What is Multi-Station Cold Forging Machine - Global Market?

A Multi-Station Cold Forging Machine is a highly specialized piece of equipment used in the manufacturing industry to shape metal parts through a process called cold forging. Unlike traditional forging, which involves heating the metal, cold forging is done at room temperature, making it more energy-efficient and capable of producing parts with superior strength and precision. These machines are designed with multiple stations, each performing a different operation such as cutting, bending, or shaping the metal. This multi-station setup allows for the continuous and automated production of complex parts, significantly increasing efficiency and reducing labor costs. The global market for these machines is driven by their widespread application in various industries, including automotive, aerospace, and construction, where the demand for high-quality, durable metal components is ever-growing. As industries continue to seek ways to improve production efficiency and product quality, the adoption of Multi-Station Cold Forging Machines is expected to rise, making them a crucial component in modern manufacturing processes.

2-3 Station, 4-5 Station, 6-7 Station, Others in the Multi-Station Cold Forging Machine - Global Market:

Multi-Station Cold Forging Machines come in various configurations, typically categorized by the number of stations they have. The 2-3 station machines are generally used for simpler parts that require fewer steps to complete. These machines are ideal for small to medium-sized production runs and are often employed in industries where the demand for specific parts is not exceedingly high. They offer a good balance between cost and functionality, making them a popular choice for smaller manufacturers. On the other hand, 4-5 station machines are more versatile and can handle more complex parts that require multiple forming steps. These machines are commonly used in the automotive and machinery sectors, where the production of intricate components is essential. The additional stations allow for more detailed work, such as threading or additional shaping, which can be done in a single pass through the machine. This not only improves efficiency but also ensures higher precision and consistency in the final product. Moving up the complexity scale, 6-7 station machines are designed for the most intricate and high-volume production needs. These machines are often found in large-scale manufacturing operations where the demand for complex parts is continuous and high. The multiple stations allow for a wide range of operations to be performed in a single cycle, significantly reducing production time and labor costs. These machines are particularly valuable in the aerospace and defense industries, where the precision and reliability of each component are critical. Other configurations of Multi-Station Cold Forging Machines may include specialized setups tailored for specific applications or industries. These machines can be customized with additional features or stations to meet the unique requirements of a particular production process. For example, some machines may include additional quality control stations to ensure each part meets stringent industry standards. Overall, the versatility and efficiency of Multi-Station Cold Forging Machines make them an indispensable tool in modern manufacturing, capable of meeting the diverse needs of various industries.

Automotive, Aerospace and Defense, Machinery and Equipment, Construction, Others in the Multi-Station Cold Forging Machine - Global Market:

The usage of Multi-Station Cold Forging Machines spans across several key industries, each benefiting from the unique advantages these machines offer. In the automotive industry, these machines are used to produce a wide range of components, from engine parts to transmission gears. The high precision and strength of cold-forged parts make them ideal for automotive applications, where durability and performance are paramount. The ability to produce complex shapes in a single pass also reduces production time and costs, making these machines a valuable asset for automotive manufacturers. In the aerospace and defense sectors, the demand for high-quality, reliable components is even more critical. Multi-Station Cold Forging Machines are used to produce parts that must withstand extreme conditions and rigorous performance standards. The precision and consistency offered by these machines ensure that each component meets the stringent requirements of these industries. Additionally, the ability to automate the production process reduces the risk of human error, further enhancing the reliability of the final product. In the machinery and equipment industry, these machines are used to produce a variety of parts, from simple fasteners to complex machinery components. The versatility of Multi-Station Cold Forging Machines allows manufacturers to produce a wide range of parts with varying degrees of complexity, all with high precision and efficiency. This flexibility is particularly valuable in an industry where the demand for custom and specialized parts is high. The construction industry also benefits from the use of these machines, particularly in the production of structural components and fasteners. The strength and durability of cold-forged parts make them ideal for construction applications, where the integrity of each component is crucial. The ability to produce large quantities of parts quickly and efficiently also helps to meet the high demand for construction materials. Other industries, such as electronics and consumer goods, also utilize Multi-Station Cold Forging Machines for the production of various components. The precision and efficiency of these machines make them suitable for a wide range of applications, from small electronic connectors to larger consumer products. Overall, the versatility and efficiency of Multi-Station Cold Forging Machines make them a valuable asset in a wide range of industries, helping to improve production processes and product quality.

Multi-Station Cold Forging Machine - Global Market Outlook:

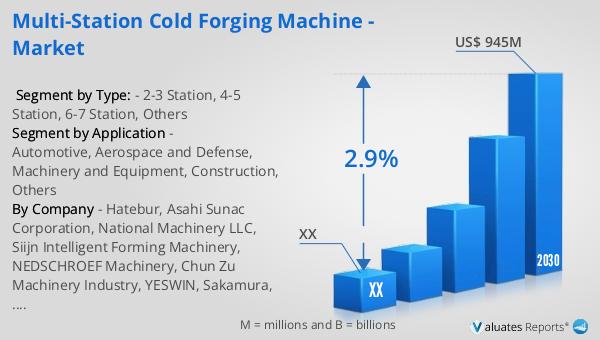

The global market for Multi-Station Cold Forging Machines was valued at approximately $789 million in 2023 and is projected to reach around $945 million by 2030, growing at a compound annual growth rate (CAGR) of 2.9% during the forecast period from 2024 to 2030. In North America, the market for these machines was valued at $ million in 2023 and is expected to reach $ million by 2030, also growing at a CAGR of % during the same forecast period. This growth is driven by the increasing demand for high-quality, durable metal components across various industries, including automotive, aerospace, and construction. The adoption of Multi-Station Cold Forging Machines is expected to rise as industries continue to seek ways to improve production efficiency and product quality. The versatility and efficiency of these machines make them an indispensable tool in modern manufacturing, capable of meeting the diverse needs of various industries. As the market continues to grow, manufacturers are likely to invest in advanced technologies and innovative solutions to enhance the capabilities of these machines, further driving their adoption and market growth.

| Report Metric | Details |

| Report Name | Multi-Station Cold Forging Machine - Market |

| Forecasted market size in 2030 | US$ 945 million |

| CAGR | 2.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Hatebur, Asahi Sunac Corporation, National Machinery LLC, Siijn Intelligent Forming Machinery, NEDSCHROEF Machinery, Chun Zu Machinery Industry, YESWIN, Sakamura, Sacma Group, Ningbo Haixing Machinery, Shixi Enterprise, Nakashimada, Tanisaka Iron Works Ltd., Harbin Rainbow Technology Co.,Ltd, ESSEBI |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |