medical tests and the safe storage of temperature-sensitive materials. In the Automobile industry, TEC modules are used in climate control systems to provide efficient cooling and heating solutions for vehicle interiors. They are also employed in battery thermal management systems to maintain optimal battery temperatures, enhancing the performance and lifespan of electric and hybrid vehicles. Industrial applications of TEC modules include cooling systems for machinery and equipment, where precise temperature control is essential for maintaining operational efficiency and preventing overheating. In the Aerospace Defense sector, TEC modules are used to cool electronic components in aircraft, satellites, and military equipment, ensuring reliable performance in extreme conditions. Other applications of TEC modules include cooling solutions for scientific instruments, data centers, and renewable energy systems. The versatility and efficiency of TEC modules make them an ideal choice for a wide range of cooling needs, driving their adoption across various industries. As technology continues to advance, the demand for TEC modules is expected to grow, further expanding their usage in new and existing applications.

Global Thermoelectric Cooler (TEC) Modules Market Outlook:

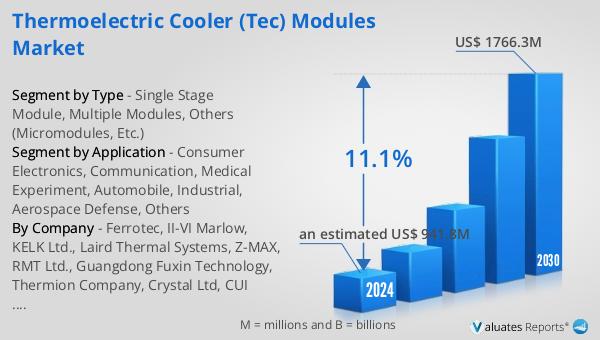

The global Thermoelectric Cooler (TEC) Modules market is anticipated to grow significantly, reaching an estimated value of US$ 1766.3 million by 2030, up from US$ 941.8 million in 2024, with a compound annual growth rate (CAGR) of 11.1% during the period from 2024 to 2030. The market is dominated by the top three companies, which collectively hold about 40% of the market share. Geographically, China leads the market with a share of approximately 28%, followed by North America and Japan, which hold shares of about 23% and 20%, respectively. In terms of product segmentation, single stage modules represent the largest segment, accounting for over 50% of the market share. This growth is driven by the increasing demand for energy-efficient cooling solutions and the widespread adoption of TEC modules across various industries. The versatility and efficiency of TEC modules make them an attractive option for a wide range of applications, from consumer electronics to industrial machinery. As technology continues to advance, the performance and reliability of TEC modules are expected to improve, further driving their adoption and market growth.

| Report Metric | Details |

| Report Name | Thermoelectric Cooler (TEC) Modules Market |

| Accounted market size in 2024 | an estimated US$ 941.8 million |

| Forecasted market size in 2030 | US$ 1766.3 million |

| CAGR | 11.1% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Ferrotec, II-VI Marlow, KELK Ltd., Laird Thermal Systems, Z-MAX, RMT Ltd., Guangdong Fuxin Technology, Thermion Company, Crystal Ltd, CUI Devices, Kryotherm Industries, Phononic, Merit Technology Group, TE Technology, KJLP electronics co., ltd, Thermonamic Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |