What is Global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market?

The Global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market is a specialized segment within the broader pulp and paper industry. BCTMP is a type of pulp produced through a combination of chemical and mechanical processes, which results in a high-yield pulp with excellent brightness and strength properties. This type of pulp is particularly valued for its cost-effectiveness and versatility, making it suitable for a wide range of paper products. The global market for BCTMP is driven by the increasing demand for paperboard, tissue, and specialty papers, among other applications. The market is characterized by a few key players who dominate the industry, and it is geographically diverse, with significant consumption in regions like Europe, North America, and China. The market dynamics are influenced by factors such as raw material availability, technological advancements, and environmental regulations. Overall, the BCTMP market is poised for steady growth, driven by its unique properties and the ongoing demand for high-quality paper products.

Hardwood BCTMP, Softwood BCTMP, Others in the Global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market:

Hardwood BCTMP, Softwood BCTMP, and other types of BCTMP each have distinct characteristics and applications within the Global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market. Hardwood BCTMP is derived from deciduous trees such as birch, aspen, and maple. This type of pulp is known for its short fibers, which contribute to a smooth surface and good printability, making it ideal for coated and uncoated papers, as well as specialty papers. Hardwood BCTMP is also used in tissue and towel products due to its softness and absorbency. On the other hand, Softwood BCTMP is produced from coniferous trees like spruce, pine, and fir. Softwood BCTMP is characterized by its long fibers, which provide excellent strength and bulk. This makes it particularly suitable for paperboard applications, where durability and rigidity are essential. Softwood BCTMP is also used in the production of high-strength papers and specialty products that require enhanced mechanical properties. In addition to hardwood and softwood BCTMP, there are other types of BCTMP that are produced from a mix of hardwood and softwood fibers or from non-wood sources such as agricultural residues. These other types of BCTMP offer a balance of properties and are used in various applications depending on the specific requirements. The choice between hardwood, softwood, and other types of BCTMP depends on factors such as the desired end-use properties, cost considerations, and availability of raw materials. Each type of BCTMP has its own advantages and limitations, and manufacturers often blend different types to achieve the optimal balance of properties for their specific applications. Overall, the diversity of BCTMP types allows for a wide range of applications and contributes to the versatility and growth of the global BCTMP market.

Paperboard, Coated and Uncoated Papers, Tissue and Towel, Specialty and Others in the Global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market:

The Global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market finds extensive usage in various areas, including paperboard, coated and uncoated papers, tissue and towel, specialty papers, and others. In the paperboard sector, BCTMP is highly valued for its strength and bulk, making it an ideal material for packaging applications. Paperboard made from BCTMP is used in the production of cartons, boxes, and other packaging materials that require durability and rigidity. The high yield and cost-effectiveness of BCTMP also make it a preferred choice for paperboard manufacturers looking to optimize their production processes. In the realm of coated and uncoated papers, BCTMP is prized for its excellent printability and smooth surface. Coated papers, which are used in high-quality printing applications such as magazines, brochures, and catalogs, benefit from the brightness and smoothness provided by BCTMP. Uncoated papers, used in applications like office paper, envelopes, and notebooks, also benefit from the good printability and opacity of BCTMP. In the tissue and towel sector, BCTMP is used for its softness and absorbency. Tissue products such as facial tissues, toilet paper, and paper towels require a pulp that can provide a soft feel and high absorbency, and BCTMP meets these requirements effectively. The high yield of BCTMP also makes it a cost-effective option for tissue manufacturers. Specialty papers, which include products such as filter papers, release liners, and security papers, also utilize BCTMP for its unique properties. The versatility of BCTMP allows it to be tailored to meet the specific requirements of these specialty applications, whether it be strength, smoothness, or other desired characteristics. In addition to these primary areas, BCTMP is also used in other applications such as newsprint, book papers, and certain types of industrial papers. The diverse range of applications for BCTMP highlights its versatility and the important role it plays in the global pulp and paper industry.

Global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market Outlook:

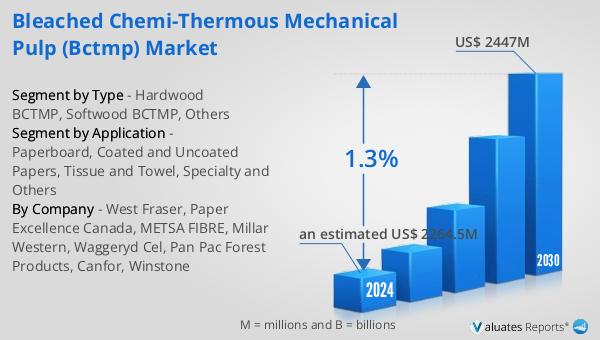

The global Bleached Chemi-Thermous Mechanical Pulp (BCTMP) market is anticipated to grow from an estimated US$ 2264.5 million in 2024 to US$ 2447 million by 2030, reflecting a compound annual growth rate (CAGR) of 1.3% during the period from 2024 to 2030. The market is dominated by the top three BCTMP players, who collectively account for approximately 46% of the total global market. Europe stands out as the largest consumer market for BCTMP, representing about 25% of the global consumption, followed by North America and China. When it comes to types of BCTMP, Softwood BCTMP holds the largest segment with a share of 58%. This dominance is attributed to the superior strength and bulk properties of softwood fibers, which make them highly suitable for a wide range of applications, particularly in the paperboard sector. The market dynamics are shaped by various factors, including technological advancements, environmental regulations, and the availability of raw materials. The steady growth of the BCTMP market is driven by its unique properties and the ongoing demand for high-quality paper products across different regions.

| Report Metric | Details |

| Report Name | Bleached Chemi-Thermous Mechanical Pulp (BCTMP) Market |

| Accounted market size in 2024 | an estimated US$ 2264.5 million |

| Forecasted market size in 2030 | US$ 2447 million |

| CAGR | 1.3% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | West Fraser, Paper Excellence Canada, METSA FIBRE, Millar Western, Waggeryd Cel, Pan Pac Forest Products, Canfor, Winstone |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |