What is Global Fixed Focus Camera Module Market?

The Global Fixed Focus Camera Module Market refers to the worldwide industry focused on the production and distribution of camera modules that have a fixed focus lens. Unlike adjustable or auto-focus lenses, fixed focus lenses are set to a specific focal length and cannot be altered. These modules are widely used in various electronic devices such as mobile phones, digital cameras, and other imaging devices. The primary advantage of fixed focus camera modules is their simplicity and cost-effectiveness, making them ideal for mass production and use in budget-friendly devices. They are particularly popular in applications where the subject distance is relatively constant, and high precision focusing is not required. This market is driven by the increasing demand for affordable imaging solutions and the growing integration of cameras in a wide range of consumer electronics. The fixed focus camera module market is characterized by continuous advancements in technology, aiming to improve image quality and reduce production costs.

Lens Module, Lens Mounts, Photoreceptor, Others in the Global Fixed Focus Camera Module Market:

In the context of the Global Fixed Focus Camera Module Market, several key components play crucial roles, including the lens module, lens mounts, photoreceptor, and other associated parts. The lens module is the core component that houses the fixed focus lens. It is designed to capture light and direct it onto the photoreceptor. The quality of the lens module significantly impacts the overall image quality, making it a critical element in the camera module. Lens mounts are the structures that hold the lens module in place within the camera assembly. They ensure that the lens is correctly aligned and securely attached, which is essential for maintaining consistent image quality. Photoreceptors, also known as image sensors, are responsible for converting the light captured by the lens into electronic signals that can be processed to form an image. The performance of the photoreceptor is vital for determining the resolution and clarity of the captured images. Other components in the fixed focus camera module include the housing, which protects the internal parts, and various electronic circuits that manage the operation of the camera. These components work together to create a functional and efficient camera module that can be integrated into various devices. The continuous development and refinement of these components are essential for meeting the evolving demands of the market and enhancing the performance of fixed focus camera modules.

Mobile Phone, Digital Camera, Others in the Global Fixed Focus Camera Module Market:

The Global Fixed Focus Camera Module Market finds extensive usage in several key areas, including mobile phones, digital cameras, and other electronic devices. In mobile phones, fixed focus camera modules are commonly used in front-facing cameras for selfies and video calls. Their simplicity and cost-effectiveness make them ideal for this application, where the subject distance is relatively constant, and high precision focusing is not required. Fixed focus modules provide adequate image quality for social media sharing and video conferencing, making them a popular choice among smartphone manufacturers. In digital cameras, fixed focus modules are often used in entry-level models designed for casual photography. These cameras are typically aimed at consumers who prefer a straightforward, point-and-shoot experience without the need for manual focusing. The fixed focus design ensures that the camera is always ready to capture images quickly, making it convenient for spontaneous photography. Other applications of fixed focus camera modules include security cameras, webcams, and various industrial and medical imaging devices. In security cameras, the fixed focus design provides a reliable and maintenance-free solution for monitoring fixed areas. Webcams benefit from the simplicity and affordability of fixed focus modules, making them accessible to a wide range of users for video conferencing and online communication. In industrial and medical imaging, fixed focus camera modules are used in applications where the subject distance is controlled, and consistent image quality is required. Overall, the versatility and cost-effectiveness of fixed focus camera modules make them suitable for a wide range of applications, driving their demand in the global market.

Global Fixed Focus Camera Module Market Outlook:

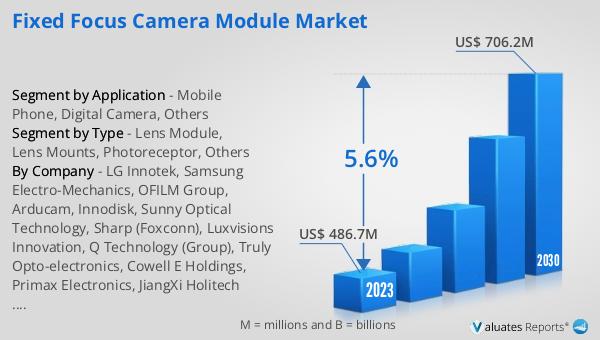

The global Fixed Focus Camera Module market was valued at US$ 486.7 million in 2023 and is anticipated to reach US$ 706.2 million by 2030, witnessing a CAGR of 5.6% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by the increasing demand for affordable and reliable imaging solutions across various industries. The fixed focus camera module market benefits from the widespread adoption of cameras in consumer electronics, particularly mobile phones and digital cameras. As technology continues to advance, the performance and image quality of fixed focus camera modules are expected to improve, further boosting their adoption. The market's growth is also supported by the ongoing development of new applications and the integration of camera modules into a broader range of devices. This positive market outlook reflects the potential for significant opportunities and advancements in the fixed focus camera module industry over the coming years.

| Report Metric | Details |

| Report Name | Fixed Focus Camera Module Market |

| Accounted market size in 2023 | US$ 486.7 million |

| Forecasted market size in 2030 | US$ 706.2 million |

| CAGR | 5.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | LG Innotek, Samsung Electro-Mechanics, OFILM Group, Arducam, Innodisk, Sunny Optical Technology, Sharp (Foxconn), Luxvisions Innovation, Q Technology (Group), Truly Opto-electronics, Cowell E Holdings, Primax Electronics, JiangXi Holitech Technology, Namuga, Partron, MCNEX, Jiangxi Shine-Tech Optical, Shenzhen Sinoseen Technology, Shenzhen CM Technology, Rayprus, Beilong Precision Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |