What is Global High-brightness LED Market?

The Global High-brightness LED Market refers to the worldwide industry focused on the production and sale of high-brightness light-emitting diodes (LEDs). These LEDs are known for their superior luminosity and energy efficiency compared to traditional lighting solutions. High-brightness LEDs are used in a variety of applications, including automotive lighting, general illumination, backlighting for displays, and signage. The market has seen significant growth due to the increasing demand for energy-efficient lighting solutions and the rising adoption of LEDs in various sectors. Technological advancements have also played a crucial role in enhancing the performance and reducing the cost of high-brightness LEDs, making them more accessible to a broader range of consumers and industries. The market is characterized by intense competition among key players, continuous innovation, and a focus on sustainability and energy conservation. As a result, the Global High-brightness LED Market is poised for continued expansion, driven by the growing need for efficient and environmentally friendly lighting solutions.

High-Density Multiplexed Diagnostic Assays, Very High-Density Multiplexed Diagnostic Assays in the Global High-brightness LED Market:

High-Density Multiplexed Diagnostic Assays and Very High-Density Multiplexed Diagnostic Assays are advanced diagnostic tools that leverage the capabilities of the Global High-brightness LED Market. These assays are designed to simultaneously detect and quantify multiple biomarkers in a single sample, making them highly efficient and cost-effective for clinical diagnostics. High-brightness LEDs play a crucial role in these assays by providing the necessary illumination for accurate and sensitive detection of biomarkers. The use of high-brightness LEDs ensures that the assays can deliver precise and reliable results, even when dealing with complex and low-abundance targets. In High-Density Multiplexed Diagnostic Assays, multiple biomarkers are detected using a combination of fluorescent dyes and high-brightness LEDs. The LEDs excite the fluorescent dyes, causing them to emit light at specific wavelengths, which is then detected and quantified by specialized instruments. This process allows for the simultaneous analysis of multiple biomarkers, providing comprehensive diagnostic information from a single sample. Very High-Density Multiplexed Diagnostic Assays take this concept a step further by increasing the number of detectable biomarkers, thereby enhancing the diagnostic capabilities and throughput of the assays. The integration of high-brightness LEDs in these assays is essential for achieving the required sensitivity and specificity. The LEDs provide consistent and intense illumination, which is critical for the accurate detection of low-abundance biomarkers. Additionally, the energy efficiency and long lifespan of high-brightness LEDs make them ideal for use in diagnostic assays, where consistent performance and reliability are paramount. The Global High-brightness LED Market has enabled significant advancements in multiplexed diagnostic assays, contributing to improved diagnostic accuracy, faster turnaround times, and reduced costs. These benefits are particularly important in clinical settings, where timely and accurate diagnostics are crucial for patient care. The use of high-brightness LEDs in multiplexed diagnostic assays also supports the development of personalized medicine, as it allows for the detailed analysis of multiple biomarkers, leading to more tailored and effective treatment plans. Overall, the integration of high-brightness LEDs in High-Density and Very High-Density Multiplexed Diagnostic Assays represents a significant advancement in the field of diagnostics, driven by the innovations and growth within the Global High-brightness LED Market.

Clinical Diagnostic Laboratories, Hospitals and Clinics in the Global High-brightness LED Market:

The Global High-brightness LED Market has found extensive applications in Clinical Diagnostic Laboratories, Hospitals, and Clinics, revolutionizing the way diagnostics and patient care are conducted. In Clinical Diagnostic Laboratories, high-brightness LEDs are used in a variety of diagnostic instruments and assays, including High-Density and Very High-Density Multiplexed Diagnostic Assays. These LEDs provide the necessary illumination for accurate detection and quantification of biomarkers, enabling laboratories to perform comprehensive and precise diagnostics. The energy efficiency and long lifespan of high-brightness LEDs also contribute to cost savings and operational efficiency in laboratories, allowing them to handle a higher volume of tests with consistent performance. In Hospitals, high-brightness LEDs are used in various medical devices and equipment, such as surgical lights, endoscopes, and imaging systems. The superior brightness and clarity provided by these LEDs enhance the visibility and accuracy of medical procedures, improving patient outcomes. For instance, in surgical lights, high-brightness LEDs offer bright, shadow-free illumination, allowing surgeons to perform intricate procedures with greater precision. In endoscopes, the use of high-brightness LEDs ensures clear and detailed imaging of internal organs, aiding in accurate diagnosis and treatment. The energy efficiency of high-brightness LEDs also reduces the overall energy consumption of hospitals, contributing to sustainability and cost savings. Clinics also benefit from the use of high-brightness LEDs in various diagnostic and treatment devices. For example, in dermatology clinics, high-brightness LEDs are used in phototherapy devices for the treatment of skin conditions such as psoriasis and eczema. The consistent and intense illumination provided by these LEDs ensures effective treatment outcomes. Additionally, high-brightness LEDs are used in diagnostic devices such as otoscopes and ophthalmoscopes, providing clear and bright illumination for the examination of the ear and eye, respectively. The use of high-brightness LEDs in these devices enhances the accuracy of diagnoses and improves patient care. Overall, the Global High-brightness LED Market has significantly impacted Clinical Diagnostic Laboratories, Hospitals, and Clinics by providing advanced lighting solutions that enhance the accuracy, efficiency, and effectiveness of diagnostics and medical procedures. The continuous innovation and growth within the market are expected to drive further advancements in medical technology, ultimately improving patient care and outcomes.

Global High-brightness LED Market Outlook:

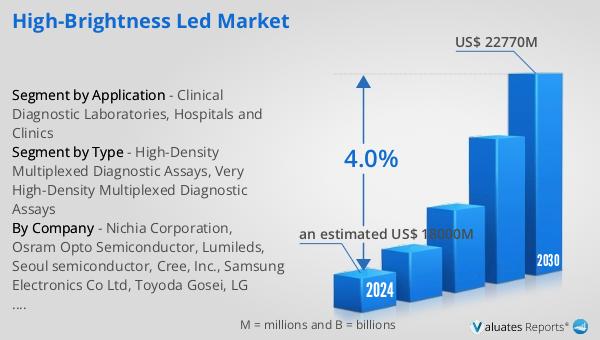

The global market for High-brightness LEDs is anticipated to grow significantly, reaching an estimated value of US$ 22,770 million by 2030, up from approximately US$ 18,000 million in 2024. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.0% between 2024 and 2030. The market is highly competitive, with the top three players collectively holding around 30% of the total market share. This indicates a concentrated market where a few key players dominate, driving innovation and setting industry standards. The projected growth of the High-brightness LED market is driven by increasing demand for energy-efficient lighting solutions across various sectors, including automotive, general illumination, and display backlighting. Technological advancements and continuous innovation are also key factors contributing to the market's expansion. As the market grows, it is expected to see further developments in LED technology, leading to even more efficient and cost-effective lighting solutions. The competitive landscape will likely continue to evolve, with major players striving to maintain their market positions through strategic initiatives and product innovations. Overall, the future of the Global High-brightness LED Market looks promising, with significant growth opportunities and advancements on the horizon.

| Report Metric | Details |

| Report Name | High-brightness LED Market |

| Accounted market size in 2024 | an estimated US$ 18000 in million |

| Forecasted market size in 2030 | US$ 22770 million |

| CAGR | 4.0% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Nichia Corporation, Osram Opto Semiconductor, Lumileds, Seoul semiconductor, Cree, Inc., Samsung Electronics Co Ltd, Toyoda Gosei, LG Innoteck, Everlight, MLS CO.,LTD |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |